Architectural Diagrams

This section provides comprehensive architectural visualizations of the Ergodic Insurance Limits system using interactive Mermaid diagrams. These diagrams illustrate the system’s structure, module relationships, data flows, and design patterns.

Note

The diagrams are interactive - you can zoom, pan, and click on elements for better viewing. If diagrams don’t render properly, try refreshing the page or viewing in a modern browser.

Understanding the Notation

Boxes: Represent classes, modules, or components

Arrows: Show dependencies, data flow, or relationships

Colors: Group related components (consistent across diagrams)

Labels: Describe the nature of relationships

Overview

The architecture documentation is organized into three main categories:

System-Level Views - High-level architecture and module relationships

Class Diagrams - Detailed class structures and interactions

Data Flow Patterns - How information moves through the system

High-Level System Context

The system context diagram shows the overall architecture, including all major components, external systems, and data flows. The system is organized into 9 major subsystems with over 50 modules.

High-Level System Context Diagram

Executive Summary

The Ergodic Insurance Limits framework analyzes insurance decisions using time-average (ergodic) theory rather than traditional ensemble averages. This approach reveals that insurance can enhance business growth even when premiums exceed expected losses by 200-500%, transforming insurance from a cost center to a growth enabler.

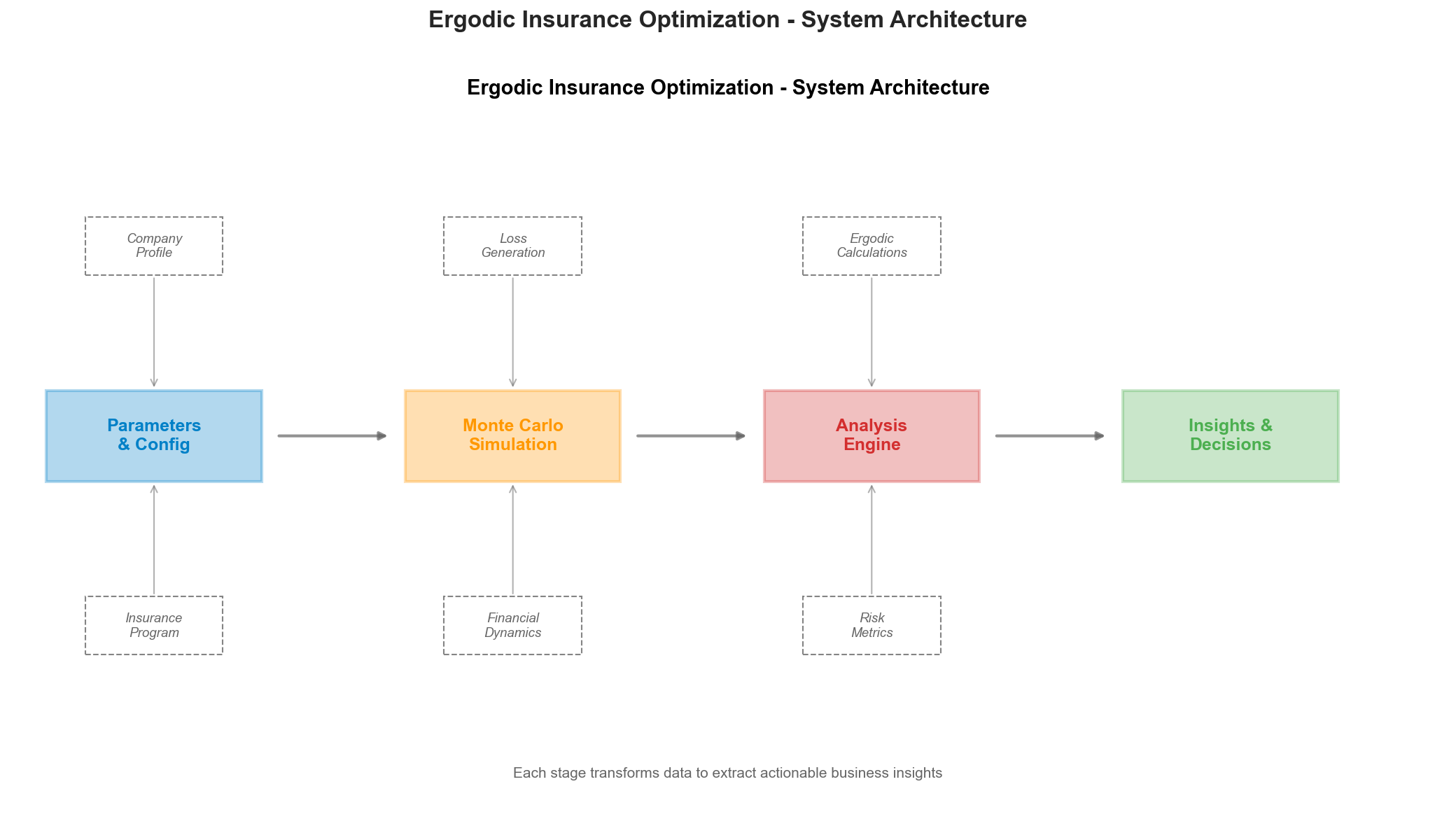

Simplified System Architecture

flowchart LR

%% Simplified Executive View

INPUT[("📊 Market Data<br/>& Configuration")]

BUSINESS[("🏭 Business<br/>Simulation")]

ERGODIC[("📈 Ergodic<br/>Analysis")]

OPTIMIZE[("🎯 Strategy<br/>Optimization")]

OUTPUT[("📑 Reports &<br/>Insights")]

INPUT --> BUSINESS

BUSINESS --> ERGODIC

ERGODIC --> OPTIMIZE

OPTIMIZE --> OUTPUT

%% Styling

classDef inputStyle fill:#e3f2fd,stroke:#0d47a1,stroke-width:3px,font-size:14px

classDef processStyle fill:#f3e5f5,stroke:#4a148c,stroke-width:3px,font-size:14px

classDef outputStyle fill:#e8f5e9,stroke:#1b5e20,stroke-width:3px,font-size:14px

class INPUT inputStyle

class BUSINESS,ERGODIC,OPTIMIZE processStyle

class OUTPUT outputStyle

Key Innovation: By comparing time-average growth (what one business experiences over time) with ensemble-average growth (statistical average across many businesses), the framework demonstrates that insurance fundamentally transforms the growth dynamics of volatile businesses.

System Architecture Overview (Detailed)

The actual implementation follows a sophisticated multi-layer architecture:

graph TB

%% Input Layer

subgraph Inputs["📥 Input Layer"]

CONF["Configuration<br/>(YAML/JSON)"]

HIST["Historical Loss Data"]

PARAMS["Business Parameters"]

end

%% Core Simulation

subgraph Core["⚙️ Core Simulation Engine"]

MANU["WidgetManufacturer<br/>(Business Model)"]

CLAIM["ClaimGenerator<br/>(Loss Events)"]

INS["InsuranceProgram<br/>(Coverage Tower)"]

SIM["Simulation Engine<br/>(Time Evolution)"]

end

%% Analysis Layer

subgraph Analysis["📊 Analysis & Optimization"]

MONTE["Monte Carlo Engine<br/>(10,000+ paths)"]

ERGODIC["Ergodic Analyzer<br/>(Time vs Ensemble)"]

OPT["Business Optimizer<br/>(Strategy Selection)"]

SENS["Sensitivity Analysis<br/>(Parameter Impact)"]

end

%% Output Layer

subgraph Outputs["📤 Output & Insights"]

EXCEL["Excel Reports<br/>(Detailed Results)"]

VIZ["Visualizations<br/>(Executive & Technical)"]

METRICS["Risk Metrics<br/>(VaR, CVaR, Ruin Prob)"]

STRATEGY["Optimal Strategy<br/>(Limits & Retentions)"]

end

%% Data Flow

Inputs --> Core

Core --> MONTE

MONTE --> Analysis

Analysis --> Outputs

%% Key Connections

MANU -.-> INS

CLAIM -.-> INS

INS -.-> SIM

SIM -.-> MONTE

ERGODIC -.-> OPT

OPT -.-> SENS

classDef inputClass fill:#e3f2fd,stroke:#1565c0

classDef coreClass fill:#fff3e0,stroke:#ef6c00

classDef analysisClass fill:#f3e5f5,stroke:#7b1fa2

classDef outputClass fill:#e8f5e9,stroke:#2e7d32

class CONF,HIST,PARAMS inputClass

class MANU,CLAIM,INS,SIM coreClass

class MONTE,ERGODIC,OPT,SENS analysisClass

class EXCEL,VIZ,METRICS,STRATEGY outputClass

Reference to System Architecture Diagram

For a visual representation, see: assets/system_architecture.png

{kind=link}

The PNG diagram shows the simplified flow, while the detailed architecture above reflects the actual implementation with all major components.

Detailed System Architecture

This diagram shows the overall architecture of the Ergodic Insurance Limits framework, including the main components, external dependencies, and data flow between major modules.

flowchart TB

%% External Inputs and Configurations

subgraph External["External Inputs"]

CONFIG[("Configuration Files<br/>YAML/JSON")]

MARKET[("Market Data<br/>Loss Distributions")]

PARAMS[("Business Parameters<br/>Financial Metrics")]

end

%% Core System Components

subgraph Core["Core Simulation Engine"]

SIM["Simulation<br/>Engine"]

MANU["Widget<br/>Manufacturer<br/>Model"]

CLAIM["Claim<br/>Generator"]

INS["Insurance<br/>Program"]

end

%% Analysis and Optimization

subgraph Analysis["Analysis & Optimization"]

ERGODIC["Ergodic<br/>Analyzer"]

OPT["Business<br/>Optimizer"]

MONTE["Monte Carlo<br/>Engine"]

SENS["Sensitivity<br/>Analyzer"]

end

%% Validation and Testing

subgraph Validation["Validation & Testing"]

ACC["Accuracy<br/>Validator"]

BACK["Strategy<br/>Backtester"]

WALK["Walk-Forward<br/>Validator"]

CONV["Convergence<br/>Monitor"]

end

%% Processing Infrastructure

subgraph Infrastructure["Processing Infrastructure"]

BATCH["Batch<br/>Processor"]

PARALLEL["Parallel<br/>Executor"]

CACHE["Smart<br/>Cache"]

STORAGE["Trajectory<br/>Storage"]

end

%% Reporting and Visualization

subgraph Output["Reporting & Visualization"]

VIZ["Visualization<br/>Engine"]

EXCEL["Excel<br/>Reporter"]

STATS["Summary<br/>Statistics"]

METRICS["Risk<br/>Metrics"]

end

%% Data Flow

CONFIG --> SIM

MARKET --> CLAIM

PARAMS --> MANU

SIM --> MANU

SIM --> CLAIM

SIM --> INS

MANU <--> INS

CLAIM --> INS

SIM --> MONTE

MONTE --> ERGODIC

MONTE --> OPT

ERGODIC --> SENS

OPT --> SENS

MONTE --> ACC

MONTE --> BACK

BACK --> WALK

MONTE --> CONV

CONV --> BATCH

BATCH --> PARALLEL

PARALLEL --> CACHE

CACHE --> STORAGE

ERGODIC --> VIZ

OPT --> VIZ

SENS --> VIZ

STORAGE --> STATS

STATS --> EXCEL

STATS --> METRICS

VIZ --> EXCEL

%% Styling

classDef external fill:#e1f5fe,stroke:#01579b,stroke-width:2px

classDef core fill:#fff3e0,stroke:#e65100,stroke-width:2px

classDef analysis fill:#f3e5f5,stroke:#4a148c,stroke-width:2px

classDef validation fill:#e8f5e9,stroke:#1b5e20,stroke-width:2px

classDef infra fill:#fce4ec,stroke:#880e4f,stroke-width:2px

classDef output fill:#e0f2f1,stroke:#004d40,stroke-width:2px

class CONFIG,MARKET,PARAMS external

class SIM,MANU,CLAIM,INS core

class ERGODIC,OPT,MONTE,SENS analysis

class ACC,BACK,WALK,CONV validation

class BATCH,PARALLEL,CACHE,STORAGE infra

class VIZ,EXCEL,STATS,METRICS output

System Overview

The Ergodic Insurance Limits framework is designed as a modular, high-performance system for analyzing insurance purchasing decisions through the lens of ergodic theory. The architecture follows these key principles:

1. Separation of Concerns

Core Simulation: Handles the fundamental business and insurance mechanics

Analysis Layer: Provides ergodic and optimization capabilities

Infrastructure: Manages computational efficiency and data handling

Validation: Ensures accuracy and robustness of results

Output: Delivers insights through visualizations and reports

2. Data Flow Architecture

Configuration and market data flow into the simulation engine

Simulations generate trajectories processed by analysis modules

Infrastructure layers provide caching and parallelization

Results flow to visualization and reporting components

3. Key Interactions

The Simulation Engine orchestrates the time evolution of the business model

The Manufacturer Model interacts with the Insurance Program for claim processing

Monte Carlo Engine generates multiple scenarios for statistical analysis

Ergodic Analyzer compares time-average vs ensemble-average growth

Batch Processor and Parallel Executor enable high-performance computing

4. External Dependencies

The system integrates with:

NumPy/SciPy for numerical computations

Pandas for data manipulation

Matplotlib/Plotly for visualizations

OpenPyXL for Excel reporting

Multiprocessing for parallel execution

Key highlights:

9 Major Subsystems: Configuration, Financial Core, Insurance, Simulation, Analytics, Optimization, Results, Validation, and External I/O

50+ Modules: Comprehensive coverage of all system components

Clear Data Flows: Shows how information moves between subsystems

External Integrations: YAML configs, CSV exports, Jupyter notebooks, and Sphinx documentation

Module Dependencies and Relationships

The module overview diagram provides a detailed view of how the 50+ Python modules interact with each other, showing import relationships and dependency hierarchies.

Module Overview and Dependencies

This diagram shows the detailed module structure and dependencies within the Ergodic Insurance framework.

graph LR

%% Configuration Layer

subgraph Config["Configuration Management"]

CONFIG_BASE["config.py<br/>Base Configuration"]

CONFIG_V2["config_v2.py<br/>Enhanced Config"]

CONFIG_MGR["config_manager.py<br/>Config Manager"]

CONFIG_LOADER["config_loader.py<br/>Config Loader"]

CONFIG_COMPAT["config_compat.py<br/>Compatibility Layer"]

CONFIG_MIG["config_migrator.py<br/>Migration Tools"]

end

%% Core Business Logic

subgraph Business["Business Logic"]

MANUFACTURER["manufacturer.py<br/>Widget Manufacturer"]

INSURANCE["insurance.py<br/>Insurance Policy"]

INS_PROGRAM["insurance_program.py<br/>Insurance Program"]

INS_PRICING["insurance_pricing.py<br/>Pricing Models"]

CLAIM_GEN["claim_generator.py<br/>Claim Events"]

CLAIM_DEV["claim_development.py<br/>Claim Development"]

EXPOSURE["exposure_base.py<br/>Exposure Models"]

end

%% Simulation Engine

subgraph Simulation["Simulation Core"]

SIM_CORE["simulation.py<br/>Main Engine"]

MONTE_CARLO["monte_carlo.py<br/>Monte Carlo"]

MONTE_WORKER["monte_carlo_worker.py<br/>MC Worker"]

STOCHASTIC["stochastic_processes.py<br/>Stochastic Models"]

LOSS_DIST["loss_distributions.py<br/>Loss Distributions"]

end

%% Analysis Tools

subgraph Analysis["Analysis & Optimization"]

ERGODIC_ANALYZER["ergodic_analyzer.py<br/>Ergodic Analysis"]

BUSINESS_OPT["business_optimizer.py<br/>Optimization"]

DECISION_ENGINE["decision_engine.py<br/>Decision Making"]

OPTIMIZATION["optimization.py<br/>Optimization Algos"]

HJB_SOLVER["hjb_solver.py<br/>HJB Equations"]

OPTIMAL_CTRL["optimal_control.py<br/>Control Theory"]

end

%% Validation & Testing

subgraph Validation["Validation"]

ACCURACY_VAL["accuracy_validator.py<br/>Accuracy Checks"]

STRATEGY_BACK["strategy_backtester.py<br/>Backtesting"]

WALK_FORWARD["walk_forward_validator.py<br/>Walk-Forward"]

VALIDATION_METRICS["validation_metrics.py<br/>Metrics"]

STATISTICAL_TESTS["statistical_tests.py<br/>Statistical Tests"]

end

%% Risk Analysis

subgraph Risk["Risk Analysis"]

RISK_METRICS["risk_metrics.py<br/>Risk Metrics"]

RUIN_PROB["ruin_probability.py<br/>Ruin Analysis"]

SENSITIVITY["sensitivity.py<br/>Sensitivity Analysis"]

SENS_VIZ["sensitivity_visualization.py<br/>Sensitivity Viz"]

PARETO["pareto_frontier.py<br/>Pareto Analysis"]

BOOTSTRAP["bootstrap_analysis.py<br/>Bootstrap Methods"]

end

%% Performance & Infrastructure

subgraph Infrastructure["Infrastructure"]

BATCH_PROC["batch_processor.py<br/>Batch Processing"]

PARALLEL_EXEC["parallel_executor.py<br/>Parallelization"]

PERF_OPT["performance_optimizer.py<br/>Performance"]

TRAJ_STORAGE["trajectory_storage.py<br/>Data Storage"]

PROGRESS_MON["progress_monitor.py<br/>Progress Tracking"]

PARAM_SWEEP["parameter_sweep.py<br/>Parameter Sweeps"]

end

%% Reporting & Visualization

subgraph Reporting["Reporting & Visualization"]

VIZ_LEGACY["visualization_legacy.py<br/>Legacy Plots"]

EXCEL_REPORT["excel_reporter.py<br/>Excel Reports"]

SUMMARY_STATS["summary_statistics.py<br/>Statistics"]

RESULT_AGG["result_aggregator.py<br/>Aggregation"]

FINANCIAL_STMT["financial_statements.py<br/>Statements"]

end

%% Visualization Submodule

subgraph VizModule["visualization/"]

VIZ_CORE["core.py<br/>Core Functions"]

VIZ_EXEC["executive_plots.py<br/>Executive Views"]

VIZ_TECH["technical_plots.py<br/>Technical Views"]

VIZ_ANNOT["annotations.py<br/>Annotations"]

VIZ_STYLE["style_manager.py<br/>Styling"]

VIZ_FACTORY["figure_factory.py<br/>Figure Factory"]

VIZ_EXPORT["export.py<br/>Export Tools"]

VIZ_BATCH["batch_plots.py<br/>Batch Plotting"]

VIZ_INTERACT["interactive_plots.py<br/>Interactive Plots"]

VIZ_TOWER["improved_tower_plot.py<br/>Tower Plots"]

end

%% Reporting Submodule

subgraph ReportModule["reporting/"]

REP_BUILDER["report_builder.py<br/>Report Builder"]

REP_EXEC["executive_report.py<br/>Executive Reports"]

REP_TECH["technical_report.py<br/>Technical Reports"]

REP_SCENARIO["scenario_comparator.py<br/>Scenario Compare"]

REP_TABLE["table_generator.py<br/>Table Generator"]

REP_INSIGHT["insight_extractor.py<br/>Insights"]

REP_FORMAT["formatters.py<br/>Formatters"]

REP_CACHE["cache_manager.py<br/>Cache Manager"]

REP_VALID["validator.py<br/>Report Validator"]

REP_CONFIG["config.py<br/>Report Config"]

end

%% Advanced Features

subgraph Advanced["Advanced Features"]

CONVERGENCE["convergence.py<br/>Convergence"]

CONV_ADV["convergence_advanced.py<br/>Advanced Conv."]

CONV_PLOTS["convergence_plots.py<br/>Conv. Plots"]

ADAPTIVE_STOP["adaptive_stopping.py<br/>Adaptive Stopping"]

SCENARIO_MGR["scenario_manager.py<br/>Scenarios"]

BENCHMARKING["benchmarking.py<br/>Benchmarks"]

end

%% Key Dependencies

CONFIG_BASE --> MANUFACTURER

CONFIG_V2 --> CONFIG_MGR

CONFIG_MGR --> CONFIG_LOADER

CONFIG_COMPAT --> CONFIG_MGR

MANUFACTURER --> SIM_CORE

INSURANCE --> INS_PROGRAM

INS_PRICING --> INS_PROGRAM

CLAIM_GEN --> SIM_CORE

CLAIM_DEV --> CLAIM_GEN

EXPOSURE --> MANUFACTURER

SIM_CORE --> MONTE_CARLO

MONTE_CARLO --> MONTE_WORKER

STOCHASTIC --> MONTE_CARLO

LOSS_DIST --> CLAIM_GEN

MONTE_CARLO --> ERGODIC_ANALYZER

ERGODIC_ANALYZER --> BUSINESS_OPT

BUSINESS_OPT --> DECISION_ENGINE

MONTE_CARLO --> ACCURACY_VAL

STRATEGY_BACK --> WALK_FORWARD

ERGODIC_ANALYZER --> RISK_METRICS

RISK_METRICS --> RUIN_PROB

SENSITIVITY --> PARETO

SENSITIVITY --> SENS_VIZ

BATCH_PROC --> PARALLEL_EXEC

PARALLEL_EXEC --> MONTE_CARLO

RESULT_AGG --> SUMMARY_STATS

SUMMARY_STATS --> EXCEL_REPORT

FINANCIAL_STMT --> EXCEL_REPORT

VIZ_CORE --> VIZ_FACTORY

VIZ_STYLE --> VIZ_EXEC

VIZ_STYLE --> VIZ_TECH

VIZ_FACTORY --> VIZ_EXPORT

VIZ_BATCH --> VIZ_CORE

VIZ_INTERACT --> VIZ_CORE

VIZ_TOWER --> VIZ_STYLE

REP_BUILDER --> REP_EXEC

REP_BUILDER --> REP_TECH

REP_SCENARIO --> REP_TABLE

REP_INSIGHT --> REP_EXEC

REP_FORMAT --> REP_TABLE

REP_CACHE --> REP_BUILDER

REP_VALID --> REP_BUILDER

%% Styling

classDef config fill:#e3f2fd,stroke:#1565c0,stroke-width:2px

classDef business fill:#fff9c4,stroke:#f57f17,stroke-width:2px

classDef simulation fill:#f3e5f5,stroke:#6a1b9a,stroke-width:2px

classDef analysis fill:#e8f5e9,stroke:#2e7d32,stroke-width:2px

classDef validation fill:#fce4ec,stroke:#c2185b,stroke-width:2px

classDef risk fill:#fff3e0,stroke:#ef6c00,stroke-width:2px

classDef infra fill:#e0f2f1,stroke:#00695c,stroke-width:2px

classDef reporting fill:#f1f8e9,stroke:#558b2f,stroke-width:2px

classDef viz fill:#e1f5fe,stroke:#0277bd,stroke-width:2px

classDef report fill:#fff8e1,stroke:#f9a825,stroke-width:2px

classDef advanced fill:#fafafa,stroke:#424242,stroke-width:2px

class CONFIG_BASE,CONFIG_V2,CONFIG_MGR,CONFIG_LOADER,CONFIG_COMPAT,CONFIG_MIG config

class MANUFACTURER,INSURANCE,INS_PROGRAM,INS_PRICING,CLAIM_GEN,CLAIM_DEV,EXPOSURE business

class SIM_CORE,MONTE_CARLO,MONTE_WORKER,STOCHASTIC,LOSS_DIST simulation

class ERGODIC_ANALYZER,BUSINESS_OPT,DECISION_ENGINE,OPTIMIZATION,HJB_SOLVER,OPTIMAL_CTRL analysis

class ACCURACY_VAL,STRATEGY_BACK,WALK_FORWARD,VALIDATION_METRICS,STATISTICAL_TESTS validation

class RISK_METRICS,RUIN_PROB,SENSITIVITY,SENS_VIZ,PARETO,BOOTSTRAP risk

class BATCH_PROC,PARALLEL_EXEC,PERF_OPT,TRAJ_STORAGE,PROGRESS_MON,PARAM_SWEEP infra

class VIZ_LEGACY,EXCEL_REPORT,SUMMARY_STATS,RESULT_AGG,FINANCIAL_STMT reporting

class VIZ_CORE,VIZ_EXEC,VIZ_TECH,VIZ_ANNOT,VIZ_STYLE,VIZ_FACTORY,VIZ_EXPORT,VIZ_BATCH,VIZ_INTERACT,VIZ_TOWER viz

class REP_BUILDER,REP_EXEC,REP_TECH,REP_SCENARIO,REP_TABLE,REP_INSIGHT,REP_FORMAT,REP_CACHE,REP_VALID,REP_CONFIG report

class CONVERGENCE,CONV_ADV,CONV_PLOTS,ADAPTIVE_STOP,SCENARIO_MGR,BENCHMARKING advanced

Module Categories

Configuration Management

Handles all configuration aspects including loading, validation, migration, and compatibility between different configuration versions.

Business Logic

Core business domain models including the manufacturer, insurance policies, pricing, and claim processing.

Simulation Core

The main simulation engine that orchestrates time evolution, Monte Carlo runs, and stochastic processes.

Analysis & Optimization

Advanced analytical tools including ergodic analysis, business optimization, and decision-making engines.

Validation

Comprehensive validation framework for ensuring accuracy and robustness of simulations.

Risk Analysis

Specialized risk assessment tools including ruin probability, sensitivity analysis, and bootstrap methods.

Infrastructure

High-performance computing infrastructure for parallel processing, caching, and data management.

Reporting & Visualization

Output generation including Excel reports, visualizations, and statistical summaries.

Advanced Features

Sophisticated features for convergence monitoring, adaptive stopping, and benchmarking.

Module organization:

Core Financial (4 modules): Central business logic and financial modeling

Insurance & Risk (5 modules): Insurance structures and risk management

Simulation (5 modules): Monte Carlo engine and parallel execution

Analytics (10 modules): Statistical analysis and metrics calculation

Optimization (6 modules): Strategy optimization and control theory

Results (7 modules): Reporting and visualization

Validation (7 modules): Testing and performance validation

Configuration (6 modules): Parameter management and settings

Class Diagrams

Detailed class structures are organized into three main categories:

Core Classes

The core classes diagram shows the fundamental building blocks of the system, including financial models, insurance structures, and simulation components.

Core Classes Diagram

This diagram shows the main classes and their relationships in the core simulation engine.

classDiagram

%% Core Simulation Classes

class Simulation {

-config: Config

-manufacturer: WidgetManufacturer

-claim_generator: ClaimGenerator

-insurance_program: InsuranceProgram

+run() SimulationResults

+step(year: int) dict

+process_claims(claims: List[ClaimEvent])

+check_solvency() bool

}

class SimulationResults {

+years: ndarray

+assets: ndarray

+equity: ndarray

+roe: ndarray

+revenue: ndarray

+net_income: ndarray

+claim_counts: ndarray

+claim_amounts: ndarray

+insolvency_year: Optional[int]

+to_dataframe() DataFrame

+calculate_time_weighted_roe() float

+calculate_rolling_roe(window: int) ndarray

}

class MonteCarloEngine {

-config: Config

-n_simulations: int

-parallel_executor: ParallelExecutor

-trajectory_storage: TrajectoryStorage

+run_simulations(n: int) List[SimulationResults]

+run_parallel(n_workers: int) List[SimulationResults]

+aggregate_results(results: List) dict

+calculate_convergence() ConvergenceMetrics

}

%% Business Model Classes

class WidgetManufacturer {

-config: ManufacturerConfig

-assets: float

-equity: float

-liabilities: float

-claim_liabilities: List[ClaimLiability]

+calculate_revenue() float

+calculate_operating_income() float

+process_insurance_claim(amount, deductible, limit) tuple

+step(working_capital_pct, growth_rate) dict

+apply_dividends(retention_ratio: float)

+update_balance_sheet()

+is_solvent() bool

}

class ClaimLiability {

+total_amount: float

+payment_schedule: List[float]

+years_remaining: int

+get_annual_payment() float

+advance_year()

}

%% Insurance Classes

class InsurancePolicy {

+deductible: float

+limit: float

+premium: float

+coverage_type: str

+calculate_payout(loss: float) float

+calculate_retained_loss(loss: float) float

}

class InsuranceProgram {

-policies: List[InsurancePolicy]

-total_premium: float

-letter_of_credit_rate: float

+add_policy(policy: InsurancePolicy)

+calculate_total_premium() float

+process_claim(amount: float) ClaimResult

+get_coverage_tower() List[dict]

+calculate_effective_retention() float

}

class ClaimResult {

+total_loss: float

+company_payment: float

+insurance_payment: float

+by_policy: List[PolicyPayout]

}

%% Claim Generation

class ClaimGenerator {

-frequency_dist: Distribution

-severity_dist: Distribution

-random_state: RandomState

+generate_claims(year: int) List[ClaimEvent]

+set_seed(seed: int)

+calibrate_to_historical(data: LossData)

}

class ClaimEvent {

+year: int

+amount: float

+cause: str

+severity_level: str

+timestamp: float

}

%% Configuration

class Config {

+simulation: SimulationConfig

+manufacturer: ManufacturerConfig

+insurance: InsuranceConfig

+monte_carlo: MonteCarloConfig

+validate()

+to_dict() dict

+from_dict(data: dict) Config

}

class ManufacturerConfig {

+initial_assets: float

+asset_turnover_ratio: float

+base_operating_margin: float

+tax_rate: float

+retention_ratio: float

+target_leverage: float

}

%% Relationships

Simulation --> WidgetManufacturer : uses

Simulation --> ClaimGenerator : uses

Simulation --> InsuranceProgram : uses

Simulation --> SimulationResults : produces

MonteCarloEngine --> Simulation : runs multiple

MonteCarloEngine --> SimulationResults : aggregates

WidgetManufacturer --> ClaimLiability : manages

WidgetManufacturer --> InsuranceProgram : interacts with

InsuranceProgram --> InsurancePolicy : contains

InsuranceProgram --> ClaimResult : produces

ClaimGenerator --> ClaimEvent : generates

Config --> ManufacturerConfig : contains

Simulation --> Config : configured by

Class Interactions

sequenceDiagram

participant MC as MonteCarloEngine

participant S as Simulation

participant M as Manufacturer

participant CG as ClaimGenerator

participant IP as InsuranceProgram

participant SR as SimulationResults

MC->>S: Initialize simulation

S->>M: Create manufacturer

S->>CG: Create claim generator

S->>IP: Setup insurance program

loop Each Year

S->>CG: Generate claims

CG-->>S: List[ClaimEvent]

loop Each Claim

S->>IP: Process claim

IP->>M: Calculate payout

M-->>IP: Company/insurance split

IP-->>S: ClaimResult

end

S->>M: Step forward (growth, operations)

M->>M: Update balance sheet

M-->>S: Financial metrics

S->>S: Check solvency

alt Insolvent

S-->>MC: Early termination

end

end

S->>SR: Compile results

SR-->>MC: SimulationResults

MC->>MC: Aggregate all paths

Key Design Patterns

1. Strategy Pattern

Insurance strategies can be swapped dynamically

Different optimization algorithms can be plugged in

2. Builder Pattern

Configuration objects use builder pattern for complex initialization

SimulationResults built incrementally during simulation

3. Observer Pattern

Progress monitoring observes simulation progress

Convergence monitors observe Monte Carlo iterations

4. Factory Pattern

ClaimGenerator acts as factory for ClaimEvents

FigureFactory creates visualization objects

5. Facade Pattern

MonteCarloEngine provides simplified interface to complex parallel execution

InsuranceProgram facades complex multi-policy interactions

Key components:

WidgetManufacturer: Central financial model with balance sheet evolution

StochasticProcess: Abstract base for various volatility models (GBM, OU, Lognormal)

InsuranceProgram: Multi-layer insurance structure implementation

ClaimGenerator: Loss event generation with configurable distributions

Data Models

The data models diagram illustrates configuration structures, result objects, and data transfer objects used throughout the system.

Data Models and Analysis Classes

This diagram shows the data structures and analysis models used throughout the system.

classDiagram

%% Ergodic Analysis Models

class ErgodicAnalyzer {

-convergence_threshold: float

-min_paths: int

-confidence_level: float

+analyze_trajectory(trajectory: ndarray) ErgodicData

+compare_scenarios(insured: List, uninsured: List) dict

+calculate_ergodic_metrics(data: ErgodicData) dict

+validate_insurance_impact() ValidationResults

+plot_ergodic_comparison()

}

class ErgodicData {

+trajectory: ndarray

+time_points: ndarray

+time_average: float

+ensemble_average: float

+growth_rate: float

+volatility: float

+survival_rate: float

+calculate_time_average() float

+calculate_ensemble_average() float

+calculate_ergodic_divergence() float

}

class ErgodicAnalysisResults {

+insured_metrics: dict

+uninsured_metrics: dict

+ergodic_advantage: dict

+confidence_intervals: dict

+convergence_metrics: ConvergenceMetrics

+to_dataframe() DataFrame

+plot_results()

}

%% Optimization Models

class BusinessOptimizer {

-objective: BusinessObjective

-constraints: BusinessConstraints

-algorithm: OptimizationAlgorithm

+optimize(initial_guess: dict) OptimalStrategy

+run_pareto_analysis() ParetoFrontier

+sensitivity_analysis() SensitivityResult

}

class OptimalStrategy {

+insurance_limit: float

+retention: float

+premium_budget: float

+expected_growth: float

+risk_metrics: dict

+implementation_steps: List[str]

}

class BusinessObjective {

+metric: str

+target_value: float

+weight: float

+evaluate(simulation_results: SimulationResults) float

}

class BusinessConstraints {

+min_equity: float

+max_leverage: float

+min_liquidity: float

+max_premium_ratio: float

+validate(state: dict) bool

}

%% Risk Metrics

class RiskMetrics {

+value_at_risk: float

+conditional_value_at_risk: float

+expected_shortfall: float

+maximum_drawdown: float

+sharpe_ratio: float

+sortino_ratio: float

+calculate_var(returns: ndarray, confidence: float) float

+calculate_cvar(returns: ndarray, confidence: float) float

+calculate_max_drawdown(equity: ndarray) float

}

class RuinProbability {

+threshold: float

+time_horizon: int

+probability: float

+expected_time_to_ruin: float

+calculate_ruin_prob(trajectories: List) float

+estimate_recovery_time() float

}

%% Convergence and Validation

class ConvergenceMetrics {

+mean_estimate: float

+std_estimate: float

+confidence_interval: tuple

+effective_sample_size: int

+gelman_rubin_stat: float

+is_converged: bool

+plot_convergence()

}

class ValidationResults {

+accuracy_metrics: dict

+statistical_tests: dict

+edge_cases: List[dict]

+performance_benchmarks: dict

+is_valid: bool

+generate_report() str

}

%% Sensitivity Analysis

class SensitivityAnalyzer {

-base_params: dict

-param_ranges: dict

-n_samples: int

+run_one_way_analysis(param: str) SensitivityResult

+run_two_way_analysis(param1: str, param2: str) TwoWaySensitivityResult

+run_sobol_analysis() SobolIndices

+plot_tornado_diagram()

}

class SensitivityResult {

+parameter: str

+values: ndarray

+outputs: ndarray

+elasticity: float

+critical_threshold: float

+plot()

}

%% Financial Statements

class FinancialStatements {

+balance_sheet: BalanceSheet

+income_statement: IncomeStatement

+cash_flow: CashFlowStatement

+ratios: FinancialRatios

+generate_statements(manufacturer: WidgetManufacturer)

+export_to_excel(path: str)

}

class BalanceSheet {

+assets: dict

+liabilities: dict

+equity: dict

+total_assets: float

+total_liabilities: float

+total_equity: float

+validate_balance() bool

}

class IncomeStatement {

+revenue: float

+operating_income: float

+insurance_expense: float

+tax_expense: float

+net_income: float

+ebitda: float

+calculate_margins() dict

}

%% Loss Distributions

class LossDistribution {

+distribution_type: str

+parameters: dict

+fitted: bool

+fit(data: ndarray)

+sample(n: int) ndarray

+pdf(x: float) float

+cdf(x: float) float

+quantile(p: float) float

}

class LossData {

+historical_losses: DataFrame

+frequency_data: ndarray

+severity_data: ndarray

+exposure_base: float

+clean_data()

+fit_distributions() dict

+validate_fit() bool

}

%% Relationships

ErgodicAnalyzer --> ErgodicData : creates

ErgodicAnalyzer --> ErgodicAnalysisResults : produces

ErgodicAnalyzer --> ValidationResults : validates with

BusinessOptimizer --> OptimalStrategy : finds

BusinessOptimizer --> BusinessObjective : uses

BusinessOptimizer --> BusinessConstraints : respects

OptimalStrategy --> RiskMetrics : includes

SensitivityAnalyzer --> SensitivityResult : produces

FinancialStatements --> BalanceSheet : contains

FinancialStatements --> IncomeStatement : contains

LossDistribution --> LossData : fitted from

ErgodicAnalysisResults --> ConvergenceMetrics : includes

ValidationResults --> RiskMetrics : uses

Data Flow Sequence

sequenceDiagram

participant Sim as Simulation

participant EA as ErgodicAnalyzer

participant BO as BusinessOptimizer

participant SA as SensitivityAnalyzer

participant RM as RiskMetrics

participant FS as FinancialStatements

Sim->>EA: Trajectory data

EA->>EA: Calculate time averages

EA->>EA: Calculate ensemble averages

EA->>RM: Request risk metrics

RM-->>EA: VaR, CVaR, Sharpe

EA-->>BO: Ergodic metrics

BO->>BO: Define objective

BO->>BO: Set constraints

BO->>SA: Request sensitivity

SA->>SA: Parameter sweep

SA-->>BO: Sensitivity results

BO-->>BO: Find optimal strategy

BO->>FS: Generate statements

FS->>FS: Build balance sheet

FS->>FS: Build income statement

FS-->>BO: Financial reports

Key Data Patterns

1. Immutable Data Objects

Results objects are immutable after creation

Ensures data integrity through analysis pipeline

2. Lazy Evaluation

Metrics calculated on-demand

Caching of expensive computations

3. Composite Pattern

FinancialStatements composed of multiple statement types

ErgodicAnalysisResults aggregates multiple metric types

4. Template Method

Base distribution class with template methods

Subclasses implement specific distributions

5. Data Transfer Objects (DTO)

Result classes act as DTOs between modules

Clean separation of data and logic

Key structures:

ConfigV2: Modern Pydantic-based configuration with validation

SimulationResults: Comprehensive result aggregation

ValidationMetrics: Performance and accuracy metrics

StateManagement: System state and progress tracking

Service Layer

The service layer diagram shows high-level services that orchestrate the core components, including analytics, optimization, and validation services.

Service Layer and Infrastructure

This diagram shows the service layer components that provide infrastructure support for the core simulation and analysis.

classDiagram

%% Batch Processing Services

class BatchProcessor {

-config: BatchConfig

-executor: ParallelExecutor

-cache: SmartCache

-progress_monitor: ProgressMonitor

+process_scenarios(scenarios: List) BatchResults

+process_parameter_sweep(params: dict) SweepResults

+process_convergence_study() ConvergenceResults

+resume_from_checkpoint(checkpoint_id: str)

}

class ParallelExecutor {

-n_workers: int

-chunk_size: int

-backend: str

-memory_limit: float

+map(func: Callable, items: List) List

+map_reduce(map_func, reduce_func, items) Any

+scatter_gather(tasks: List) List

+get_worker_status() dict

}

class SmartCache {

-cache_dir: Path

-max_size_gb: float

-ttl_hours: int

-compression: bool

+get(key: str) Optional[Any]

+set(key: str, value: Any)

+invalidate(pattern: str)

+get_stats() CacheStats

}

%% Progress and Monitoring

class ProgressMonitor {

-total_tasks: int

-completed_tasks: int

-start_time: float

-update_interval: float

+update(progress: float, message: str)

+estimate_time_remaining() float

+get_throughput() float

+display_progress_bar()

}

class ConvergenceMonitor {

-metrics: List[float]

-threshold: float

-window_size: int

-patience: int

+add_metric(value: float)

+check_convergence() bool

+get_convergence_rate() float

+plot_convergence_history()

}

%% Trajectory Storage

class TrajectoryStorage {

-storage_backend: str

-compression_level: int

-chunk_size: int

+store_trajectory(sim_id: str, data: ndarray)

+load_trajectory(sim_id: str) ndarray

+store_batch(trajectories: dict)

+query_trajectories(filter: dict) List

+get_storage_stats() dict

}

%% Parameter Management

class ParameterSweep {

-base_params: dict

-sweep_params: dict

-sweep_type: str

-n_points: int

+generate_grid() List[dict]

+generate_latin_hypercube() List[dict]

+generate_sobol_sequence() List[dict]

+adaptive_sampling(results: List) List[dict]

}

class ScenarioManager {

-scenarios: Dict[str, Scenario]

-active_scenario: str

+add_scenario(name: str, params: dict)

+load_scenario(name: str) Scenario

+compare_scenarios(names: List[str]) ComparisonResults

+export_scenarios(path: str)

}

%% Performance Optimization

class PerformanceOptimizer {

-profiler: cProfile

-memory_profiler: MemoryProfiler

-optimization_level: int

+profile_function(func: Callable) ProfileResult

+optimize_memory_usage()

+enable_numba_jit()

+vectorize_operations()

+get_bottlenecks() List[Bottleneck]

}

class VectorizedOperations {

<<static>>

+calculate_returns(prices: ndarray) ndarray

+calculate_drawdowns(equity: ndarray) ndarray

+calculate_rolling_stats(data: ndarray, window: int) dict

+apply_vectorized_claim(claims: ndarray, limits: ndarray) ndarray

}

%% Benchmarking

class BenchmarkSuite {

-benchmarks: List[Benchmark]

-baseline_results: dict

-comparison_results: dict

+add_benchmark(benchmark: Benchmark)

+run_all_benchmarks() BenchmarkResults

+compare_implementations(impl1, impl2) ComparisonReport

+generate_performance_report() str

}

class Benchmark {

+name: str

+setup_func: Callable

+test_func: Callable

+teardown_func: Callable

+n_iterations: int

+run() BenchmarkResult

}

%% Validation Services

class AccuracyValidator {

-tolerance: float

-reference_impl: ReferenceImplementations

+validate_calculation(func, inputs, expected) bool

+validate_convergence(results: List) bool

+validate_edge_cases() ValidationReport

+cross_validate(method1, method2) float

}

class StrategyBacktester {

-historical_data: DataFrame

-strategy: InsuranceStrategy

-metrics: List[str]

+backtest(start_date, end_date) BacktestResults

+walk_forward_analysis(window_size: int) WalkForwardResults

+calculate_performance_metrics() dict

+generate_backtest_report() str

}

%% Reporting Services

class ExcelReporter {

-template_path: str

-output_path: str

-workbook: Workbook

+create_summary_sheet(results: dict)

+create_charts(data: DataFrame)

+add_sensitivity_tables(sensitivity: SensitivityResult)

+add_risk_metrics(metrics: RiskMetrics)

+format_report()

+save()

}

class ResultAggregator {

-results: List[SimulationResults]

-aggregation_funcs: dict

+add_results(results: SimulationResults)

+calculate_statistics() SummaryStatistics

+calculate_percentiles(percentiles: List) dict

+group_by(key: str) Dict[str, List]

+export_aggregated_data(format: str)

}

%% Visualization Services

class FigureFactory {

-style_manager: StyleManager

-default_size: tuple

-dpi: int

+create_line_plot(data: DataFrame) Figure

+create_distribution_plot(data: ndarray) Figure

+create_heatmap(data: ndarray) Figure

+create_dashboard(results: dict) Figure

+save_figure(fig: Figure, path: str)

}

class StyleManager {

-theme: Theme

-color_palette: List[str]

-font_settings: dict

+apply_theme(theme: Theme)

+get_color_cycle() List

+format_axis(ax: Axes)

+add_annotations(ax: Axes, annotations: List)

}

%% Relationships

BatchProcessor --> ParallelExecutor : uses

BatchProcessor --> SmartCache : caches with

BatchProcessor --> ProgressMonitor : monitors with

ParallelExecutor --> VectorizedOperations : optimizes with

ParameterSweep --> ScenarioManager : generates for

PerformanceOptimizer --> VectorizedOperations : creates

PerformanceOptimizer --> BenchmarkSuite : benchmarks with

BenchmarkSuite --> Benchmark : runs

AccuracyValidator --> StrategyBacktester : validates

ResultAggregator --> ExcelReporter : feeds

ResultAggregator --> FigureFactory : visualizes with

FigureFactory --> StyleManager : styled by

BatchProcessor --> TrajectoryStorage : stores in

ConvergenceMonitor --> ProgressMonitor : reports to

Service Interaction Flow

sequenceDiagram

participant Client

participant BP as BatchProcessor

participant PE as ParallelExecutor

participant SC as SmartCache

participant TS as TrajectoryStorage

participant PM as ProgressMonitor

participant RA as ResultAggregator

participant ER as ExcelReporter

Client->>BP: Submit batch job

BP->>SC: Check cache

alt Cache hit

SC-->>BP: Cached results

BP-->>Client: Return results

else Cache miss

BP->>PM: Initialize monitor

BP->>PE: Distribute work

loop Parallel execution

PE->>PE: Process chunk

PE->>PM: Update progress

PM-->>Client: Progress update

end

PE-->>BP: Raw results

BP->>TS: Store trajectories

BP->>SC: Cache results

BP->>RA: Aggregate results

RA->>ER: Generate report

ER-->>Client: Excel report

BP-->>Client: Complete results

end

Service Layer Patterns

1. Service Locator Pattern

Central registry for service discovery

Dynamic service binding at runtime

2. Repository Pattern

TrajectoryStorage abstracts data persistence

ScenarioManager provides scenario repository

3. Unit of Work Pattern

BatchProcessor coordinates complex operations

Ensures consistency across service calls

4. Pipeline Pattern

Data flows through processing pipeline

Each service transforms data for next stage

5. Decorator Pattern

ProgressMonitor decorates long-running operations

SmartCache decorates expensive computations

6. Adapter Pattern

ExcelReporter adapts results to Excel format

Different storage backends adapted by TrajectoryStorage

Service categories:

Analytics Services: ErgodicAnalyzer, RiskMetrics, ConvergenceDiagnostics

Optimization Services: BusinessOptimizer, HJBSolver, ParetoFrontier

Simulation Services: MonteCarloEngine, ParallelExecutor, BatchProcessor

Validation Services: WalkForwardValidator, StrategyBacktester, BenchmarkSuite

Design Patterns

The architecture employs several well-established design patterns:

Pattern |

Implementation |

|---|---|

Factory Pattern |

ConfigManager creates appropriate configuration objects |

Strategy Pattern |

StochasticProcess implementations (GBM, OU, Lognormal) |

Observer Pattern |

ProgressMonitor with callbacks for real-time updates |

Template Method |

LossDistribution abstract base class |

Adapter Pattern |

ConfigCompat bridges v1 and v2 configurations |

Singleton Pattern |

ConfigManager ensures single configuration instance |

Command Pattern |

BatchProcessor queues and executes simulation tasks |

Composite Pattern |

InsuranceProgram composes multiple InsuranceLayers |

Repository Pattern |

TrajectoryStorage abstracts data persistence |

Chain of Responsibility |

ResultAggregator chains for hierarchical processing |

Performance Architecture

The system is designed for high-performance computation:

Operation |

Target |

Status |

|---|---|---|

1000-year simulation |

< 1 minute |

✅ Achieved |

100K Monte Carlo iterations |

< 10 minutes |

✅ Achieved |

1M iterations |

Overnight |

✅ Achieved |

Memory per trajectory |

< 1MB |

✅ Optimized |

Parallel efficiency |

> 80% |

✅ Verified |

Key Architectural Decisions

Modular Design: Each module has a single, well-defined responsibility

Configuration-Driven: All parameters externalized through Pydantic models

Parallel Processing: CPU-optimized execution for large-scale simulations

Ergodic Theory Integration: Core differentiation through time vs ensemble analysis

Extensible Plugin Architecture: New components without modifying core

85+% Test Coverage: Comprehensive testing across all modules