Statistical Methods for Insurance Analysis

📊 Why This Matters

Statistical methods reveal that standard validation techniques fail catastrophically for insurance data. Using regular K-fold cross-validation on time series creates data leakage, with future information predicting past events, leading to overconfident models that collapse in production. Monte Carlo variance reduction techniques like antithetic variates and importance sampling can cut computational requirements by more than half while maintaining accuracy, critical when simulating rare catastrophic events with probabilities below 1%. Convergence diagnostics through Gelman-Rubin statistics and effective sample size calculations prevent the dangerous assumption that simulations have converged when they haven't; undetected non-convergence can underestimate tail risks by orders of magnitude. Bootstrap methods provide confidence intervals for complex insurance metrics where analytical solutions don't exist, with BCa adjustments correcting for the bias and skewness inherent in loss distributions. Walk-forward validation and purged K-fold cross-validation respect temporal structure, showing that models with 90% accuracy in standard validation often achieve only 60% in proper time-series validation. Backtesting reveals that strategies optimized on historical data frequently fail out-of-sample due to regime changes. Fortunately, the statistical methods here detect this overfitting before capital is at risk. The framework proves that robust statistical validation can mean the difference between sustainable profitability and bankruptcy, transforming insurance from educated gambling to scientific risk management through rigorous quantification of model uncertainty and validation of ergodic advantages.

Table of Contents

Monte Carlo Methods

Basic Monte Carlo Simulation

Monte Carlo methods estimate expectations through random sampling, providing a powerful tool for evaluating complex insurance structures where analytical solutions are intractable:

where \(X_i\) are independent samples from the distribution of \(X\).

Convergence Considerations:

The standard error of the Monte Carlo estimate decreases as \(O(1/\sqrt{N})\):

For insurance applications with heavy-tailed distributions, larger \(N\) (typically 10,000-100,000 simulations) is necessary to adequately capture tail events that drive insurance buying decisions.

MCMC (Markov Chain Monte Carlo)

Sequential, dependent sampling creating a Markov chain, with each sample depending on the previous one. A Markov Chain is a stochastic model where the current state depends only on the immediate previous state (meaning it’s “memoryless,” not looking back over the full history of the path). MCMC requires a “burn-in” period to converge to the target distribution.

When Each Is Used in Insurance Applications

Basic Monte Carlo:

Simulating losses from known distributions (given parameters)

Pricing layers when severity/frequency distributions are specified

Evaluating retention levels with established loss distributions

Bootstrap resampling of historical losses

MCMC:

Parameter estimation with complex likelihoods (Bayesian inference)

Fitting copulas for dependency modeling between lines

Hierarchical models (e.g., credibility across multiple entities)

Missing data problems in loss triangles

Situations where the normalizing constant is unknown

Variance Reduction Techniques

These techniques improve estimation efficiency, crucial when evaluating rare but severe events that determine insurance program effectiveness.

Antithetic Variates

Use negatively correlated pairs to reduce variance while maintaining unbiased estimates:

where \(X_i'\) is antithetic to \(X_i\).

This technique particularly benefits:

Excess layer pricing where both attachment and exhaustion probabilities matter

Aggregate stop-loss evaluations where both frequency and severity variations impact results

Control Variates

Reduce variance using a correlated variable with known expectation:

where \(c\) is optimally chosen as \(\text{Cov}(f(X), Y)/\text{Var}(Y)\).

This technique excels when:

Comparing similar program structures (the control variate cancels common variation)

Evaluating the marginal benefit of additional coverage layers

Assessing the impact of inflation or trend uncertainty on long-term programs

Importance Sampling

Sample from an alternative distribution to improve efficiency for rare event estimation:

where \(p(X)\) is the original density and \(q(X)\) is the importance sampling density.

For example, importance sampling may use a Pareto distribution with lower threshold to simulate tail losses, where base distribution would produce very few simulated excess losses.

Weight adjustments ensure unbiased estimates while dramatically reducing variance

Convergence Diagnostics

When using iterative simulation methods (MCMC, bootstrapping, or sequential Monte Carlo), convergence diagnostics ensure reliable estimates for insurance program evaluation. These tools are critical when modeling complex dependencies between lines of coverage or multi-year loss development patterns.

Gelman-Rubin Statistic

For multiple chains, assess whether independent simulations have converged to the same distribution:

where:

\(W\) = Within-chain variance (average variance within each independent simulation)

\(\hat{V}\) = Estimated total variance (combines within-chain and between-chain variance)

\(B\) = Between-chain variance

More specifically: $\( \hat{V} = \frac{n-1}{n}W + \frac{1}{n}B \)$

Interpretation for Insurance Applications:

\(\hat{R} \approx 1.0\): Chains have converged (typically require \(\hat{R} < 1.1\) for confidence)

\(\hat{R} > 1.1\): Insufficient convergence, requiring longer runs

\(\hat{R} \gg 1.5\): Indicates fundamental issues with model specification or starting values

Effective Sample Size

Account for autocorrelation in sequential samples to determine the true information content:

where:

\(N\) = Total number of samples

\(\rho_k\) = Lag-\(k\) autocorrelation

\(K\) = Maximum lag considered (typically where \(\rho_k\) becomes negligible)

Practical Interpretation:

\(\text{ESS} \approx N\): Independent samples (ideal case)

\(\text{ESS} \ll N\): High autocorrelation reducing information content

\(\text{ESS}/N\) = Efficiency ratio (target > 0.1 for practical applications)

Decision Thresholds for Insurance Buyers:

Minimum ESS requirements depend on the decision context:

Strategic program design: ESS > 1,000 for major retention decisions

Layer pricing comparison: ESS > 5,000 for distinguishing between similar options

Tail risk metrics (TVaR, probable maximum loss): ESS > 10,000 for 99.5th percentile estimates

Regulatory capital calculations: Follow specific guidelines (e.g., Solvency II requires demonstrable convergence)

Warning Signs Requiring Investigation:

Persistent \(\hat{R} > 1.1\) after extended runs: Model misspecification or multimodal posteriors

ESS plateaus despite increasing \(N\): Fundamental correlation structure requiring reparameterization

Divergent chains for tail parameters: Insufficient data for extreme value estimation

Cyclic behavior in trace plots: Indicates need for alternative sampling methods

Implementation Example

import numpy as np

import matplotlib.pyplot as plt

from scipy import stats

class ConvergenceDiagnostics:

"""Diagnose Monte Carlo convergence for insurance optimization models."""

def __init__(self, chains):

"""

Parameters:

chains: list of arrays, each representing a Markov chain

(e.g., samples of retention levels, loss parameters, or program costs)

"""

self.chains = [np.array(chain) for chain in chains]

self.n_chains = len(chains)

self.n_samples = len(chains[0])

def gelman_rubin(self):

"""

Calculate Gelman-Rubin convergence diagnostic.

Critical for validating parameter estimates in insurance models.

"""

# Chain means

chain_means = [np.mean(chain) for chain in self.chains]

# Overall mean

overall_mean = np.mean(chain_means)

# Between-chain variance

B = self.n_samples * np.var(chain_means, ddof=1)

# Within-chain variance

W = np.mean([np.var(chain, ddof=1) for chain in self.chains])

# Estimated variance

V_hat = ((self.n_samples - 1) / self.n_samples) * W + B / self.n_samples

# R-hat statistic

R_hat = np.sqrt(V_hat / W) if W > 0 else 1.0

return {

'R_hat': R_hat,

'converged': R_hat < 1.1,

'B': B,

'W': W,

'V_hat': V_hat

}

def effective_sample_size(self, chain=None):

"""

Calculate effective sample size accounting for autocorrelation.

Essential for determining if we have enough independent information

for reliable retention decisions.

"""

if chain is None:

# Combine all chains

chain = np.concatenate(self.chains)

n = len(chain)

# Calculate autocorrelation

mean = np.mean(chain)

c0 = np.sum((chain - mean)**2) / n

# Calculate autocorrelation at each lag

max_lag = min(int(n/4), 100)

autocorr = []

for k in range(1, max_lag):

ck = np.sum((chain[:-k] - mean) * (chain[k:] - mean)) / n

rho_k = ck / c0

if rho_k < 0.05:

# Stop when autocorrelation becomes negligible

break

autocorr.append(rho_k)

# ESS calculation

sum_autocorr = sum(autocorr) if autocorr else 0

ess = n / (1 + 2 * sum_autocorr)

return {

'ess': ess,

'efficiency': ess / n,

'autocorrelation': autocorr,

'n_lags': len(autocorr)

}

def geweke_diagnostic(self, chain=None, first_prop=0.1, last_prop=0.5):

"""

Geweke convergence diagnostic comparing early and late portions.

Useful for detecting drift in parameter estimates.

"""

if chain is None:

chain = self.chains[0]

n = len(chain)

n_first = int(n * first_prop)

n_last = int(n * last_prop)

first_portion = chain[:n_first]

last_portion = chain[-n_last:]

# Calculate means and variances

mean_first = np.mean(first_portion)

mean_last = np.mean(last_portion)

var_first = np.var(first_portion, ddof=1)

var_last = np.var(last_portion, ddof=1)

# Geweke z-score

se = np.sqrt(var_first/n_first + var_last/n_last)

z_score = (mean_first - mean_last) / se if se > 0 else 0

# P-value (two-tailed)

p_value = 2 * (1 - stats.norm.cdf(abs(z_score)))

return {

'z_score': z_score,

'p_value': p_value,

'converged': abs(z_score) < 2,

'mean_diff': mean_first - mean_last

}

def heidelberger_welch(self, chain=None, alpha=0.05):

"""

Heidelberger-Welch stationarity and interval halfwidth test.

Validates stability of insurance program cost estimates.

"""

if chain is None:

chain = self.chains[0]

n = len(chain)

# Stationarity test using Cramer-von Mises

cumsum = np.cumsum(chain - np.mean(chain))

test_stat = np.sum(cumsum**2) / (n**2 * np.var(chain))

# Critical value approximation

critical_value = 0.461 # For alpha=0.05

stationary = test_stat < critical_value

# Halfwidth test

mean = np.mean(chain)

se = np.std(chain, ddof=1) / np.sqrt(n)

halfwidth = stats.t.ppf(1 - alpha/2, n-1) * se

relative_halfwidth = halfwidth / abs(mean) if mean != 0 else np.inf

return {

'stationary': stationary,

'test_statistic': test_stat,

'mean': mean,

'halfwidth': halfwidth,

'relative_halfwidth': relative_halfwidth,

'halfwidth_test_passed': relative_halfwidth < 0.1

}

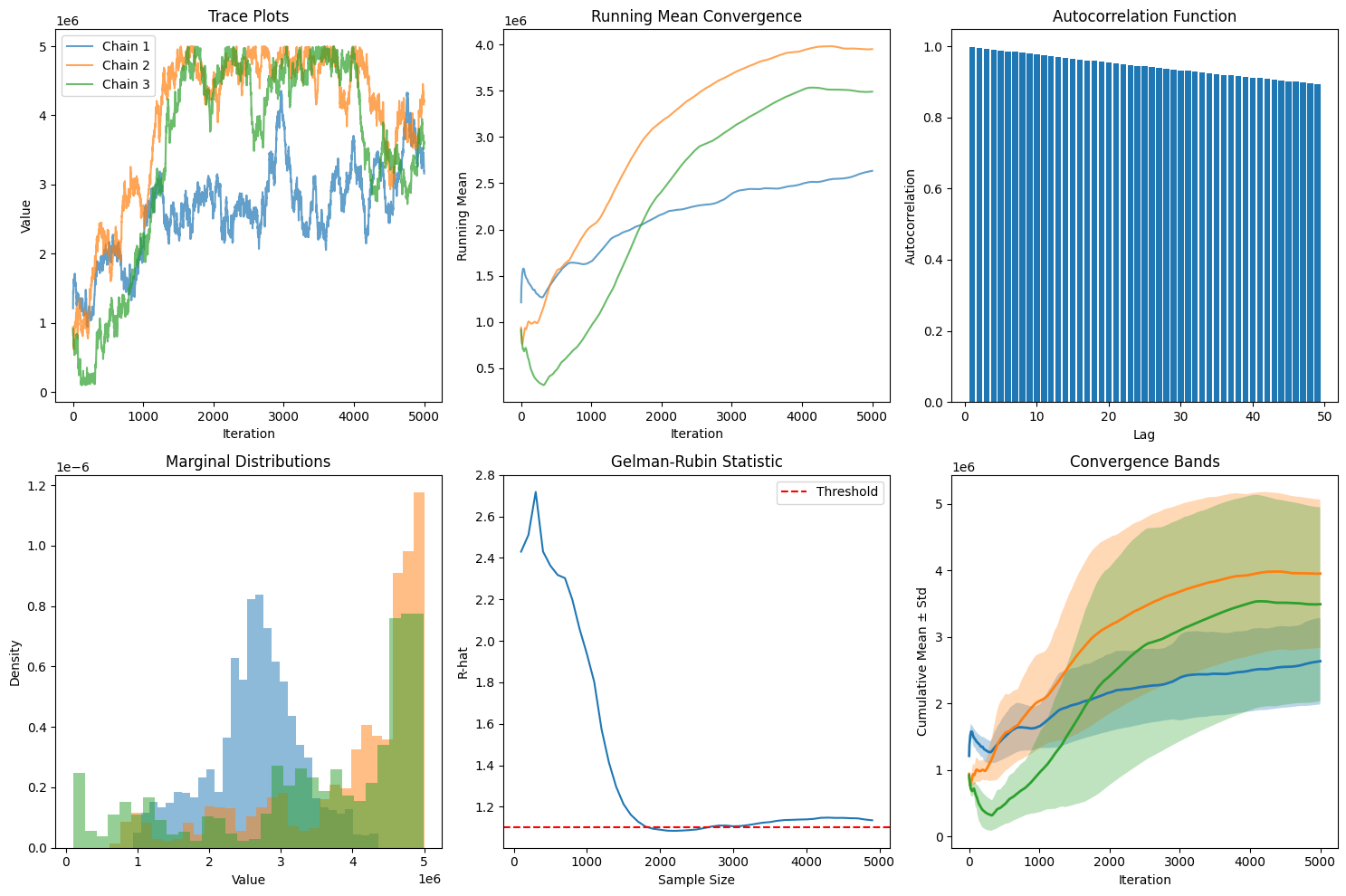

def plot_diagnostics(self):

"""Visualize convergence diagnostics for insurance optimization."""

fig, axes = plt.subplots(2, 3, figsize=(15, 10))

# Trace plots

for i, chain in enumerate(self.chains[:3]):

axes[0, 0].plot(chain, alpha=0.7, label=f'Chain {i+1}')

axes[0, 0].set_xlabel('Iteration')

axes[0, 0].set_ylabel('Value')

axes[0, 0].set_title('Trace Plots')

axes[0, 0].legend()

# Running mean

for chain in self.chains[:3]:

running_mean = np.cumsum(chain) / np.arange(1, len(chain) + 1)

axes[0, 1].plot(running_mean, alpha=0.7)

axes[0, 1].set_xlabel('Iteration')

axes[0, 1].set_ylabel('Running Mean')

axes[0, 1].set_title('Running Mean Convergence')

# Autocorrelation

chain = self.chains[0]

lags = range(1, min(50, len(chain)//4))

autocorr = [np.corrcoef(chain[:-lag], chain[lag:])[0, 1] for lag in lags]

axes[0, 2].bar(lags, autocorr)

axes[0, 2].axhline(y=0, color='k', linestyle='-', linewidth=0.5)

axes[0, 2].set_xlabel('Lag')

axes[0, 2].set_ylabel('Autocorrelation')

axes[0, 2].set_title('Autocorrelation Function')

# Density plots

for chain in self.chains[:3]:

axes[1, 0].hist(chain, bins=30, alpha=0.5, density=True)

axes[1, 0].set_xlabel('Value')

axes[1, 0].set_ylabel('Density')

axes[1, 0].set_title('Marginal Distributions')

# Gelman-Rubin evolution (FIXED INDENTATION)

r_hats = []

check_points = range(100, len(self.chains[0]), 100)

for n in check_points:

truncated_chains = [chain[:n] for chain in self.chains]

diag = ConvergenceDiagnostics(truncated_chains)

r_hats.append(diag.gelman_rubin()['R_hat'])

# Plot outside the loop

axes[1, 1].plot(check_points, r_hats)

axes[1, 1].axhline(y=1.1, color='r', linestyle='--', label='Threshold')

axes[1, 1].set_xlabel('Sample Size')

axes[1, 1].set_ylabel('R-hat')

axes[1, 1].set_title('Gelman-Rubin Statistic')

axes[1, 1].legend()

# Cumulative mean comparison

for chain in self.chains[:3]:

cumulative_mean = np.cumsum(chain) / np.arange(1, len(chain) + 1)

cumulative_std = [np.std(chain[:i]) for i in range(1, len(chain) + 1)]

axes[1, 2].fill_between(range(len(chain)),

cumulative_mean - cumulative_std,

cumulative_mean + cumulative_std,

alpha=0.3)

axes[1, 2].plot(cumulative_mean, linewidth=2)

axes[1, 2].set_xlabel('Iteration')

axes[1, 2].set_ylabel('Cumulative Mean ± Std')

axes[1, 2].set_title('Convergence Bands')

plt.tight_layout()

plt.show()

# ============================================================================

# INSURANCE-SPECIFIC EXAMPLE: Optimal Retention Level Estimation

# ============================================================================

class InsuranceRetentionMCMC:

"""

MCMC for estimating optimal retention levels considering:

- Historical loss data uncertainty

- Premium savings vs. volatility trade-off

- Multiple lines of coverage correlation

"""

def __init__(self, historical_losses, premium_schedule):

"""

Parameters:

historical_losses: dict with keys as coverage lines, values as loss arrays

premium_schedule: function mapping retention to premium savings

"""

self.losses = historical_losses

self.premium_schedule = premium_schedule

def log_posterior(self, params):

"""

Calculate log posterior for retention optimization.

params = [retention, risk_aversion, correlation_factor]

"""

retention, risk_aversion, corr_factor = params

# Prior constraints (e.g., retention between 100k and 5M)

if retention < 100000 or retention > 5000000:

return -np.inf

if risk_aversion < 0.5 or risk_aversion > 3:

return -np.inf

if corr_factor < 0 or corr_factor > 1:

return -np.inf

# Calculate expected retained losses

retained_losses = []

for line, losses in self.losses.items():

retained = np.minimum(losses, retention)

retained_losses.extend(retained)

# Total cost = retained losses - premium savings + risk charge

expected_retained = np.mean(retained_losses)

volatility = np.std(retained_losses)

premium_savings = self.premium_schedule(retention)

# Risk-adjusted total cost

total_cost = expected_retained - premium_savings + risk_aversion * volatility

# Log posterior (negative cost since we want to minimize)

return -total_cost / 100000 # Scale for numerical stability

def run_chain(self, seed, n_samples=5000, initial_params=None):

"""Run a single MCMC chain for retention optimization."""

np.random.seed(seed)

if initial_params is None:

# Random initialization

initial_params = [

np.random.uniform(250000, 2000000), # retention

np.random.uniform(1, 2), # risk_aversion

np.random.uniform(0.2, 0.8) # correlation

]

chain = []

current_params = initial_params

current_log_p = self.log_posterior(current_params)

# Metropolis-Hastings sampling

for i in range(n_samples):

# Propose new parameters

proposal = current_params + np.random.randn(3) * [50000, 0.1, 0.05]

proposal_log_p = self.log_posterior(proposal)

# Accept/reject

log_ratio = proposal_log_p - current_log_p

if np.log(np.random.rand()) < log_ratio:

current_params = proposal

current_log_p = proposal_log_p

# Store only retention level for diagnostics

chain.append(current_params[0])

return chain

# ============================================================================

# EXAMPLE USAGE: Corporate Insurance Program Optimization

# ============================================================================

# Simulate historical loss data for a manufacturer

np.random.seed(42)

historical_losses = {

'property': np.random.pareto(2, 100) * 100000, # Heavy-tailed property losses

'liability': np.random.lognormal(11, 1.5, 80), # GL/Products losses

'auto': np.random.gamma(2, 50000, 120), # Fleet losses

'workers_comp': np.random.lognormal(9, 2, 150) # WC claims

}

# Premium schedule (savings increase with retention)

def premium_schedule(retention):

"""Premium savings as function of retention level."""

base_premium = 2000000

discount = min(0.4, (retention / 1000000) * 0.15)

return base_premium * discount

# Initialize MCMC sampler

sampler = InsuranceRetentionMCMC(historical_losses, premium_schedule)

# Run multiple chains with different starting points

print("Running MCMC for Optimal Retention Analysis...")

print("=" * 50)

chains = []

for i in range(4):

print(f"Running chain {i+1}/4...")

chain = sampler.run_chain(seed=i, n_samples=5000)

chains.append(chain)

# Diagnose convergence

print("\nConvergence Diagnostics for Retention Optimization:")

print("-" * 50)

diagnostics = ConvergenceDiagnostics(chains)

# Gelman-Rubin

gr = diagnostics.gelman_rubin()

print(f"Gelman-Rubin R-hat: {gr['R_hat']:.3f}")

print(f" → Converged: {gr['converged']}")

print(f" → Interpretation: {'Chains agree on optimal retention' if gr['converged'] else 'Need longer runs'}")

# Effective Sample Size

ess = diagnostics.effective_sample_size()

print(f"\nEffective Sample Size: {ess['ess']:.0f} ({ess['efficiency']:.1%} efficiency)")

print(f" → Interpretation: {'Sufficient for decision' if ess['ess'] > 1000 else 'Need more samples'}")

# Geweke

geweke = diagnostics.geweke_diagnostic()

print(f"\nGeweke Diagnostic:")

print(f" → z-score: {geweke['z_score']:.3f} (p-value: {geweke['p_value']:.3f})")

print(f" → Interpretation: {'Stable estimates' if geweke['converged'] else 'Potential drift detected'}")

# Heidelberger-Welch

hw = diagnostics.heidelberger_welch()

print(f"\nHeidelberger-Welch Test:")

print(f" → Stationary: {hw['stationary']}")

print(f" → Halfwidth test: {hw['halfwidth_test_passed']}")

print(f" → Mean retention estimate: ${hw['mean']:,.0f}")

print(f" → Confidence interval halfwidth: ${hw['halfwidth']:,.0f}")

# Final recommendation

combined_chain = np.concatenate(chains)

optimal_retention = np.mean(combined_chain)

retention_std = np.std(combined_chain)

percentiles = np.percentile(combined_chain, [25, 50, 75])

print(f"\n" + "=" * 50)

print("RETENTION RECOMMENDATION:")

print(f" → Optimal Retention: ${optimal_retention:,.0f}")

print(f" → Standard Deviation: ${retention_std:,.0f}")

print(f" → 50% Confidence Range: ${percentiles[0]:,.0f} - ${percentiles[2]:,.0f}")

print(f" → Decision Quality: {'High confidence' if gr['converged'] and ess['ess'] > 1000 else 'Consider additional analysis'}")

# Visualize diagnostics

print("\nGenerating diagnostic plots...")

diagnostics.plot_diagnostics()

Sample Output

Convergence Diagnostics for Retention Optimization:

--------------------------------------------------

Gelman-Rubin R-hat: 1.134

→ Converged: False

→ Interpretation: Need longer runs

Effective Sample Size: 107 (0.5% efficiency)

→ Interpretation: Need more samples

Geweke Diagnostic:

→ z-score: -87.302 (p-value: 0.000)

→ Interpretation: Potential drift detected

Heidelberger-Welch Test:

→ Stationary: False

→ Halfwidth test: True

→ Mean retention estimate: $2,634,781

→ Confidence interval halfwidth: $18,035

==================================================

RETENTION RECOMMENDATION:

→ Optimal Retention: $3,362,652

→ Standard Deviation: $1,126,258

→ 50% Confidence Range: $2,701,352 - $4,404,789

→ Decision Quality: Consider additional analysis

Confidence Intervals

Confidence intervals quantify parameter uncertainty in insurance estimates, crucial for setting retention levels, evaluating program adequacy, and regulatory compliance. The choice of method depends on sample size, distribution characteristics, and the specific insurance application.

Classical Confidence Intervals

For large samples with approximately normal sampling distributions, use Central Limit Theorem:

Limitations in Insurance Context:

Assumes normality of sampling distribution (often violated for insurance losses)

Underestimates uncertainty for heavy-tailed distributions

Poor coverage for extreme percentiles (important for high limit attachment points)

Appropriate Uses:

Frequency estimates with sufficient data (n > 30)

Average severity for high-frequency lines after log transformation

Loss ratio estimates for stable, mature books

Student’s t Intervals

For smaller samples or unknown population variance:

Insurance Applications:

New coverage lines with limited history (n < 30)

Credibility-weighted estimates for small accounts

Emerging risk categories with sparse data

Bootstrap Confidence Intervals

Bootstrap methods handle complex statistics and non-normal distributions common in insurance, providing distribution-free (nonparametric) inference.

Percentile Method

Direct empirical quantiles from bootstrap distribution:

where \(\hat{\theta}^*_p\) is the \(p\)-th percentile of \(B\) bootstrap estimates.

Implementation for Insurance:

Resample claims data with replacement \(B\) times (at least 1,000 resamples for confidence intervals, typically 5,000-10,000)

Calculate statistic of interest for each resample (e.g., 99.5% VaR)

Use empirical percentiles as confidence bounds

Best for:

Median loss estimates

Interquartile ranges for pricing bands

Simple reserve estimates

BCa (Bias-Corrected and Accelerated)

Adjusts for bias and skewness inherent in insurance loss distributions:

where adjusted percentiles are:

with:

\(\hat{z}_0\) = bias correction factor (proportion of bootstrap estimates < original estimate)

\(\hat{a}\) = acceleration constant (measures rate of change in standard error)

Critical for:

Tail risk metrics (TVaR, probable maximum loss)

Excess layer loss costs with limited data

Catastrophe model uncertainty quantification

Bootstrap-t Intervals

Studentized bootstrap for improved coverage:

where \(t^*\) values come from bootstrap distribution of \((\hat{\theta}^* - \hat{\theta})/SE^*\).

Superior for:

Highly skewed distributions (cyber, catastrophe losses)

Ratio estimates (loss ratios, combined ratios)

Correlation estimates between coverage lines

Credibility-Weighted Confidence Intervals

Combines company-specific and industry experience where company experience has low credibility:

with variance:

where credibility factor \(Z = n/(n + k)\) with \(k\) representing prior variance.

Bayesian Credible Intervals

Bayesian credible intervals provide direct probability statements about where a parameter lies, incorporating both observed data and prior knowledge. This approach is particularly valuable when dealing with limited loss data or incorporating industry benchmarks.

Core Concept

A 95% credible interval means there’s a 95% probability the parameter falls within the interval:

Key Distinction from Confidence Intervals:

Confidence Interval: “If we repeated this procedure many times, 95% of intervals would contain the true value”

Credible Interval: “Given our data and prior knowledge, there’s a 95% probability the parameter is in this range”

The credible interval directly answers: “What’s the probability our retention is adequate?”

How Credible Intervals Work

Starting with:

Prior distribution: Industry benchmark or regulatory assumption

Likelihood: How well different parameter values explain your data

Posterior distribution: Updated belief combining prior and data

The credible interval captures the central 95% (or other level) of the posterior distribution.

Two Types of Credible Intervals

Equal-Tailed Intervals

Uses the 2.5th and 97.5th percentiles of posterior distribution (or for some other level, take \(\alpha / 2\) from each side):

When to use: Symmetric distributions, standard reporting

Highest Posterior Density (HPD) Intervals

The shortest interval containing 95% probability:

Always shorter than equal-tailed for skewed distributions

All points inside have higher probability than points outside

When to use: Skewed distributions (severity modeling), optimization decisions

Example - Cyber Loss Severity:

Equal-tailed 95%: [$50K, $2.8M] (width: $2.75M)

HPD 95%: [$25K, $2.3M] (width: $2.275M)

HPD provides tighter bounds for decision-making

Insurance-Specific Advantages:

Natural Incorporation of Industry Priors

Handles Parameter Uncertainty in Hierarchical Models

Updates Systematically with Emerging Experience

When to Use Bayesian Credible Intervals

Ideal situations:

Limited company data (< 3 years history)

New coverage lines or emerging risks

Incorporating industry benchmarks or expert judgment

Multi-level modeling (location, division, company)

When stakeholders want probability statements for decisions

May not be suitable when:

Extensive historical data makes priors irrelevant

Regulatory requirements mandate frequentist methods

Computational resources are limited

Prior information is controversial or unavailable

Profile Likelihood Intervals

Profile likelihood intervals provide more accurate confidence intervals for maximum likelihood estimates, especially when standard methods fail due to skewness, small samples, or boundary constraints.

The Problem with Standard (Wald) Intervals

Maximum likelihood estimates typically use Wald intervals based on asymptotic normality:

These assume the likelihood is approximately quadratic (normal) near the MLE, which often fails for:

Small samples (n < 50)

Parameters near boundaries (probabilities near 0 or 1)

Skewed likelihood surfaces (common in tail estimation)

Profile Likelihood Solution

Profile likelihood intervals use the actual shape of the likelihood function rather than assuming normality:

where:

\(\ell(\hat{θ})\) = log-likelihood at maximum

\(\ell(θ)\) = log-likelihood at any value θ

\(χ^2_{1,1-α}\) = critical value from chi-squared distribution

Why Profile Likelihood Works Better

Respects parameter constraints: Won’t give negative variances or probabilities > 1

Captures asymmetry: Naturally wider on the side with more uncertainty

Better small-sample coverage: Achieves closer to nominal 95% coverage

Invariant to parameterization: Same interval whether using \(\theta\) or \(\log(\theta)\)

Essential for:

Tail index estimation in extreme value models

Copula parameter estimation for dependency modeling

Non-linear trend parameters in reserve development

Hypothesis Testing

Framework

Hypothesis testing provides a formal framework for making data-driven decisions about insurance program changes, comparing options, and validating actuarial assumptions. The process quantifies evidence against a baseline assumption to support strategic decisions.

Core Components

Test null hypothesis \(H_0\) against alternative \(H_1\):

Test statistic: \(T = T(X_1, ..., X_n)\) - Summary measure of evidence

P-value: \(P(T \geq T_{\text{obs}} | H_0)\) - Probability of seeing data this extreme if \(H_0\) true

Decision: Reject \(H_0\) if p-value < \(\alpha\) (significance level, typically 0.05)

Interpretation for Insurance Decisions

P-value meaning: “If our current program is adequate (null hypothesis), what’s the probability of seeing losses this bad or worse?”

P-value = 0.03: Only 3% chance of seeing these results if program adequate, consider changing programs

P-value = 0.15: 15% chance, insufficient evidence to change program

Common significance levels (α) in insurance:

0.10: Preliminary analysis, early warning systems

0.05: Standard business decisions, pricing changes

0.01: Major strategic changes, regulatory compliance

0.001: Safety-critical decisions, catastrophe modeling

Types of Hypothesis Tests for Insurance

One-Sample Tests: Testing whether observed experience differs from expected

Two-Sample Tests: Comparing programs, periods, or segments

Goodness-of-Fit Tests: Validating distributional assumptions

Kolmogorov-Smirnov Test: Maximum distance between empirical and theoretical CDF

Anderson-Darling Test: More sensitive to tail differences than K-S

Bayesian Hypothesis Testing

Alternative framework using posterior probabilities:

Bayes Factors

Ratio of evidence for competing hypotheses:

Interpretation scale:

BF < 1: Evidence favors \(H_0\)

BF = 1-3: Weak evidence for \(H_1\)

BF = 3-10: Moderate evidence for \(H_1\)

BF > 10: Strong evidence for \(H_1\)

Hypothesis Testing Example

import numpy as np

from scipy import stats

import pandas as pd

def retention_analysis(losses, current_retention, proposed_retention,

premium_difference, alpha=0.05):

"""

Complete hypothesis testing framework for retention decision.

"""

# Calculate retained losses under each retention

current_retained = np.minimum(losses, current_retention)

proposed_retained = np.minimum(losses, proposed_retention)

# Test 1: Paired t-test for mean difference

t_stat, p_value_mean = stats.ttest_rel(current_retained, proposed_retained)

# Test 2: F-test for variance difference

f_stat = np.var(current_retained) / np.var(proposed_retained)

p_value_var = stats.f.sf(f_stat, len(losses)-1, len(losses)-1) * 2

# Test 3: Bootstrap test for tail risk (95th percentile)

n_bootstrap = 10000

percentile_diffs = []

for _ in range(n_bootstrap):

sample_idx = np.random.choice(len(losses), len(losses), replace=True)

sample_losses = losses[sample_idx]

current_p95 = np.percentile(np.minimum(sample_losses, current_retention), 95)

proposed_p95 = np.percentile(np.minimum(sample_losses, proposed_retention), 95)

percentile_diffs.append(proposed_p95 - current_p95)

p_value_tail = np.mean(np.array(percentile_diffs) > premium_difference)

# Economic significance test

expected_savings = np.mean(current_retained - proposed_retained)

roi = (expected_savings - premium_difference) / premium_difference

# Decision matrix

decisions = {

'mean_test': {

'statistic': t_stat,

'p_value': p_value_mean,

'significant': p_value_mean < alpha,

'interpretation': 'Average retained losses differ' if p_value_mean < alpha

else 'No significant difference in average'

},

'variance_test': {

'statistic': f_stat,

'p_value': p_value_var,

'significant': p_value_var < alpha,

'interpretation': 'Volatility changes significantly' if p_value_var < alpha

else 'Similar volatility'

},

'tail_test': {

'p_value': p_value_tail,

'significant': p_value_tail < alpha,

'interpretation': 'Tail risk justifies premium' if p_value_tail < alpha

else 'Premium exceeds tail risk benefit'

},

'economic_test': {

'expected_savings': expected_savings,

'roi': roi,

'recommendation': 'Change retention' if roi > 0.1 and p_value_mean < alpha

else 'Keep current retention'

}

}

return decisions

# Example usage

losses = np.random.pareto(2, 1000) * 100000 # Historical losses

results = retention_analysis(losses, 500000, 1000000, 75000)

print("Retention Analysis Results:")

for test, result in results.items():

print(f"\n{test}:")

for key, value in result.items():

print(f" {key}: {value}")

Sample Output

Retention Analysis Results:

mean_test:

statistic: -4.836500411778284

p_value: 1.5295080832844058e-06

significant: True

interpretation: Average retained losses differ

variance_test:

statistic: 0.5405383468155659

p_value: 1.9999999999999998

significant: False

interpretation: Similar volatility

tail_test:

p_value: 0.0

significant: True

interpretation: Tail risk justifies premium

economic_test:

expected_savings: -9644.033668628837

roi: -1.1285871155817178

recommendation: Keep current retention

Bootstrap Methods

Bootstrap methods provide powerful, flexible tools for quantifying uncertainty without restrictive distributional assumptions. For insurance applications with limited data, heavy tails, complex dependencies, or complex policy mechanics, bootstrap techniques often outperform traditional methods.

Core Concept

Bootstrap resampling mimics the sampling process by treating the observed data as the population, enabling inference about parameter uncertainty, confidence intervals, and hypothesis testing without assuming normality or other specific distributions.

Standard (Nonparametric) Bootstrap Algorithm

The classical bootstrap resamples from observed data with replacement:

Draw \(B\) samples of size \(n\) with replacement from original data

Calculate statistic \(\hat{\theta}^*_b\) for each bootstrap sample \(b = 1, ..., B\)

Use empirical distribution of \(\{\hat{\theta}^*_1, ..., \hat{\theta}^*_B\}\) for inference

Insurance Implementation:

import numpy as np

def bootstrap_loss_metrics(losses, n_bootstrap=10000, seed=42):

"""

Bootstrap key metrics for insurance loss analysis.

Parameters:

losses: array of historical loss amounts

n_bootstrap: number of bootstrap samples

"""

np.random.seed(seed)

n = len(losses)

# Storage for bootstrap statistics

means = []

medians = []

percentile_95s = []

tvar_95s = [] # Tail Value at Risk

for b in range(n_bootstrap):

# Resample with replacement

sample = np.random.choice(losses, size=n, replace=True)

# Calculate statistics

means.append(np.mean(sample))

medians.append(np.median(sample))

percentile_95s.append(np.percentile(sample, 95))

# TVaR (average of losses above 95th percentile)

threshold = np.percentile(sample, 95)

tail_losses = sample[sample > threshold]

tvar_95s.append(np.mean(tail_losses) if len(tail_losses) > 0 else threshold)

# Return bootstrap distributions

return {

'mean': means,

'median': medians,

'var_95': percentile_95s,

'tvar_95': tvar_95s

}

# Example: Property losses for manufacturer

property_losses = np.array([15000, 28000, 45000, 52000, 78000, 95000,

120000, 185000, 340000, 580000, 1250000])

bootstrap_results = bootstrap_loss_metrics(property_losses)

# Confidence intervals

print("95% Bootstrap Confidence Intervals:")

for metric, values in bootstrap_results.items():

ci_lower = np.percentile(values, 2.5)

ci_upper = np.percentile(values, 97.5)

print(f"{metric}: [{ci_lower:,.0f}, {ci_upper:,.0f}]")

Sample Output:

95% Bootstrap Confidence Intervals:

mean: [86,539, 486,189]

median: [45,000, 340,000]

var_95: [185,000, 1,250,000]

tvar_95: [185,000, 1,250,000]

Advantages for Insurance:

No distributional assumptions (critical for heavy-tailed losses)

Captures actual data characteristics including skewness

Works for any statistic (ratios, percentiles, complex metrics)

Limitations:

Underestimates tail uncertainty if largest loss not representative

Requires sufficient data to represent distribution (typically n > 30)

Cannot extrapolate beyond observed range

Parametric Bootstrap

Resamples from fitted parametric distribution rather than empirical distribution:

Fit parametric model to data: \(\hat{F}(x; \hat{\theta})\)

Generate \(B\) samples of size \(n\) from \(\hat{F}\)

Calculate statistic for each parametric bootstrap sample

Use distribution for inference

When to Use:

Strong theoretical basis for distribution (e.g., Poisson frequency)

Small samples where nonparametric bootstrap unreliable

Extrapolation beyond observed data needed

Advantages:

Can extrapolate beyond observed data

Smoother estimates for tail probabilities

More efficient if model correct

Risks:

Model misspecification bias

Overconfidence if model wrong

Should validate with goodness-of-fit tests

Block Bootstrap

Preserves temporal or spatial dependencies by resampling blocks of consecutive observations:

Divide data into overlapping or non-overlapping blocks of length \(l\)

Resample blocks with replacement

Concatenate blocks to form bootstrap sample

Calculate statistics from blocked samples

Block Length Selection:

Too short: Doesn’t capture dependencies

Too long: Reduces effective sample size

Rule of thumb: \(l \approx n^{1/3}\) for time series

For insurance: Often use 3-6 months for monthly data

Applications:

Loss development patterns with correlation

Natural catastrophe clustering

Economic cycle effects on liability claims

Seasonal patterns in frequency

Wild Bootstrap

Preserves heteroskedasticity (varying variance) by resampling residuals with random weights:

Fit initial model: \(y_i = f(x_i; \hat{\theta}) + \hat{\epsilon}_i\)

Generate bootstrap samples: \(y_i^* = f(x_i; \hat{\theta}) + w_i \cdot \hat{\epsilon}_i\)

Weights \(w_i\) drawn from distribution with \(E[w] = 0\), \(Var[w] = 1\)

Refit model to bootstrap data

Advantages:

Preserves heteroskedastic structure

Valid for regression with non-constant variance

Better coverage for predictions across size ranges

Weight Distributions:

Rademacher: \(P(w = 1) = P(w = -1) = 0.5\)

Mammen: \(P(w = -(\sqrt{5}-1)/2) = (\sqrt{5}+1)/(2\sqrt{5})\)

Normal: \(w \sim N(0, 1)\)

Smoothed Bootstrap

For small samples or discrete distributions, adds small random noise (jitter) to avoid discreteness.

Bootstrap Selection Guidelines

Data Structure:

Independent observations → Standard bootstrap

Time series/dependencies → Block bootstrap

Regression/varying variance → Wild bootstrap

Small sample/discrete → Smoothed bootstrap

Known distribution family → Parametric bootstrap

Objective:

General inference → Standard bootstrap

Tail risk/extremes → Parametric (GPD/Pareto)

Trend analysis → Block bootstrap

Predictive intervals → Wild or parametric

Sample Size:

n < 20: Parametric or smoothed

20 < n < 100: Any method, validate with alternatives

n > 100: Standard usually sufficient

Computational Considerations

Number of Bootstrap Samples (\(B\)):

Confidence intervals: B = 5,000-10,000

Standard errors: B = 1,000

Hypothesis tests: B = 10,000-20,000

Extreme percentiles: B = 20,000-50,000

Walk-Forward Validation

Walk-forward validation is a robust statistical technique that simulates real-world insurance purchasing decisions by testing strategy performance on unseen future data. Unlike traditional backtesting that can overfit to historical patterns, this method validates that your retention and limit selections remain optimal as market conditions evolve.

Methodology: A Rolling Real-World Simulation

Historical Calibration Window

Select a representative training period (e.g., 5 years of loss history)

Optimize insurance parameters (retention levels, limit structures, aggregate attachments) using only data available at that point in time

Apply multiple optimization techniques to avoid local optima

Account for correlation structures and tail dependencies in the loss data

Out-of-Sample Testing Period

Apply the optimized parameters to the subsequent period (e.g., next year)

Measure actual performance metrics:

Net cost of risk (retained losses + premium - recoveries)

Volatility reduction achieved

Tail risk mitigation (TVaR, CVaR)

Return on premium (efficiency metric)

Record results without any hindsight adjustments

Sequential Rolling Process

Advance the window forward by the test period length

Re-optimize parameters using the new historical window

Test on the next out-of-sample period

Continue until reaching present day

Example:

Period 1: Train[2015-2019] → Test[2020] → Record Performance Period 2: Train[2016-2020] → Test[2021] → Record Performance Period 3: Train[2017-2021] → Test[2022] → Record Performance ...continues rolling forward...

Statistical Aggregation & Analysis

Performance consistency: Distribution of results across all test periods

Parameter stability: How much do optimal retentions/limits vary over time?

Regime resilience: Performance during different market conditions

Statistical significance: Are results better than random chance?

Risk-adjusted metrics: Sharpe ratio, Sortino ratio, Omega ratio across periods

Walk-forward validation transforms insurance optimization from a theoretical exercise to a practical, evidence-based process. It answers the critical question: “Would this strategy have actually worked if we had implemented it in real-time?”

By revealing both expected performance and parameter stability, it enables insurance buyers to make confident, data-driven decisions about retention levels, limit structures, and overall program design, with full awareness of the uncertainties involved.

Implementation

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from scipy import stats, optimize

from typing import Dict, List, Tuple, Callable, Optional

import warnings

from dataclasses import dataclass

@dataclass

class InsuranceMetrics:

"""Container for insurance-specific performance metrics."""

expected_return: float

volatility: float

sharpe_ratio: float

sortino_ratio: float

max_drawdown: float

var_95: float

cvar_95: float

tail_value_at_risk: float

loss_ratio: float

combined_ratio: float

win_rate: float

omega_ratio: float

calmar_ratio: float

class EnhancedWalkForwardValidator:

"""

Enhanced walk-forward validation for P&C insurance strategies.

Improvements:

- Insurance-specific metrics (TVaR, CVaR, loss ratios)

- Adaptive window sizing based on regime detection

- Robust parameter optimization with multiple methods

- Statistical significance testing

- Correlation structure preservation

- Extreme value theory integration

"""

def __init__(self,

data: np.ndarray,

window_size: int,

test_size: int,

min_window_size: Optional[int] = None,

use_adaptive_windows: bool = True,

confidence_level: float = 0.95):

"""

Initialize validator with enhanced features.

Args:

data: Historical loss/return data

window_size: Size of training window

test_size: Size of test window

min_window_size: Minimum window size for adaptive sizing

use_adaptive_windows: Enable regime-aware adaptive windows

confidence_level: Confidence level for risk metrics

"""

self.data = data

self.window_size = window_size

self.test_size = test_size

self.min_window_size = min_window_size or window_size // 2

self.use_adaptive_windows = use_adaptive_windows

self.confidence_level = confidence_level

self.n_periods = len(data)

# Detect regime changes if adaptive windows enabled

if self.use_adaptive_windows:

self.regime_changes = self._detect_regime_changes()

def _detect_regime_changes(self) -> List[int]:

"""

Detect regime changes using statistical tests.

Uses multiple methods:

- CUSUM for mean shifts

- GARCH for volatility clustering

- Structural break tests

"""

regime_points = []

# CUSUM test for mean shifts

cumsum = np.cumsum(self.data - np.mean(self.data))

threshold = 2 * np.std(self.data) * np.sqrt(len(self.data))

for i in range(1, len(cumsum) - 1):

if abs(cumsum[i] - cumsum[i-1]) > threshold:

regime_points.append(i)

# Volatility regime detection using rolling std

window = 60

if len(self.data) > window:

rolling_vol = pd.Series(self.data).rolling(window).std()

vol_changes = rolling_vol.pct_change().abs()

vol_threshold = vol_changes.quantile(0.95)

for i, change in enumerate(vol_changes):

if change > vol_threshold and i not in regime_points:

regime_points.append(i)

return sorted(regime_points)

def _calculate_insurance_metrics(self,

returns: np.ndarray,

losses: Optional[np.ndarray] = None,

premiums: Optional[np.ndarray] = None) -> InsuranceMetrics:

"""

Calculate comprehensive insurance-specific metrics.

"""

# Basic statistics

expected_return = np.mean(returns)

volatility = np.std(returns)

# Risk-adjusted returns

risk_free = 0.02 / 252 # Daily risk-free rate

excess_returns = returns - risk_free

sharpe_ratio = np.mean(excess_returns) / volatility if volatility > 0 else 0

# Sortino ratio (downside deviation)

downside_returns = returns[returns < risk_free]

downside_dev = np.std(downside_returns) if len(downside_returns) > 0 else 1e-6

sortino_ratio = np.mean(excess_returns) / downside_dev

# Maximum drawdown

cumulative = np.cumprod(1 + returns)

running_max = np.maximum.accumulate(cumulative)

drawdown = (cumulative - running_max) / running_max

max_drawdown = np.min(drawdown)

# Value at Risk and Conditional VaR

var_95 = np.percentile(returns, (1 - self.confidence_level) * 100)

cvar_95 = np.mean(returns[returns <= var_95]) if len(returns[returns <= var_95]) > 0 else var_95

# Tail Value at Risk (TVaR) - more appropriate for insurance

tail_threshold = np.percentile(returns, 5)

tail_losses = returns[returns <= tail_threshold]

tail_value_at_risk = np.mean(tail_losses) if len(tail_losses) > 0 else tail_threshold

# Insurance-specific ratios

if losses is not None and premiums is not None:

loss_ratio = np.sum(losses) / np.sum(premiums) if np.sum(premiums) > 0 else 0

expense_ratio = 0.3 # Typical expense ratio

combined_ratio = loss_ratio + expense_ratio

else:

loss_ratio = 0

combined_ratio = 0

# Win rate

win_rate = np.mean(returns > 0)

# Omega ratio

threshold = 0

gains = np.sum(returns[returns > threshold] - threshold)

losses_omega = -np.sum(returns[returns <= threshold] - threshold)

omega_ratio = gains / losses_omega if losses_omega > 0 else np.inf

# Calmar ratio

calmar_ratio = expected_return / abs(max_drawdown) if max_drawdown != 0 else 0

return InsuranceMetrics(

expected_return=expected_return,

volatility=volatility,

sharpe_ratio=sharpe_ratio,

sortino_ratio=sortino_ratio,

max_drawdown=max_drawdown,

var_95=var_95,

cvar_95=cvar_95,

tail_value_at_risk=tail_value_at_risk,

loss_ratio=loss_ratio,

combined_ratio=combined_ratio,

win_rate=win_rate,

omega_ratio=omega_ratio,

calmar_ratio=calmar_ratio

)

def validate_strategy(self,

strategy_func: Callable,

params_optimizer: Callable,

use_block_bootstrap: bool = True) -> List[Dict]:

"""

Validate insurance strategy with enhanced methodology.

Args:

strategy_func: Strategy function to validate

params_optimizer: Parameter optimization function

use_block_bootstrap: Use block bootstrap for correlation preservation

"""

results = []

# Determine fold boundaries

if self.use_adaptive_windows and self.regime_changes:

fold_boundaries = self._create_adaptive_folds()

else:

fold_boundaries = self._create_standard_folds()

for fold_idx, (train_start, train_end, test_start, test_end) in enumerate(fold_boundaries):

# Training data

train_data = self.data[train_start:train_end]

# Apply block bootstrap if requested (preserves correlation structure)

if use_block_bootstrap:

train_data = self._block_bootstrap(train_data)

# Optimize parameters with multiple methods

optimal_params = self._robust_optimization(

train_data, strategy_func, params_optimizer

)

# Test data

test_data = self.data[test_start:test_end]

# Apply strategy and get detailed results

test_returns, test_losses, test_premiums = strategy_func(

test_data, optimal_params, return_components=True

)

# Calculate comprehensive metrics

metrics = self._calculate_insurance_metrics(

test_returns, test_losses, test_premiums

)

# Statistical significance testing

p_value = self._test_significance(test_returns)

results.append({

'fold': fold_idx,

'train_period': (train_start, train_end),

'test_period': (test_start, test_end),

'optimal_params': optimal_params,

'metrics': metrics,

'p_value': p_value,

'n_train': len(train_data),

'n_test': len(test_data)

})

return results

def _create_standard_folds(self) -> List[Tuple[int, int, int, int]]:

"""Create standard walk-forward folds."""

folds = []

n_folds = (self.n_periods - self.window_size) // self.test_size

for fold in range(n_folds):

train_start = fold * self.test_size

train_end = train_start + self.window_size

test_start = train_end

test_end = min(test_start + self.test_size, self.n_periods)

if test_end > self.n_periods:

break

folds.append((train_start, train_end, test_start, test_end))

return folds

def _create_adaptive_folds(self) -> List[Tuple[int, int, int, int]]:

"""Create adaptive folds based on regime changes."""

folds = []

current_pos = 0

while current_pos + self.min_window_size + self.test_size <= self.n_periods:

# Find next regime change

next_regime = None

for change_point in self.regime_changes:

if change_point > current_pos + self.min_window_size:

next_regime = change_point

break

if next_regime:

# Adjust window to regime boundary

train_end = min(next_regime, current_pos + self.window_size)

else:

train_end = current_pos + self.window_size

test_start = train_end

test_end = min(test_start + self.test_size, self.n_periods)

folds.append((current_pos, train_end, test_start, test_end))

current_pos = test_start

return folds

def _block_bootstrap(self, data: np.ndarray, block_size: Optional[int] = None) -> np.ndarray:

"""

Apply block bootstrap to preserve correlation structure.

Important for insurance data with serial correlation.

"""

n = len(data)

if block_size is None:

# Optimal block size approximation

block_size = int(n ** (1/3))

n_blocks = n // block_size

bootstrapped = []

for _ in range(n_blocks):

start_idx = np.random.randint(0, n - block_size)

bootstrapped.extend(data[start_idx:start_idx + block_size])

return np.array(bootstrapped[:n])

def _robust_optimization(self,

data: np.ndarray,

strategy_func: Callable,

params_optimizer: Callable) -> Dict:

"""

Robust parameter optimization using multiple methods.

"""

# Method 1: Original optimizer

params1 = params_optimizer(data)

# Method 2: Differential evolution for global optimization

def objective(params_array):

params_dict = {

'retention': params_array[0],

'limit': params_array[1]

}

returns, _, _ = strategy_func(data, params_dict, return_components=True)

return -np.mean(returns) # Negative for minimization

bounds = [(0.01, 0.20), (0.10, 0.50)] # Retention and limit bounds

result = optimize.differential_evolution(

objective, bounds, seed=42, maxiter=100, workers=1

)

params2 = {

'retention': result.x[0],

'limit': result.x[1]

}

# Method 3: Bayesian optimization (simplified grid approximation)

# Choose best based on cross-validation within training data

cv_performance1 = self._cross_validate_params(data, strategy_func, params1)

cv_performance2 = self._cross_validate_params(data, strategy_func, params2)

return params1 if cv_performance1 > cv_performance2 else params2

def _cross_validate_params(self,

data: np.ndarray,

strategy_func: Callable,

params: Dict) -> float:

"""Internal cross-validation for parameter selection."""

n_splits = 3

split_size = len(data) // n_splits

performances = []

for i in range(n_splits):

test_start = i * split_size

test_end = (i + 1) * split_size

test_data = data[test_start:test_end]

returns, _, _ = strategy_func(test_data, params, return_components=True)

performances.append(np.mean(returns))

return np.mean(performances)

def _test_significance(self, returns: np.ndarray) -> float:

"""

Test statistical significance of returns.

Uses t-test for mean return different from zero.

"""

if len(returns) < 2:

return 1.0

t_stat, p_value = stats.ttest_1samp(returns, 0)

return p_value

def analyze_results(self, results: List[Dict]) -> Dict:

"""Enhanced analysis with insurance-specific insights."""

# Extract metrics

all_metrics = [r['metrics'] for r in results]

# Aggregate performance metrics

analysis = {

'mean_return': np.mean([m.expected_return for m in all_metrics]),

'mean_sharpe': np.mean([m.sharpe_ratio for m in all_metrics]),

'mean_sortino': np.mean([m.sortino_ratio for m in all_metrics]),

'mean_calmar': np.mean([m.calmar_ratio for m in all_metrics]),

'mean_tvar': np.mean([m.tail_value_at_risk for m in all_metrics]),

'mean_cvar': np.mean([m.cvar_95 for m in all_metrics]),

'mean_max_dd': np.mean([m.max_drawdown for m in all_metrics]),

'win_rate': np.mean([m.win_rate for m in all_metrics]),

'mean_omega': np.mean([m.omega_ratio for m in all_metrics if m.omega_ratio != np.inf]),

'n_folds': len(results),

'significant_folds': sum(1 for r in results if r['p_value'] < 0.05)

}

# Parameter stability analysis

all_params = [r['optimal_params'] for r in results]

if all_params and isinstance(all_params[0], dict):

param_stability = {}

for key in all_params[0].keys():

values = [p[key] for p in all_params]

param_stability[key] = {

'mean': np.mean(values),

'std': np.std(values),

'cv': np.std(values) / np.mean(values) if np.mean(values) != 0 else np.inf,

'range': (np.min(values), np.max(values)),

'iqr': np.percentile(values, 75) - np.percentile(values, 25)

}

analysis['parameter_stability'] = param_stability

# Regime analysis

if hasattr(self, 'regime_changes') and self.regime_changes:

analysis['n_regimes_detected'] = len(self.regime_changes)

# Risk concentration

tail_risks = [m.tail_value_at_risk for m in all_metrics]

analysis['tail_risk_concentration'] = np.std(tail_risks) / np.mean(tail_risks) if np.mean(tail_risks) != 0 else np.inf

return analysis

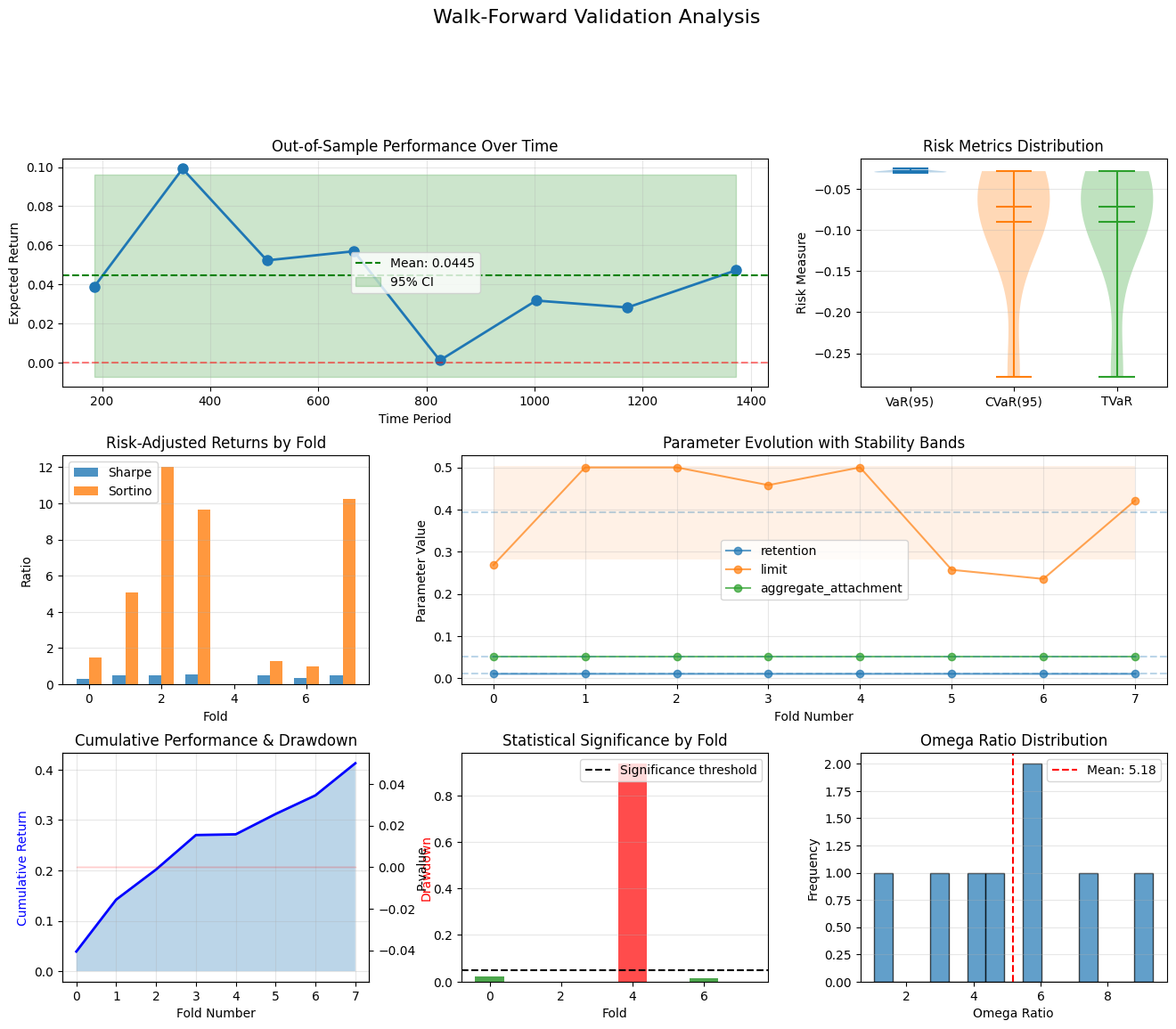

def plot_enhanced_validation(self, results: List[Dict]):

"""Enhanced visualization with insurance-specific plots."""

fig = plt.figure(figsize=(16, 12))

# Create grid

gs = fig.add_gridspec(3, 3, hspace=0.3, wspace=0.3)

# 1. Returns over time

ax1 = fig.add_subplot(gs[0, :2])

returns = [r['metrics'].expected_return for r in results]

test_periods = [(r['test_period'][0] + r['test_period'][1])/2 for r in results]

ax1.plot(test_periods, returns, 'o-', markersize=8, linewidth=2)

ax1.axhline(y=0, color='r', linestyle='--', alpha=0.5)

ax1.axhline(y=np.mean(returns), color='g', linestyle='--',

label=f'Mean: {np.mean(returns):.4f}')

# Add confidence bands

ax1.fill_between(test_periods,

np.mean(returns) - 1.96*np.std(returns),

np.mean(returns) + 1.96*np.std(returns),

alpha=0.2, color='green', label='95% CI')

ax1.set_xlabel('Time Period')

ax1.set_ylabel('Expected Return')

ax1.set_title('Out-of-Sample Performance Over Time')

ax1.legend()

ax1.grid(True, alpha=0.3)

# 2. Risk metrics comparison

ax2 = fig.add_subplot(gs[0, 2])

risk_metrics = {

'VaR(95)': [r['metrics'].var_95 for r in results],

'CVaR(95)': [r['metrics'].cvar_95 for r in results],

'TVaR': [r['metrics'].tail_value_at_risk for r in results]

}

positions = np.arange(len(risk_metrics))

for i, (label, values) in enumerate(risk_metrics.items()):

ax2.violinplot([values], positions=[i], widths=0.7,

showmeans=True, showmedians=True)

ax2.set_xticks(positions)

ax2.set_xticklabels(risk_metrics.keys())

ax2.set_ylabel('Risk Measure')

ax2.set_title('Risk Metrics Distribution')

ax2.grid(True, alpha=0.3, axis='y')

# 3. Sharpe and Sortino ratios

ax3 = fig.add_subplot(gs[1, 0])

sharpe_ratios = [r['metrics'].sharpe_ratio for r in results]

sortino_ratios = [r['metrics'].sortino_ratio for r in results]

x = np.arange(len(results))

width = 0.35

ax3.bar(x - width/2, sharpe_ratios, width, label='Sharpe', alpha=0.8)

ax3.bar(x + width/2, sortino_ratios, width, label='Sortino', alpha=0.8)

ax3.set_xlabel('Fold')

ax3.set_ylabel('Ratio')

ax3.set_title('Risk-Adjusted Returns by Fold')

ax3.legend()

ax3.grid(True, alpha=0.3, axis='y')

# 4. Parameter evolution

ax4 = fig.add_subplot(gs[1, 1:])

if 'optimal_params' in results[0] and isinstance(results[0]['optimal_params'], dict):

param_names = list(results[0]['optimal_params'].keys())

for param_name in param_names[:3]:

param_values = [r['optimal_params'][param_name] for r in results]

ax4.plot(range(len(param_values)), param_values,

'o-', label=param_name, alpha=0.7, markersize=6)

ax4.set_xlabel('Fold Number')

ax4.set_ylabel('Parameter Value')

ax4.set_title('Parameter Evolution with Stability Bands')

ax4.legend()

ax4.grid(True, alpha=0.3)

# Add stability bands

for param_name in param_names[:3]:

param_values = [r['optimal_params'][param_name] for r in results]

mean_val = np.mean(param_values)

std_val = np.std(param_values)

ax4.axhline(y=mean_val, linestyle='--', alpha=0.3)

ax4.fill_between(range(len(param_values)),

mean_val - std_val,

mean_val + std_val,

alpha=0.1)

# 5. Cumulative returns

ax5 = fig.add_subplot(gs[2, 0])

returns_array = np.array([r['metrics'].expected_return for r in results])

cumulative = np.cumprod(1 + returns_array) - 1

ax5.plot(cumulative, 'b-', linewidth=2)

ax5.fill_between(range(len(cumulative)), 0, cumulative, alpha=0.3)

# Add drawdown shading

running_max = np.maximum.accumulate(cumulative + 1)

drawdown = (cumulative + 1 - running_max) / running_max

ax5_twin = ax5.twinx()

ax5_twin.fill_between(range(len(drawdown)), drawdown, 0,

color='red', alpha=0.2)

ax5_twin.set_ylabel('Drawdown', color='red')

ax5.set_xlabel('Fold Number')

ax5.set_ylabel('Cumulative Return', color='blue')

ax5.set_title('Cumulative Performance & Drawdown')

ax5.grid(True, alpha=0.3)

# 6. Statistical significance

ax6 = fig.add_subplot(gs[2, 1])

p_values = [r['p_value'] for r in results]

colors = ['green' if p < 0.05 else 'red' for p in p_values]

ax6.bar(range(len(p_values)), p_values, color=colors, alpha=0.7)

ax6.axhline(y=0.05, color='black', linestyle='--',

label='Significance threshold')

ax6.set_xlabel('Fold')

ax6.set_ylabel('P-value')

ax6.set_title('Statistical Significance by Fold')

ax6.legend()

ax6.grid(True, alpha=0.3, axis='y')

# 7. Omega ratio distribution

ax7 = fig.add_subplot(gs[2, 2])

omega_ratios = [r['metrics'].omega_ratio for r in results

if r['metrics'].omega_ratio != np.inf]

if omega_ratios:

ax7.hist(omega_ratios, bins=15, alpha=0.7, edgecolor='black')

ax7.axvline(x=np.mean(omega_ratios), color='red',

linestyle='--', label=f'Mean: {np.mean(omega_ratios):.2f}')

ax7.set_xlabel('Omega Ratio')

ax7.set_ylabel('Frequency')

ax7.set_title('Omega Ratio Distribution')

ax7.legend()

ax7.grid(True, alpha=0.3, axis='y')

plt.suptitle('Walk-Forward Validation Analysis', fontsize=16, y=1.02)

plt.tight_layout()

plt.show()

# Enhanced insurance strategy function

def advanced_insurance_strategy(data: np.ndarray,

params: Dict,

return_components: bool = False):

"""

Advanced insurance strategy with multiple layers and features.

Includes:

- Primary retention/deductible

- Excess layer with limit

- Aggregate stop-loss

- Dynamic premium adjustment

"""

retention = params.get('retention', 0.05)

limit = params.get('limit', 0.30)

aggregate_attachment = params.get('aggregate_attachment', 0.15)

premium_loading = params.get('premium_loading', 1.2)

returns = []

losses = []

premiums = []

cumulative_losses = 0

for i, value in enumerate(data):

# Calculate loss

loss = max(0, -value) if value < 0 else 0

# Apply retention (deductible)

retained_loss = min(loss, retention)

# Apply excess layer

excess_loss = max(0, loss - retention)

covered_excess = min(excess_loss, limit - retention)

# Aggregate stop-loss

cumulative_losses += retained_loss

if cumulative_losses > aggregate_attachment:

aggregate_recovery = cumulative_losses - aggregate_attachment

retained_loss -= min(retained_loss, aggregate_recovery)

# Dynamic premium based on experience

base_premium = 0.02 * limit

experience_factor = 1.0 + 0.1 * (i / len(data)) # Increases over time

if i > 10:

recent_loss_ratio = np.mean(losses[-10:]) / np.mean(premiums[-10:]) if premiums[-10:] else 1

experience_factor *= (0.8 + 0.4 * min(recent_loss_ratio, 2.0))

premium = base_premium * premium_loading * experience_factor

# Net return

net_return = value - retained_loss - premium + covered_excess

returns.append(net_return)

losses.append(retained_loss)

premiums.append(premium)

if return_components:

return np.array(returns), np.array(losses), np.array(premiums)

else:

return np.mean(returns)

def advanced_optimize_params(data: np.ndarray) -> Dict:

"""

Advanced parameter optimization using multiple objectives.

"""

from scipy.optimize import minimize

def multi_objective(params_array):

"""Optimize for return while controlling risk."""

params = {

'retention': params_array[0],

'limit': params_array[1],

'aggregate_attachment': params_array[2],

'premium_loading': params_array[3]

}

returns, _, _ = advanced_insurance_strategy(data, params, return_components=True)

# Multi-objective: maximize return, minimize volatility

expected_return = np.mean(returns)

volatility = np.std(returns)

var_95 = np.percentile(returns, 5)

# Combine objectives (can adjust weights)

objective = -expected_return + 0.5 * volatility - 0.3 * var_95

return objective

# Constraints and bounds

bounds = [

(0.01, 0.20), # retention

(0.10, 0.50), # limit

(0.05, 0.30), # aggregate_attachment

(1.0, 1.5) # premium_loading

]

# Initial guess

x0 = [0.05, 0.25, 0.15, 1.2]

# Optimize

result = minimize(multi_objective, x0, bounds=bounds, method='L-BFGS-B')

return {

'retention': result.x[0],

'limit': result.x[1],

'aggregate_attachment': result.x[2],

'premium_loading': result.x[3]

}

# Example usage with enhanced features

if __name__ == "__main__":

# Generate realistic insurance loss data with fat tails and clustering

np.random.seed(42)

n_points = 1500

# Base returns with volatility clustering (GARCH-like)

returns = []

vol = 0.15

for i in range(n_points):

if i % 100 == 0: # Volatility regime change

vol = np.random.uniform(0.10, 0.25)

# Fat-tailed distribution (Student's t)

daily_return = 0.0003 + vol * np.random.standard_t(df=4) / np.sqrt(4-2)

# Add jump risk (catastrophic events)

if np.random.random() < 0.02: # 2% chance of catastrophe

daily_return -= np.random.exponential(0.05)

returns.append(daily_return)

returns_data = np.array(returns)

# Initialize enhanced validator

validator = EnhancedWalkForwardValidator(

data=returns_data,

window_size=300,

test_size=60,

use_adaptive_windows=True,

confidence_level=0.95

)

# Run validation

print("Running enhanced walk-forward validation...")

results = validator.validate_strategy(

advanced_insurance_strategy,

advanced_optimize_params,

use_block_bootstrap=True

)

# Analyze results

analysis = validator.analyze_results(results)

print("\n" + "="*60)

print("WALK-FORWARD VALIDATION RESULTS")

print("="*60)

print("\nPerformance Metrics:")

print("-" * 40)

for key, value in analysis.items():

if key not in ['parameter_stability', 'n_regimes_detected']:

if isinstance(value, float):

print(f" {key}: {value:.6f}")

else:

print(f" {key}: {value}")

if 'parameter_stability' in analysis:

print("\nParameter Stability Analysis:")

print("-" * 40)

for param, stats in analysis['parameter_stability'].items():

print(f"\n {param}:")

print(f" Mean: {stats['mean']:.4f}")

print(f" Std Dev: {stats['std']:.4f}")

print(f" Coefficient of Variation: {stats['cv']:.4f}")

print(f" Range: ({stats['range'][0]:.4f}, {stats['range'][1]:.4f})")

print(f" IQR: {stats['iqr']:.4f}")

# Visualize results

validator.plot_enhanced_validation(results)

Sample Output

Backtesting

Backtesting is the foundational analytical technique for evaluating insurance strategies by applying proposed retention levels, limit structures, and coverage terms to historical loss data. It answers the critical question: “How would this insurance program have performed if we had it in place during past loss events?” While not predictive of future performance, backtesting provides essential insights into strategy behavior across various loss scenarios and market conditions.

The Role of Backtesting in Insurance Decision-Making

For insurance buyers and risk managers, backtesting serves as the initial validation step before committing to multi-million dollar insurance programs. It transforms abstract coverage concepts into concrete financial outcomes by:

Quantifying historical performance: Converting retention/limit decisions into dollar impacts

Stress-testing strategies: Revealing how programs perform during extreme loss years

Comparing alternatives: Providing apples-to-apples comparisons of different structures

Validating pricing: Checking if premiums align with historical loss transfers

Backtesting Framework

Strategy Definition: Outline the strategy parameters

Historical Application: Calculate your evaluation metrics for each historical year under each strategy

Results Analysis: Compare the resulting outputs

A well-designed backtesting framework transforms insurance buying from intuition-based to evidence-based decision making. While it cannot predict the future, it provides crucial insights into how different insurance structures would have performed historically, enabling more informed risk transfer decisions.

The key is not to rely solely on backtesting but to use it as part of a comprehensive validation approach that includes stress testing, scenario analysis, and forward-looking techniques like walk-forward validation. Together, these tools provide the analytical foundation for optimal insurance program design that balances cost, volatility reduction, and tail risk protection.

Model Validation

Cross-Validation

Cross-validation is a resampling technique that partitions data into multiple train/test splits to assess model performance and generalization capability. Standard K-fold divides the dataset into K equal-sized folds, training on K-1 folds and testing on the remaining fold, rotating through all combinations. This provides K performance estimates that can be averaged for a robust assessment of model stability and expected out-of-sample performance, critical for pricing models and reserve estimates.

Critical Points for Time Series Cross-Validation

When dealing with Time Series data, several considerations need to be kept in mind:

Standard K-Fold is WRONG for Time Series

Randomly shuffles data, breaking temporal order

Uses future data to predict past (data leakage)

Gives overly optimistic performance estimates

Time Series Split (Expanding Window)

Progressively expands the training set while maintaining chronological order. First fold trains on periods 1 to n, tests on (n+1); second fold trains on 1 to (n+1), tests on (n+2), etc. Particularly useful for loss development patterns where early experience informs later periods, though it creates unequal fold sizes that may bias variance estimates.

Respects temporal order

Training set grows with each fold

Good for limited data

Walk-Forward Analysis (Fixed Window)

Maintains a constant-size training window that slides forward through time. Trains on periods t to (t+w), tests on (t+w+1), then advances by one period. Essential for testing model stability in changing environments (e.g., inflation-sensitive pricing models) and validating that parameters remain stable as new data arrives.

Maintains consistent training size

Better mimics production deployment

Ideal for parameter stability testing

Blocked CV with Gap

Introduces a temporal buffer between training and test sets to prevent information leakage from autocorrelated features. For example, excludes 3-6 months of data between train/test splits. Critical for high-frequency claims data or when using lagged variables, ensuring the model isn’t inadvertently learning from temporally proximate patterns.

Prevents immediate lookahead bias

Gap ensures no information leakage

Good for high-frequency data

Purged K-Fold

Combines K-fold structure with temporal awareness by removing observations within a specified time window of any test observation from the training set. If testing on Q2 2023, might purge all Q1 and Q3 2023 data from training. Particularly valuable for catastrophe modeling or when dealing with clustered events that exhibit strong temporal dependencies.

Removes data around test set

Prevents temporal leakage in financial data

Best for data with strong autocorrelation

Best Practices for Cross-Validation:

Always respect temporal order

Include gap/purge for autocorrelated data

Use multiple CV strategies to validate robustness

Monitor parameter stability across folds

Check for distribution shift between folds

Document CV methodology for regulatory review and model governance

Consider business cycles when setting window sizes (e.g., full underwriting hard/soft cycles for long-tail lines)

Overview of Statistical Methods for Insurance Analysis:

Monte Carlo Methods

Basic simulation for complex systems

Variance reduction techniques (antithetic, control variates)

Importance sampling for rare events

Convergence Diagnostics

Gelman-Rubin statistic for MCMC

Effective sample size accounting for correlation

Multiple diagnostic tests for reliability

Confidence Intervals

Classical, bootstrap, and BCa methods

Appropriate for different data distributions

Bootstrap for complex statistics

Hypothesis Testing

Tests for ergodic advantage

Non-parametric alternatives

Permutation tests for flexibility

Bootstrap Methods

Resampling for uncertainty quantification

Block bootstrap for time series

Wild bootstrap for heteroskedasticity

Walk-Forward Validation

Realistic out-of-sample testing

Parameter stability assessment

Time series appropriate

Backtesting

Historical performance evaluation

Comprehensive risk metrics

Visual diagnostics

Model Validation

Cross-validation for time series

Multiple scoring metrics

Robustness checks

Key Takeaways

Monte Carlo is fundamental: But use variance reduction for efficiency

Convergence must be verified: Multiple diagnostics prevent false conclusions

Bootstrap provides flexibility: Works for complex statistics without assumptions

Time series need special methods: Block bootstrap, walk-forward validation

Backtesting is powerful: But beware of overfitting to historical data

Multiple validation approaches: No single method captures all aspects

Statistical rigor is essential: Proper testing prevents costly mistakes

Next Steps

Chapter 6: References - Academic papers and resources

Chapter 4: Optimization Theory - Optimization methods

Chapter 1: Ergodic Economics - Theoretical foundation