Architectural Diagrams

This section provides comprehensive architectural visualizations of the Ergodic Insurance Limits system using interactive Mermaid diagrams. These diagrams illustrate the system’s structure, module relationships, data flows, and design patterns.

Note

The diagrams are interactive - you can zoom, pan, and click on elements for better viewing. If diagrams don’t render properly, try refreshing the page or viewing in a modern browser.

Understanding the Notation

Boxes: Represent classes, modules, or components

Arrows: Show dependencies, data flow, or relationships

Colors: Group related components (consistent across diagrams)

Labels: Describe the nature of relationships

Overview

The architecture documentation is organized into three main categories:

System-Level Views - High-level architecture and module relationships

Class Diagrams - Detailed class structures and interactions

Data Flow Patterns - How information moves through the system

High-Level System Context

The system context diagram shows the overall architecture, including all major components, external systems, and data flows. The system is organized into 9 major subsystems with over 50 modules.

High-Level System Context Diagram

Executive Summary

The Ergodic Insurance Limits framework analyzes insurance decisions using time-average (ergodic) theory rather than traditional ensemble averages. This approach reveals that insurance can enhance business growth even when premiums exceed expected losses by 200-500%, transforming insurance from a cost center to a growth enabler.

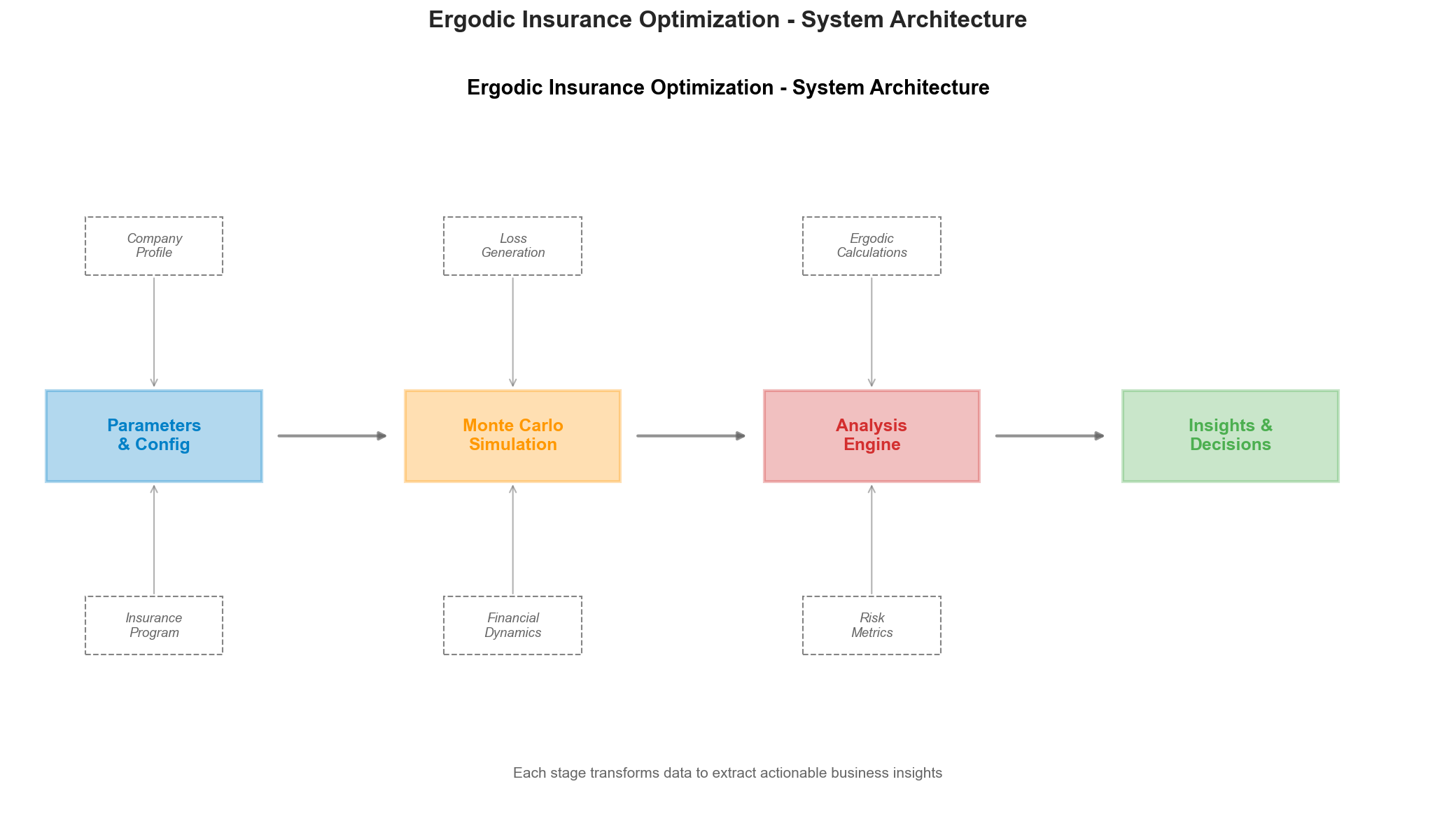

Simplified System Architecture

flowchart LR

%% Simplified Executive View

INPUT[("📊 Market Data<br/>& Configuration")]

BUSINESS[("🏭 Business<br/>Simulation")]

ERGODIC[("📈 Ergodic<br/>Analysis")]

OPTIMIZE[("🎯 Strategy<br/>Optimization")]

OUTPUT[("📑 Reports &<br/>Insights")]

INPUT --> BUSINESS

BUSINESS --> ERGODIC

ERGODIC --> OPTIMIZE

OPTIMIZE --> OUTPUT

%% Styling

classDef inputStyle fill:#e3f2fd,stroke:#0d47a1,stroke-width:3px,font-size:14px

classDef processStyle fill:#f3e5f5,stroke:#4a148c,stroke-width:3px,font-size:14px

classDef outputStyle fill:#e8f5e9,stroke:#1b5e20,stroke-width:3px,font-size:14px

class INPUT inputStyle

class BUSINESS,ERGODIC,OPTIMIZE processStyle

class OUTPUT outputStyle

Key Innovation: By comparing time-average growth (what one business experiences over time) with ensemble-average growth (statistical average across many businesses), the framework demonstrates that insurance fundamentally transforms the growth dynamics of volatile businesses.

System Architecture Overview (Detailed)

The actual implementation follows a sophisticated multi-layer architecture:

graph TB

%% Input Layer

subgraph Inputs["📥 Input Layer"]

CONF["Configuration<br/>(YAML/JSON)"]

HIST["Historical Loss Data"]

PARAMS["Business Parameters"]

end

%% Core Simulation

subgraph Core["⚙️ Core Simulation Engine"]

MANU["WidgetManufacturer<br/>(Business Model)"]

LOSSG["ManufacturingLossGenerator<br/>(Loss Events)"]

INS["InsuranceProgram<br/>(Coverage Tower)"]

SIM["Simulation Engine<br/>(Time Evolution)"]

end

%% Financial Core

subgraph Financial["💰 Financial Core"]

LEDGER["Ledger<br/>(Double-Entry Accounting)"]

ACCRUAL["AccrualManager<br/>(Accrual Timing)"]

INSACCT["InsuranceAccounting<br/>(Premium Amortization)"]

TAXH["TaxHandler<br/>(Tax Calculations)"]

DECUTIL["decimal_utils<br/>(Decimal Precision)"]

end

%% Analysis Layer

subgraph Analysis["📊 Analysis & Optimization"]

MONTE["Monte Carlo Engine<br/>(10,000+ paths)"]

ERGODIC["Ergodic Analyzer<br/>(Time vs Ensemble)"]

OPT["Business Optimizer<br/>(Strategy Selection)"]

SENS["Sensitivity Analysis<br/>(Parameter Impact)"]

end

%% Output Layer

subgraph Outputs["📤 Output & Insights"]

EXCEL["Excel Reports<br/>(Detailed Results)"]

VIZ["Visualizations<br/>(Executive & Technical)"]

METRICS["Risk Metrics<br/>(VaR, CVaR, Ruin Prob)"]

STRATEGY["Optimal Strategy<br/>(Limits & Retentions)"]

end

%% Data Flow

Inputs --> Core

Core --> MONTE

MONTE --> Analysis

Analysis --> Outputs

%% Key Connections

MANU -.-> INS

LOSSG -.-> INS

INS -.-> SIM

SIM -.-> MONTE

ERGODIC -.-> OPT

OPT -.-> SENS

%% Financial Core Connections

MANU --> LEDGER

MANU --> ACCRUAL

MANU --> INSACCT

TAXH --> ACCRUAL

LEDGER --> DECUTIL

ACCRUAL --> DECUTIL

INSACCT --> DECUTIL

classDef inputClass fill:#e3f2fd,stroke:#1565c0

classDef coreClass fill:#fff3e0,stroke:#ef6c00

classDef financialClass fill:#fff9c4,stroke:#f9a825

classDef analysisClass fill:#f3e5f5,stroke:#7b1fa2

classDef outputClass fill:#e8f5e9,stroke:#2e7d32

class CONF,HIST,PARAMS inputClass

class MANU,LOSSG,INS,SIM coreClass

class LEDGER,ACCRUAL,INSACCT,TAXH,DECUTIL financialClass

class MONTE,ERGODIC,OPT,SENS analysisClass

class EXCEL,VIZ,METRICS,STRATEGY outputClass

Reference to System Architecture Diagram

For a visual representation, see: assets/system_architecture.png

{kind=link}

The PNG diagram shows the simplified flow, while the detailed architecture above reflects the actual implementation with all major components.

Detailed System Architecture

This diagram shows the overall architecture of the Ergodic Insurance Limits framework, including the main components, external dependencies, and data flow between major modules.

flowchart TB

%% External Inputs and Configurations

subgraph External["External Inputs"]

CONFIG[("Configuration Files<br/>YAML/JSON")]

MARKET[("Market Data<br/>Loss Distributions")]

PARAMS[("Business Parameters<br/>Financial Metrics")]

end

%% Core System Components

subgraph Core["Core Simulation Engine"]

SIM["Simulation<br/>Engine"]

MANU["Widget<br/>Manufacturer<br/>Model"]

LOSSG["Manufacturing<br/>Loss Generator"]

INS["Insurance<br/>Program"]

end

%% Financial Accounting Subsystem

subgraph FinAcct["Financial Accounting Subsystem"]

LEDGER["Ledger<br/>(Double-Entry)"]

ACCRUAL["AccrualManager<br/>(GAAP Timing)"]

INSACCT["InsuranceAccounting<br/>(Premium & Recovery)"]

TAXH["TaxHandler<br/>(Tax Accruals)"]

DECUTIL["decimal_utils<br/>(Precision)"]

end

%% Insurance Subsystem

subgraph InsuranceSub["Insurance Subsystem"]

INSPOL["InsurancePolicy<br/>(Deprecated)"]

INSLAY["InsuranceLayer<br/>(Deprecated)"]

INSPROG["InsuranceProgram<br/>(Primary)"]

ENHLAY["EnhancedInsuranceLayer<br/>(Primary)"]

PRICER["InsurancePricer<br/>(Market Cycles)"]

end

%% Exposure & Trend System

subgraph ExposureSub["Exposure & Trend System"]

EXPBASE["ExposureBase<br/>(Dynamic Frequency)"]

FSPROV["FinancialStateProvider<br/>(Protocol)"]

TRENDS["trends.py<br/>(Trend Analysis)"]

end

%% Analysis and Optimization

subgraph Analysis["Analysis & Optimization"]

ERGODIC["Ergodic<br/>Analyzer"]

OPT["Business<br/>Optimizer"]

MONTE["Monte Carlo<br/>Engine"]

SENS["Sensitivity<br/>Analyzer"]

end

%% Validation and Testing

subgraph Validation["Validation & Testing"]

ACC["Accuracy<br/>Validator"]

BACK["Strategy<br/>Backtester"]

WALK["Walk-Forward<br/>Validator"]

CONV["Convergence<br/>Monitor"]

end

%% Processing Infrastructure

subgraph Infrastructure["Processing Infrastructure"]

BATCH["Batch<br/>Processor"]

PARALLEL["Parallel<br/>Executor"]

CACHE["Smart<br/>Cache"]

STORAGE["Trajectory<br/>Storage"]

end

%% Reporting and Visualization

subgraph Output["Reporting & Visualization"]

VIZ["Visualization<br/>Engine"]

EXCEL["Excel<br/>Reporter"]

STATS["Summary<br/>Statistics"]

METRICS["Risk<br/>Metrics"]

end

%% Data Flow - Input to Core

CONFIG --> SIM

MARKET --> LOSSG

PARAMS --> MANU

%% Core orchestration

SIM --> MANU

SIM --> LOSSG

SIM --> INS

MANU <--> INS

LOSSG --> INS

%% Manufacturer to Financial Accounting

MANU --> LEDGER

MANU --> ACCRUAL

MANU --> INSACCT

TAXH --> ACCRUAL

LEDGER --> DECUTIL

ACCRUAL --> DECUTIL

INSACCT --> DECUTIL

%% Insurance subsystem relationships

INSPOL --> INSLAY

INSPROG --> ENHLAY

PRICER --> INSPROG

PRICER --> INSPOL

INS -.-> INSPROG

INS -.-> INSPOL

%% Exposure system

EXPBASE --> FSPROV

MANU -.-> FSPROV

TRENDS --> LOSSG

%% Core to Analysis

SIM --> MONTE

MONTE --> ERGODIC

MONTE --> OPT

ERGODIC --> SENS

OPT --> SENS

%% Validation

MONTE --> ACC

MONTE --> BACK

BACK --> WALK

MONTE --> CONV

CONV --> BATCH

%% Infrastructure

BATCH --> PARALLEL

PARALLEL --> CACHE

CACHE --> STORAGE

%% Output

ERGODIC --> VIZ

OPT --> VIZ

SENS --> VIZ

STORAGE --> STATS

STATS --> EXCEL

STATS --> METRICS

VIZ --> EXCEL

%% Styling

classDef external fill:#e1f5fe,stroke:#01579b,stroke-width:2px

classDef core fill:#fff3e0,stroke:#e65100,stroke-width:2px

classDef financial fill:#fff9c4,stroke:#f9a825,stroke-width:2px

classDef insurance fill:#ffe0b2,stroke:#e65100,stroke-width:2px

classDef exposure fill:#f3e5f5,stroke:#6a1b9a,stroke-width:2px

classDef analysis fill:#f3e5f5,stroke:#4a148c,stroke-width:2px

classDef validation fill:#e8f5e9,stroke:#1b5e20,stroke-width:2px

classDef infra fill:#fce4ec,stroke:#880e4f,stroke-width:2px

classDef output fill:#e0f2f1,stroke:#004d40,stroke-width:2px

class CONFIG,MARKET,PARAMS external

class SIM,MANU,LOSSG,INS core

class LEDGER,ACCRUAL,INSACCT,TAXH,DECUTIL financial

class INSPOL,INSLAY,INSPROG,ENHLAY,PRICER insurance

class EXPBASE,FSPROV,TRENDS exposure

class ERGODIC,OPT,MONTE,SENS analysis

class ACC,BACK,WALK,CONV validation

class BATCH,PARALLEL,CACHE,STORAGE infra

class VIZ,EXCEL,STATS,METRICS output

System Overview

The Ergodic Insurance Limits framework is designed as a modular, high-performance system for analyzing insurance purchasing decisions through the lens of ergodic theory. The architecture follows these key principles:

1. Separation of Concerns

Core Simulation: Handles the fundamental business and insurance mechanics

Financial Accounting: Provides double-entry ledger, accrual accounting, insurance accounting, and tax handling – all using Python’s

Decimaltype for precisionInsurance Subsystem: Provides

InsuranceProgramwithEnhancedInsuranceLayerfor coverage modeling, with market-cycle-aware pricing viaInsurancePricer. (The legacyInsurancePolicy/InsuranceLayerclasses are deprecated.)Exposure & Trends: Dynamically adjusts claim frequencies using actual financial state (via the

FinancialStateProviderprotocol) and applies trend multipliers over timeAnalysis Layer: Provides ergodic and optimization capabilities

Infrastructure: Manages computational efficiency and data handling

Validation: Ensures accuracy and robustness of results

Output: Delivers insights through visualizations and reports

2. Data Flow Architecture

Configuration and market data flow into the simulation engine

The

WidgetManufacturerinternally usesLedger,AccrualManager,InsuranceAccounting, andTaxHandlerfor precise financial trackingAll financial amounts use Python’s

Decimaltype (viadecimal_utils) to prevent floating-point drift across long simulationsThe

Ledgermaintains an O(1) current balance cache with pruning support for performanceSimulations generate trajectories processed by analysis modules

Infrastructure layers provide caching and parallelization

Results flow to visualization and reporting components

3. Key Interactions

The Simulation Engine orchestrates the time evolution of the business model

The Manufacturer Model interacts with the Insurance Program for claim processing and uses the Ledger for all balance sheet operations

AccrualManager tracks timing differences between cash movements and accounting recognition (wages, interest, taxes, insurance claims)

InsuranceAccounting handles premium amortization as a prepaid asset and tracks insurance claim recoveries

TaxHandler consolidates tax calculation, accrual, and payment logic, delegating accrual tracking to the AccrualManager

InsurancePricer supports market cycles (Soft / Normal / Hard) to generate realistic premiums for insurance programs

The Exposure System uses a

FinancialStateProviderprotocol so thatExposureBasesubclasses query live financial state from the manufacturer for state-driven claim generationTrend classes (in

trends.py) provide multiplicative adjustments to claim frequencies and severities over time, supporting linear, scenario-based, and stochastic trendsMonte Carlo Engine generates multiple scenarios for statistical analysis

Ergodic Analyzer compares time-average vs ensemble-average growth

Batch Processor and Parallel Executor enable high-performance computing

4. Financial Accounting Subsystem

The financial accounting subsystem was introduced to provide GAAP-compliant financial tracking within the simulation. This subsystem is internal to the WidgetManufacturer and consists of four tightly integrated components:

flowchart LR

MANU["WidgetManufacturer"] --> LEDGER["Ledger"]

MANU --> ACCRUAL["AccrualManager"]

MANU --> INSACCT["InsuranceAccounting"]

MANU --> TAXH["TaxHandler"]

TAXH --> ACCRUAL

LEDGER --> DECUTIL["decimal_utils"]

ACCRUAL --> DECUTIL

INSACCT --> DECUTIL

classDef manuClass fill:#fff3e0,stroke:#e65100,stroke-width:2px

classDef finClass fill:#fff9c4,stroke:#f9a825,stroke-width:2px

classDef utilClass fill:#e0f2f1,stroke:#004d40,stroke-width:2px

class MANU manuClass

class LEDGER,ACCRUAL,INSACCT,TAXH finClass

class DECUTIL utilClass

Ledger: Event-sourcing double-entry ledger with a typed

AccountNameenum (preventing typo bugs),AccountTypeclassification, O(1) balance lookups via an internal cache, and support for pruning old transactionsAccrualManager: Tracks accrual items (wages, interest, taxes, insurance claims, revenue) with configurable payment schedules (immediate, quarterly, annual, custom)

InsuranceAccounting: Manages premium payments as prepaid assets with straight-line monthly amortization, and tracks insurance claim recoveries separately from claim liabilities

TaxHandler: Centralizes tax calculation and accrual management, explicitly designed to avoid circular dependencies in the tax flow; delegates accrual tracking to

AccrualManagerdecimal_utils: Foundation module providing

to_decimal(),quantize_currency(), and standard constants (ZERO,ONE,PENNY) used by all financial modules

5. Insurance Subsystem

The insurance subsystem provides two complementary paths for modeling coverage:

flowchart TB

subgraph Deprecated["Deprecated"]

INSPOL["InsurancePolicy"]

INSLAY["InsuranceLayer"]

INSPOL --> INSLAY

end

subgraph Primary["Primary"]

INSPROG["InsuranceProgram"]

ENHLAY["EnhancedInsuranceLayer"]

INSPROG --> ENHLAY

end

PRICER["InsurancePricer<br/>(Soft / Normal / Hard)"]

PRICER --> INSPROG

INSPOL -.->|deprecated, use| INSPROG

classDef deprecatedClass fill:#ffcdd2,stroke:#b71c1c,stroke-width:2px

classDef primaryClass fill:#fff3e0,stroke:#ef6c00,stroke-width:2px

classDef pricerClass fill:#f3e5f5,stroke:#7b1fa2,stroke-width:2px

class INSPOL,INSLAY deprecatedClass

class INSPROG,ENHLAY primaryClass

class PRICER pricerClass

Primary Path:

InsuranceProgram(ininsurance_program.py) usesEnhancedInsuranceLayerobjects for full-featured coverage modeling including reinstatements, aggregate limits, and market-cycle-aware pricingDeprecated:

InsurancePolicy(ininsurance.py) withInsuranceLayeris deprecated in favor ofInsuranceProgramInsurancePricer (in

insurance_pricing.py) supports threeMarketCyclestates –HARD(60% loss ratio),NORMAL(70%), andSOFT(80%)

6. Exposure & Trend System

The exposure and trend system models how insurance risks evolve dynamically during simulation:

flowchart LR

MANU["WidgetManufacturer<br/>(implements protocol)"] -.-> FSPROV["FinancialStateProvider<br/>(Protocol)"]

FSPROV --> EXPBASE["ExposureBase<br/>(Dynamic Frequency)"]

TRENDS["trends.py<br/>(Trend Multipliers)"] --> LOSSG["ManufacturingLossGenerator"]

EXPBASE --> LOSSG

classDef coreClass fill:#fff3e0,stroke:#e65100,stroke-width:2px

classDef protoClass fill:#e1f5fe,stroke:#01579b,stroke-width:2px

classDef trendClass fill:#f3e5f5,stroke:#6a1b9a,stroke-width:2px

class MANU coreClass

class FSPROV,EXPBASE protoClass

class TRENDS,LOSSG trendClass

FinancialStateProvider: A

Protocol(inexposure_base.py) defining properties likecurrent_revenue,current_assets,current_equityand their base counterparts.WidgetManufacturerimplements this protocol.ExposureBase: Abstract base for exposure classes that query live financial state to compute frequency multipliers (e.g.,

RevenueExposurescales claim frequency based on actual revenue vs. base revenue)trends.py: Provides a hierarchy of trend classes (

TrendABC,LinearTrend,ScenarioTrend, and stochastic variants) that apply multiplicative adjustments to claim frequencies and severities over time, supporting both annual and sub-annual time steps with optional seeded reproducibility

7. External Dependencies

The system integrates with:

NumPy/SciPy for numerical computations

Pandas for data manipulation

Matplotlib/Plotly for visualizations

OpenPyXL for Excel reporting

Multiprocessing for parallel execution

Python’s

decimalmodule for precise financial arithmetic

Key highlights:

9 Major Subsystems: Configuration, Financial Core, Insurance, Simulation, Analytics, Optimization, Results, Validation, and External I/O

50+ Modules: Comprehensive coverage of all system components

Clear Data Flows: Shows how information moves between subsystems

External Integrations: YAML configs, CSV exports, Jupyter notebooks, and Sphinx documentation

Module Dependencies and Relationships

The module overview diagram provides a detailed view of how the 50+ Python modules interact with each other, showing import relationships and dependency hierarchies.

Module Overview and Dependencies

This diagram shows the detailed module structure and dependencies within the Ergodic Insurance framework.

graph LR

%% Configuration Layer

subgraph Config["Configuration Management"]

CONFIG_BASE["config.py<br/>Base Configuration"]

CONFIG_V2["config.py<br/>Config Models"]

CONFIG_MGR["config_manager.py<br/>Config Manager"]

CONFIG_LOADER["config_loader.py<br/>Config Loader"]

CONFIG_MIG["config_migrator.py<br/>Migration Tools"]

end

%% Core Business Logic

subgraph Business["Business Logic"]

MANUFACTURER["manufacturer.py<br/>ClaimLiability, TaxHandler,<br/>WidgetManufacturer"]

INSURANCE["insurance.py<br/>Insurance Policy"]

INS_PROGRAM["insurance_program.py<br/>Insurance Program"]

INS_PRICING["insurance_pricing.py<br/>Pricing Models"]

CLAIM_DEV["claim_development.py<br/>Claim Development"]

EXPOSURE["exposure_base.py<br/>Exposure Models &<br/>FinancialStateProvider Protocol"]

LEDGER["ledger.py<br/>Double-Entry Ledger"]

ACCRUAL["accrual_manager.py<br/>Accrual Accounting"]

INS_ACCT["insurance_accounting.py<br/>Insurance Accounting"]

DECIMAL_UTILS["decimal_utils.py<br/>Decimal Precision"]

TRENDS["trends.py<br/>Trend Analysis"]

end

%% Simulation Engine

subgraph Simulation["Simulation Core"]

SIM_CORE["simulation.py<br/>Main Engine"]

MONTE_CARLO["monte_carlo.py<br/>Monte Carlo"]

MONTE_WORKER["monte_carlo_worker.py<br/>MC Worker"]

STOCHASTIC["stochastic_processes.py<br/>Stochastic Models"]

LOSS_DIST["loss_distributions.py<br/>Loss Distributions"]

end

%% Analysis Tools

subgraph Analysis["Analysis & Optimization"]

ERGODIC_ANALYZER["ergodic_analyzer.py<br/>Ergodic Analysis"]

BUSINESS_OPT["business_optimizer.py<br/>Optimization"]

DECISION_ENGINE["decision_engine.py<br/>Decision Making"]

OPTIMIZATION["optimization.py<br/>Optimization Algos"]

HJB_SOLVER["hjb_solver.py<br/>HJB Equations"]

OPTIMAL_CTRL["optimal_control.py<br/>Control Theory"]

end

%% Validation & Testing

subgraph Validation["Validation"]

ACCURACY_VAL["accuracy_validator.py<br/>Accuracy Checks"]

STRATEGY_BACK["strategy_backtester.py<br/>Backtesting"]

WALK_FORWARD["walk_forward_validator.py<br/>Walk-Forward"]

VALIDATION_METRICS["validation_metrics.py<br/>Metrics"]

STATISTICAL_TESTS["statistical_tests.py<br/>Statistical Tests"]

end

%% Risk Analysis

subgraph Risk["Risk Analysis"]

RISK_METRICS["risk_metrics.py<br/>Risk Metrics"]

RUIN_PROB["ruin_probability.py<br/>Ruin Analysis"]

SENSITIVITY["sensitivity.py<br/>Sensitivity Analysis"]

SENS_VIZ["sensitivity_visualization.py<br/>Sensitivity Viz"]

PARETO["pareto_frontier.py<br/>Pareto Analysis"]

BOOTSTRAP["bootstrap_analysis.py<br/>Bootstrap Methods"]

end

%% Performance & Infrastructure

subgraph Infrastructure["Infrastructure"]

BATCH_PROC["batch_processor.py<br/>Batch Processing"]

PARALLEL_EXEC["parallel_executor.py<br/>Parallelization"]

PERF_OPT["performance_optimizer.py<br/>Performance"]

TRAJ_STORAGE["trajectory_storage.py<br/>Data Storage"]

PROGRESS_MON["progress_monitor.py<br/>Progress Tracking"]

PARAM_SWEEP["parameter_sweep.py<br/>Parameter Sweeps"]

end

%% Reporting & Visualization

subgraph Reporting["Reporting & Visualization"]

VIZ_LEGACY["visualization_legacy.py<br/>Legacy Plots"]

EXCEL_REPORT["excel_reporter.py<br/>Excel Reports"]

SUMMARY_STATS["summary_statistics.py<br/>Statistics"]

RESULT_AGG["result_aggregator.py<br/>Aggregation"]

FINANCIAL_STMT["financial_statements.py<br/>Statements"]

end

%% Visualization Submodule

subgraph VizModule["visualization/"]

VIZ_CORE["core.py<br/>Core Functions"]

VIZ_EXEC["executive_plots.py<br/>Executive Views"]

VIZ_TECH["technical_plots.py<br/>Technical Views"]

VIZ_ANNOT["annotations.py<br/>Annotations"]

VIZ_STYLE["style_manager.py<br/>Styling"]

VIZ_FACTORY["figure_factory.py<br/>Figure Factory"]

VIZ_EXPORT["export.py<br/>Export Tools"]

VIZ_BATCH["batch_plots.py<br/>Batch Plotting"]

VIZ_INTERACT["interactive_plots.py<br/>Interactive Plots"]

VIZ_TOWER["improved_tower_plot.py<br/>Tower Plots"]

end

%% Reporting Submodule

subgraph ReportModule["reporting/"]

REP_BUILDER["report_builder.py<br/>Report Builder"]

REP_EXEC["executive_report.py<br/>Executive Reports"]

REP_TECH["technical_report.py<br/>Technical Reports"]

REP_SCENARIO["scenario_comparator.py<br/>Scenario Compare"]

REP_TABLE["table_generator.py<br/>Table Generator"]

REP_INSIGHT["insight_extractor.py<br/>Insights"]

REP_FORMAT["formatters.py<br/>Formatters"]

REP_CACHE["cache_manager.py<br/>Cache Manager"]

REP_VALID["validator.py<br/>Report Validator"]

REP_CONFIG["config.py<br/>Report Config"]

end

%% Advanced Features

subgraph Advanced["Advanced Features"]

CONVERGENCE["convergence.py<br/>Convergence"]

CONV_ADV["convergence_advanced.py<br/>Advanced Conv."]

CONV_PLOTS["convergence_plots.py<br/>Conv. Plots"]

ADAPTIVE_STOP["adaptive_stopping.py<br/>Adaptive Stopping"]

SCENARIO_MGR["scenario_manager.py<br/>Scenarios"]

BENCHMARKING["benchmarking.py<br/>Benchmarks"]

end

%% Configuration dependencies

CONFIG_BASE --> MANUFACTURER

CONFIG_V2 --> CONFIG_MGR

CONFIG_MGR --> CONFIG_LOADER

CONFIG_LOADER --> CONFIG_MGR

%% Business Logic: Decimal utilities feed into accounting modules

DECIMAL_UTILS --> LEDGER

DECIMAL_UTILS --> ACCRUAL

DECIMAL_UTILS --> INS_ACCT

DECIMAL_UTILS --> MANUFACTURER

%% Business Logic: Accounting modules feed into manufacturer

LEDGER --> MANUFACTURER

ACCRUAL --> MANUFACTURER

INS_ACCT --> MANUFACTURER

%% Business Logic: Insurance and exposure relationships

INSURANCE --> INS_PROGRAM

INS_PRICING --> INS_PROGRAM

EXPOSURE --> MANUFACTURER

%% Simulation dependencies

MANUFACTURER --> SIM_CORE

INS_PROGRAM --> SIM_CORE

LOSS_DIST --> SIM_CORE

SIM_CORE --> MONTE_CARLO

MONTE_CARLO --> MONTE_WORKER

STOCHASTIC --> MONTE_CARLO

%% Analysis dependencies

MONTE_CARLO --> ERGODIC_ANALYZER

ERGODIC_ANALYZER --> BUSINESS_OPT

BUSINESS_OPT --> DECISION_ENGINE

%% Validation dependencies

MONTE_CARLO --> ACCURACY_VAL

STRATEGY_BACK --> WALK_FORWARD

%% Risk dependencies

ERGODIC_ANALYZER --> RISK_METRICS

RISK_METRICS --> RUIN_PROB

SENSITIVITY --> PARETO

SENSITIVITY --> SENS_VIZ

%% Infrastructure dependencies

BATCH_PROC --> PARALLEL_EXEC

PARALLEL_EXEC --> MONTE_CARLO

%% Reporting dependencies

RESULT_AGG --> SUMMARY_STATS

SUMMARY_STATS --> EXCEL_REPORT

FINANCIAL_STMT --> EXCEL_REPORT

%% Visualization dependencies

VIZ_CORE --> VIZ_FACTORY

VIZ_STYLE --> VIZ_EXEC

VIZ_STYLE --> VIZ_TECH

VIZ_FACTORY --> VIZ_EXPORT

VIZ_BATCH --> VIZ_CORE

VIZ_INTERACT --> VIZ_CORE

VIZ_TOWER --> VIZ_STYLE

%% Reporting module dependencies

REP_BUILDER --> REP_EXEC

REP_BUILDER --> REP_TECH

REP_SCENARIO --> REP_TABLE

REP_INSIGHT --> REP_EXEC

REP_FORMAT --> REP_TABLE

REP_CACHE --> REP_BUILDER

REP_VALID --> REP_BUILDER

%% Styling

classDef config fill:#e3f2fd,stroke:#1565c0,stroke-width:2px

classDef business fill:#fff9c4,stroke:#f57f17,stroke-width:2px

classDef simulation fill:#f3e5f5,stroke:#6a1b9a,stroke-width:2px

classDef analysis fill:#e8f5e9,stroke:#2e7d32,stroke-width:2px

classDef validation fill:#fce4ec,stroke:#c2185b,stroke-width:2px

classDef risk fill:#fff3e0,stroke:#ef6c00,stroke-width:2px

classDef infra fill:#e0f2f1,stroke:#00695c,stroke-width:2px

classDef reporting fill:#f1f8e9,stroke:#558b2f,stroke-width:2px

classDef viz fill:#e1f5fe,stroke:#0277bd,stroke-width:2px

classDef report fill:#fff8e1,stroke:#f9a825,stroke-width:2px

classDef advanced fill:#fafafa,stroke:#424242,stroke-width:2px

class CONFIG_BASE,CONFIG_V2,CONFIG_MGR,CONFIG_LOADER,CONFIG_MIG config

class MANUFACTURER,INSURANCE,INS_PROGRAM,INS_PRICING,CLAIM_DEV,EXPOSURE,LEDGER,ACCRUAL,INS_ACCT,DECIMAL_UTILS,TRENDS business

class SIM_CORE,MONTE_CARLO,MONTE_WORKER,STOCHASTIC,LOSS_DIST simulation

class ERGODIC_ANALYZER,BUSINESS_OPT,DECISION_ENGINE,OPTIMIZATION,HJB_SOLVER,OPTIMAL_CTRL analysis

class ACCURACY_VAL,STRATEGY_BACK,WALK_FORWARD,VALIDATION_METRICS,STATISTICAL_TESTS validation

class RISK_METRICS,RUIN_PROB,SENSITIVITY,SENS_VIZ,PARETO,BOOTSTRAP risk

class BATCH_PROC,PARALLEL_EXEC,PERF_OPT,TRAJ_STORAGE,PROGRESS_MON,PARAM_SWEEP infra

class VIZ_LEGACY,EXCEL_REPORT,SUMMARY_STATS,RESULT_AGG,FINANCIAL_STMT reporting

class VIZ_CORE,VIZ_EXEC,VIZ_TECH,VIZ_ANNOT,VIZ_STYLE,VIZ_FACTORY,VIZ_EXPORT,VIZ_BATCH,VIZ_INTERACT,VIZ_TOWER viz

class REP_BUILDER,REP_EXEC,REP_TECH,REP_SCENARIO,REP_TABLE,REP_INSIGHT,REP_FORMAT,REP_CACHE,REP_VALID,REP_CONFIG report

class CONVERGENCE,CONV_ADV,CONV_PLOTS,ADAPTIVE_STOP,SCENARIO_MGR,BENCHMARKING advanced

Module Categories

Configuration Management

Handles all configuration aspects including loading, validation, migration, and compatibility between different configuration versions.

Business Logic

Core business domain models including the manufacturer, insurance policies, pricing, claim processing, and financial accounting infrastructure.

ledger.py - Double-entry financial ledger implementing event-sourced transaction tracking. Provides

AccountType,AccountName,EntryType, andTransactionTypeenums along withLedgerEntryandLedgerclasses for GAAP-compliant accounting with full audit trails.accrual_manager.py - Accrual accounting management following GAAP timing principles. Contains

AccrualTypeandPaymentScheduleenums, plusAccrualItemandAccrualManagerclasses for tracking timing differences between cash movements and accounting recognition.insurance_accounting.py - Insurance premium accounting with prepaid asset tracking and systematic amortization. Provides

InsuranceRecoveryandInsuranceAccountingclasses for claim recovery receivables and premium expense management.decimal_utils.py - Decimal precision utilities for financial calculations. Provides

to_decimal,quantize_currency, and related helpers along with constants (ZERO,ONE,PENNY) to prevent floating-point accumulation errors in iterative simulations.trends.py - Trend analysis for insurance claim frequency and severity adjustments. Implements a hierarchy of trend classes (

Trend,NoTrend,LinearTrend,RandomWalkTrend,MeanRevertingTrend,RegimeSwitchingTrend,ScenarioTrend) that apply multiplicative adjustments over time.manufacturer.py - Core financial model containing

ClaimLiability(actuarial claim payment tracking),TaxHandler(tax computation logic), andWidgetManufacturer(main business simulation class).WidgetManufacturerintegrates withLedger,AccrualManager, andInsuranceAccountingfor full double-entry financial modeling.exposure_base.py - Exposure models and the

FinancialStateProviderprotocol. The protocol defines the interface for providing real-time financial state to exposure bases;WidgetManufacturerimplements this protocol.

Simulation Core

The main simulation engine that orchestrates time evolution, Monte Carlo runs, and stochastic processes.

Analysis & Optimization

Advanced analytical tools including ergodic analysis, business optimization, and decision-making engines.

Validation

Comprehensive validation framework for ensuring accuracy and robustness of simulations.

Risk Analysis

Specialized risk assessment tools including ruin probability, sensitivity analysis, and bootstrap methods.

Infrastructure

High-performance computing infrastructure for parallel processing, caching, and data management.

Reporting & Visualization

Output generation including Excel reports, visualizations, and statistical summaries.

Advanced Features

Sophisticated features for convergence monitoring, adaptive stopping, and benchmarking.

Module organization:

Core Financial (4 modules): Central business logic and financial modeling

Insurance & Risk (5 modules): Insurance structures and risk management

Simulation (5 modules): Monte Carlo engine and parallel execution

Analytics (10 modules): Statistical analysis and metrics calculation

Optimization (6 modules): Strategy optimization and control theory

Results (7 modules): Reporting and visualization

Validation (7 modules): Testing and performance validation

Configuration (6 modules): Parameter management and settings

Class Diagrams

Detailed class structures are organized into three main categories:

Core Classes

The core classes diagram shows the fundamental building blocks of the system, including financial models, insurance structures, and simulation components.

Core Classes Diagram

This diagram shows the main classes and their relationships in the core simulation engine. The diagrams are split into focused views for readability: an overview diagram showing high-level relationships, followed by detailed diagrams for the business model, insurance, loss generation, and simulation subsystems.

Overview Diagram

classDiagram

direction TB

class Simulation {

+manufacturer: WidgetManufacturer

+loss_generator: List~ManufacturingLossGenerator~

+insurance_program: InsuranceProgram

+time_horizon: int

+run() SimulationResults

+step_annual(year, losses) dict

+run_with_loss_data() SimulationResults

+get_trajectory() DataFrame

}

class _compare_strategies {

<<module>>

+run_monte_carlo(config, policy, n_scenarios) dict

+compare_strategies(config, policies, n_scenarios) StrategyComparisonResult

}

class MonteCarloEngine {

+loss_generator: ManufacturingLossGenerator

+insurance_program: InsuranceProgram

+manufacturer: WidgetManufacturer

+config: MonteCarloConfig

+run() MonteCarloResults

+export_results(results, filepath)

+compute_bootstrap_confidence_intervals() dict

+run_with_progress_monitoring() MonteCarloResults

+run_with_convergence_monitoring() MonteCarloResults

+estimate_ruin_probability() RuinProbabilityResults

}

class WidgetManufacturer {

+config: ManufacturerConfig

+ledger: Ledger

+insurance_accounting: InsuranceAccounting

+accrual_manager: AccrualManager

+step() MetricsDict

+calculate_revenue() Decimal

+process_insurance_claim() tuple

+check_solvency() bool

+copy() WidgetManufacturer

+reset()

}

class InsuranceProgram {

+layers: List~EnhancedInsuranceLayer~

+deductible: float

+layer_states: List~LayerState~

+calculate_premium() float

+process_claim(amount) dict

+calculate_ergodic_benefit() dict

+optimize_layer_structure() OptimalStructure

}

class InsurancePolicy {

<<deprecated>>

+layers: List~InsuranceLayer~

+deductible: float

+process_claim(amount) tuple

+calculate_premium() float

+to_enhanced_program() InsuranceProgram

}

class ManufacturingLossGenerator {

+attritional: AttritionalLossGenerator

+large: LargeLossGenerator

+catastrophic: CatastrophicLossGenerator

+generate_losses(duration, revenue) tuple

+reseed(seed)

+validate_distributions() dict

}

Simulation --> WidgetManufacturer : simulates

Simulation --> ManufacturingLossGenerator : uses

Simulation --> InsurancePolicy : uses (deprecated)

Simulation --> SimulationResults : produces

MonteCarloEngine --> WidgetManufacturer : copies per path

MonteCarloEngine --> ManufacturingLossGenerator : uses

MonteCarloEngine --> InsuranceProgram : uses

MonteCarloEngine --> MonteCarloResults : produces

_compare_strategies --> MonteCarloEngine : orchestrates MC runs

InsurancePolicy --> InsuranceProgram : converts to (deprecated)

WidgetManufacturer ..|> FinancialStateProvider : implements

Business Model Detail

This diagram shows the internal structure of the manufacturer model, including the financial ledger, tax handling, claim liabilities, and accounting modules.

classDiagram

class WidgetManufacturer {

+config: ManufacturerConfig

+ledger: Ledger

+insurance_accounting: InsuranceAccounting

+accrual_manager: AccrualManager

+stochastic_process: StochasticProcess

+claim_liabilities: List~ClaimLiability~

+is_ruined: bool

+cash: Decimal

+accounts_receivable: Decimal

+inventory: Decimal

+total_assets: Decimal

+equity: Decimal

+step() MetricsDict

+calculate_revenue() Decimal

+calculate_operating_income() Decimal

+calculate_net_income() Decimal

+process_insurance_claim() tuple

+process_uninsured_claim() tuple

+record_insurance_premium(amount)

+record_insurance_loss(amount)

+check_solvency() bool

+handle_insolvency()

+calculate_metrics() MetricsDict

+copy() WidgetManufacturer

+reset()

}

class ClaimLiability {

+original_amount: Decimal

+remaining_amount: Decimal

+year_incurred: int

+is_insured: bool

+development_strategy: ClaimDevelopment

+payment_schedule: List~float~

+get_payment(years_since_incurred) Decimal

+make_payment(amount) Decimal

}

class TaxHandler {

+tax_rate: float

+accrual_manager: AccrualManager

+calculate_tax_liability(income) Decimal

+apply_limited_liability_cap(tax, equity) tuple

+calculate_and_accrue_tax() tuple

}

class ClaimDevelopment {

+pattern_name: str

+development_factors: List~float~

+tail_factor: float

+calculate_payments(amount, accident_yr, payment_yr) float

+get_cumulative_paid(years_since_accident) float

+create_immediate()$ ClaimDevelopment

+create_medium_tail_5yr()$ ClaimDevelopment

+create_long_tail_10yr()$ ClaimDevelopment

+create_very_long_tail_15yr()$ ClaimDevelopment

}

class Ledger {

<<Single Source of Truth>>

+record_transaction()

+get_balance(account) Decimal

+prune_entries(before_date)

}

class AccrualManager {

+record_accrual()

+process_accrued_payments()

+get_total_accruals() Decimal

}

class InsuranceAccounting {

+record_premium()

+record_loss()

+record_recovery()

}

class FinancialStateProvider {

<<Protocol>>

+current_revenue: Decimal

+current_assets: Decimal

+current_equity: Decimal

+base_revenue: Decimal

+base_assets: Decimal

+base_equity: Decimal

}

WidgetManufacturer --> Ledger : owns

WidgetManufacturer --> AccrualManager : owns

WidgetManufacturer --> InsuranceAccounting : owns

WidgetManufacturer --> ClaimLiability : manages 0..*

WidgetManufacturer --> TaxHandler : uses

WidgetManufacturer ..|> FinancialStateProvider : implements

ClaimLiability --> ClaimDevelopment : uses strategy

TaxHandler --> AccrualManager : records accruals

Insurance Subsystem Detail

This diagram shows the primary insurance path (InsuranceProgram / EnhancedInsuranceLayer / LayerState)

and the deprecated basic path (InsurancePolicy / InsuranceLayer).

classDiagram

class InsurancePolicy {

<<deprecated>>

+layers: List~InsuranceLayer~

+deductible: float

+pricing_enabled: bool

+pricer: InsurancePricer

+process_claim(amount) tuple

+calculate_recovery(amount) float

+calculate_premium() float

+get_total_coverage() float

+from_yaml(path)$ InsurancePolicy

+to_enhanced_program() InsuranceProgram

+apply_pricing(revenue)

+create_with_pricing()$ InsurancePolicy

}

class InsuranceLayer {

<<deprecated, dataclass>>

+attachment_point: float

+limit: float

+rate: float

+calculate_recovery(loss_amount) float

+calculate_premium() float

}

class InsuranceProgram {

+name: str

+layers: List~EnhancedInsuranceLayer~

+deductible: float

+layer_states: List~LayerState~

+pricing_enabled: bool

+pricer: InsurancePricer

+calculate_premium() float

+process_claim(amount) dict

+process_annual_claims(claims) dict

+reset_annual()

+get_program_summary() dict

+get_total_coverage() float

+calculate_ergodic_benefit(loss_history) dict

+find_optimal_attachment_points(data) list

+optimize_layer_widths(points, budget) list

+optimize_layer_structure(loss_data) OptimalStructure

+from_yaml(path)$ InsuranceProgram

+create_standard_manufacturing_program()$ InsuranceProgram

+apply_pricing(revenue)

+create_with_pricing()$ InsuranceProgram

+get_pricing_summary() dict

}

class EnhancedInsuranceLayer {

<<dataclass>>

+attachment_point: float

+limit: float

+base_premium_rate: float

+reinstatements: int

+reinstatement_premium: float

+reinstatement_type: ReinstatementType

+aggregate_limit: float

+limit_type: str

+calculate_base_premium() float

+calculate_reinstatement_premium() float

+can_respond(loss_amount) bool

+calculate_layer_loss(total_loss) float

}

class LayerState {

<<dataclass>>

+layer: EnhancedInsuranceLayer

+current_limit: float

+used_limit: float

+is_exhausted: bool

+aggregate_used: float

+process_claim(amount, timing) tuple

+reset()

+get_available_limit() float

+get_utilization_rate() float

}

InsurancePolicy --> InsuranceLayer : contains 1..* (deprecated)

InsurancePolicy ..> InsuranceProgram : converts to (deprecated)

InsuranceProgram --> EnhancedInsuranceLayer : contains 1..*

InsuranceProgram --> LayerState : tracks 1..*

LayerState --> EnhancedInsuranceLayer : wraps

Loss Generation Subsystem

This diagram shows the composite loss generator pattern and the loss event model.

ManufacturingLossGenerator composes three specialized generators for different

severity bands: attritional, large, and catastrophic.

classDiagram

class ManufacturingLossGenerator {

+attritional: AttritionalLossGenerator

+large: LargeLossGenerator

+catastrophic: CatastrophicLossGenerator

+exposure: ExposureBase

+gpd_generator: GeneralizedParetoLoss

+generate_losses(duration, revenue) tuple

+reseed(seed)

+create_simple(freq, mean, std)$ ManufacturingLossGenerator

+validate_distributions() dict

}

class AttritionalLossGenerator {

+frequency: float

+severity: LognormalLoss

+generate_losses(duration, revenue) list

+reseed(seed)

}

class LargeLossGenerator {

+frequency: float

+severity: LognormalLoss

+generate_losses(duration, revenue) list

+reseed(seed)

}

class CatastrophicLossGenerator {

+frequency: float

+severity: ParetoLoss

+generate_losses(duration, revenue) list

+reseed(seed)

}

class LossEvent {

<<dataclass>>

+amount: float

+time: float

+loss_type: str

+description: str

}

class LossDistribution {

<<abstract>>

+rng: Generator

+generate_severity(n)* ndarray

+expected_value()* float

+reset_seed(seed)

}

class LognormalLoss {

+mu: float

+sigma: float

+mean: float

+generate_severity(n) ndarray

+expected_value() float

}

class ParetoLoss {

+alpha: float

+xm: float

+generate_severity(n) ndarray

+expected_value() float

}

ManufacturingLossGenerator *-- AttritionalLossGenerator : composes

ManufacturingLossGenerator *-- LargeLossGenerator : composes

ManufacturingLossGenerator *-- CatastrophicLossGenerator : composes

ManufacturingLossGenerator ..> LossEvent : produces

AttritionalLossGenerator ..> LossEvent : produces

LargeLossGenerator ..> LossEvent : produces

CatastrophicLossGenerator ..> LossEvent : produces

LognormalLoss --|> LossDistribution

ParetoLoss --|> LossDistribution

AttritionalLossGenerator --> LognormalLoss : uses

LargeLossGenerator --> LognormalLoss : uses

CatastrophicLossGenerator --> ParetoLoss : uses

Simulation and Monte Carlo Detail

This diagram shows the simulation orchestration layer, including both the

single-path Simulation class and the multi-path MonteCarloEngine.

classDiagram

class Simulation {

+manufacturer: WidgetManufacturer

+loss_generator: List~ManufacturingLossGenerator~

+insurance_program: InsuranceProgram

+time_horizon: int

+seed: int

+run(progress_interval) SimulationResults

+step_annual(year, losses) dict

+run_with_loss_data(loss_data) SimulationResults

+get_trajectory() DataFrame

}

class _compare_strategies {

<<module>>

+run_monte_carlo(config, policy, n_scenarios) dict

+compare_strategies(config, policies, n_scenarios) StrategyComparisonResult

}

class SimulationResults {

<<dataclass>>

+years: ndarray

+assets: ndarray

+equity: ndarray

+roe: ndarray

+revenue: ndarray

+net_income: ndarray

+claim_counts: ndarray

+claim_amounts: ndarray

+insolvency_year: int

+to_dataframe() DataFrame

+calculate_time_weighted_roe() float

+calculate_rolling_roe(window) ndarray

+summary_stats() dict

}

class MonteCarloEngine {

+loss_generator: ManufacturingLossGenerator

+insurance_program: InsuranceProgram

+manufacturer: WidgetManufacturer

+config: MonteCarloConfig

+convergence_diagnostics: ConvergenceDiagnostics

+parallel_executor: ParallelExecutor

+trajectory_storage: TrajectoryStorage

+run() MonteCarloResults

-_run_sequential() MonteCarloResults

-_run_parallel() MonteCarloResults

-_run_enhanced_parallel() MonteCarloResults

-_calculate_growth_rates(assets) ndarray

-_calculate_metrics(results) dict

-_check_convergence(results) dict

+export_results(results, filepath)

+compute_bootstrap_confidence_intervals(results) dict

+run_with_progress_monitoring() MonteCarloResults

+run_with_convergence_monitoring() MonteCarloResults

+estimate_ruin_probability(config) RuinProbabilityResults

}

class MonteCarloResults {

<<dataclass>>

+final_assets: ndarray

+annual_losses: ndarray

+insurance_recoveries: ndarray

+retained_losses: ndarray

+growth_rates: ndarray

+ruin_probability: dict

+metrics: dict

+convergence: dict

+execution_time: float

+config: MonteCarloConfig

+performance_metrics: PerformanceMetrics

+bootstrap_confidence_intervals: dict

+summary() str

}

class MonteCarloConfig {

<<dataclass>>

+n_simulations: int

+n_years: int

+parallel: bool

+n_workers: int

+seed: int

+use_enhanced_parallel: bool

+insolvency_tolerance: float

}

Simulation --> SimulationResults : produces

MonteCarloEngine --> MonteCarloResults : produces

MonteCarloEngine --> MonteCarloConfig : configured by

_compare_strategies --> MonteCarloEngine : orchestrates MC runs

Class Interactions

sequenceDiagram

participant MC as MonteCarloEngine

participant S as Simulation

participant M as WidgetManufacturer

participant LG as ManufacturingLossGenerator

participant IP as InsuranceProgram

participant SR as SimulationResults

MC->>M: copy() for each path

MC->>LG: reseed() per path

rect rgb(240, 240, 255)

Note over S,SR: Single Simulation Path

loop Each Year

S->>LG: generate_losses(duration, revenue)

LG-->>S: List of LossEvent

loop Each LossEvent

S->>IP: process_claim(amount)

IP-->>S: recovery details dict

S->>M: record_insurance_loss(retained)

S->>M: record_insurance_premium(premium)

end

S->>M: step(growth_rate)

M->>M: calculate_revenue()

M->>M: calculate_operating_income()

M->>M: calculate_net_income()

M->>M: check_solvency()

M-->>S: MetricsDict

alt Insolvent

M->>M: handle_insolvency()

S-->>MC: Early termination

end

end

S->>SR: Compile results

end

SR-->>MC: Path results

MC->>MC: Aggregate all paths

MC->>MC: Calculate risk metrics

MC->>MC: Check convergence

Key Design Patterns

1. Strategy Pattern

ClaimLiabilityusesClaimDevelopmentas a payment strategyInsurance structures can use different pricing engines (

InsurancePricer)Loss generators use pluggable severity distributions (

LossDistribution)

2. Composite Pattern

ManufacturingLossGeneratorcomposesAttritionalLossGenerator,LargeLossGenerator, andCatastrophicLossGeneratorInsuranceProgrammanages multipleEnhancedInsuranceLayerinstances

3. Protocol (Structural Typing)

FinancialStateProviderprotocol enables exposure-based classes to query live financial state fromWidgetManufacturerwithout tight couplingImplemented via Python

typing.Protocolfor duck-typed structural subtyping

4. Factory Pattern

ManufacturingLossGenerator.create_simple()for easy setupInsuranceProgram.create_standard_manufacturing_program()for standard configurationsClaimDevelopment.create_immediate(),create_medium_tail_5yr(), etc. for preset patternsInsurancePolicy.create_with_pricing()andInsuranceProgram.create_with_pricing()for priced programs

5. Event Sourcing

Ledgerserves as the single source of truth for all balance sheet accountsAll financial mutations go through ledger transactions

Balance sheet values are derived from ledger state, not stored independently

6. Observer Pattern

ProgressMonitorobserves Monte Carlo simulation progressConvergenceDiagnosticsmonitors chain convergence during execution

7. Facade Pattern

MonteCarloEngineprovides a simplified interface to complex parallel execution, checkpointing, and aggregationInsuranceProgramfacades complex multi-layer claim allocation with reinstatements

Key components:

WidgetManufacturer: Central financial model with balance sheet evolution

StochasticProcess: Abstract base for various volatility models (GBM, OU, Lognormal)

InsuranceProgram: Multi-layer insurance structure implementation

ClaimGenerator: Loss event generation with configurable distributions

Data Models

The data models diagram illustrates configuration structures, result objects, and data transfer objects used throughout the system.

Data Models and Analysis Classes

This document shows the data structures and analysis models used throughout the system. The diagrams are split into focused sections for readability.

Ergodic Analysis

The ergodic analysis subsystem implements Ole Peters’ ergodic economics framework, comparing time-average versus ensemble-average growth rates to demonstrate how insurance transforms business growth dynamics.

classDiagram

class ErgodicAnalyzer {

-convergence_threshold: float

+calculate_time_average_growth(trajectories) dict

+calculate_ensemble_average(trajectories) dict

+compare_scenarios(insured, uninsured, metric) dict

+check_convergence(values, window_size) tuple

+analyze_simulation_batch(results, label) dict

+integrate_loss_ergodic_analysis(loss_data, insurance, manufacturer) ErgodicAnalysisResults

+validate_insurance_ergodic_impact(...) ValidationResults

+significance_test(insured_growth, uninsured_growth) dict

}

class ErgodicData {

<<dataclass>>

+time_series: ndarray

+values: ndarray

+metadata: dict

+validate() bool

}

class ErgodicAnalysisResults {

<<dataclass>>

+time_average_growth: float

+ensemble_average_growth: float

+survival_rate: float

+ergodic_divergence: float

+insurance_impact: dict

+validation_passed: bool

+metadata: dict

}

class ValidationResults {

<<dataclass>>

+is_valid: bool

+checks: dict

+warnings: list

+summary: str

}

ErgodicAnalyzer --> ErgodicData : accepts

ErgodicAnalyzer --> ErgodicAnalysisResults : produces

ErgodicAnalyzer --> ValidationResults : validates with

ErgodicAnalysisResults --> ErgodicData : derived from

ErgodicAnalyzer is the core analysis engine. It accepts trajectories as ErgodicData or SimulationResults, calculates time-average and ensemble-average growth rates, performs convergence checks, and runs integrated loss-ergodic analysis. The compare_scenarios() method is the primary entry point for comparing insured versus uninsured outcomes.

ErgodicData is a lightweight dataclass holding time series arrays and metadata. It validates array length consistency before analysis.

ErgodicAnalysisResults captures the complete output of an integrated analysis, including growth rates, survival statistics, insurance impact metrics, and validation status.

Business Optimization

The optimization subsystem uses ergodic metrics to find insurance strategies that maximize real business outcomes such as ROE, growth rate, and survival probability.

classDiagram

class BusinessOptimizer {

-manufacturer: WidgetManufacturer

-loss_distribution: LossDistribution

-decision_engine: InsuranceDecisionEngine

-ergodic_analyzer: ErgodicAnalyzer

-optimizer_config: BusinessOptimizerConfig

+maximize_roe_with_insurance(constraints, time_horizon) OptimalStrategy

+minimize_bankruptcy_risk(growth_targets, budget) OptimalStrategy

+optimize_capital_efficiency(constraints) OptimalStrategy

+optimize_business_outcomes(objectives, constraints) BusinessOptimizationResult

}

class OptimalStrategy {

<<dataclass>>

+coverage_limit: float

+deductible: float

+premium_rate: float

+expected_roe: float

+bankruptcy_risk: float

+growth_rate: float

+capital_efficiency: float

+recommendations: list~str~

+to_dict() dict

}

class BusinessObjective {

<<dataclass>>

+name: str

+weight: float

+target_value: float

+optimization_direction: OptimizationDirection

+constraint_type: str

+constraint_value: float

}

class BusinessConstraints {

<<dataclass>>

+max_risk_tolerance: float

+min_roe_threshold: float

+max_leverage_ratio: float

+min_liquidity_ratio: float

+max_premium_budget: float

+min_coverage_ratio: float

+regulatory_requirements: dict

}

class BusinessOptimizationResult {

<<dataclass>>

+optimal_strategy: OptimalStrategy

+objective_values: dict

+constraint_satisfaction: dict

+convergence_info: dict

+sensitivity_analysis: dict

+is_feasible() bool

}

BusinessOptimizer --> OptimalStrategy : finds

BusinessOptimizer --> BusinessObjective : uses

BusinessOptimizer --> BusinessConstraints : respects

BusinessOptimizer --> BusinessOptimizationResult : produces

BusinessOptimizationResult --> OptimalStrategy : contains

BusinessOptimizer provides multiple optimization methods: maximize_roe_with_insurance() for ROE-focused optimization, minimize_bankruptcy_risk() for safety-first strategies, optimize_capital_efficiency() for capital allocation, and optimize_business_outcomes() for multi-objective optimization using BusinessObjective definitions.

OptimalStrategy is the output dataclass capturing the recommended insurance parameters (coverage limit, deductible, premium rate) along with expected business outcomes and actionable recommendations.

Risk Analysis

Risk metrics and ruin probability analysis provide the quantitative foundation for evaluating tail risk and insurance value.

classDiagram

class RiskMetrics {

-losses: ndarray

-weights: ndarray

-rng: Generator

+var(confidence, method, bootstrap_ci) float

+tvar(confidence) float

+expected_shortfall(confidence) float

+pml(return_period) float

+maximum_drawdown() float

+economic_capital(confidence) float

+tail_index(threshold) float

+risk_adjusted_metrics() dict

+coherence_test() dict

+summary_statistics() dict

+plot_distribution()

}

class RiskMetricsResult {

<<dataclass>>

+metric_name: str

+value: float

+confidence_level: float

+confidence_interval: tuple

+metadata: dict

}

class RuinProbabilityAnalyzer {

-manufacturer: WidgetManufacturer

-loss_generator: ManufacturingLossGenerator

-insurance_program: InsuranceProgram

-config: MonteCarloConfig

+analyze_ruin_probability(config) RuinProbabilityResults

}

class RuinProbabilityResults {

<<dataclass>>

+time_horizons: ndarray

+ruin_probabilities: ndarray

+confidence_intervals: ndarray

+bankruptcy_causes: dict

+survival_curves: ndarray

+execution_time: float

+n_simulations: int

+convergence_achieved: bool

+mid_year_ruin_count: int

+ruin_month_distribution: dict

+summary() str

}

class RuinProbabilityConfig {

<<dataclass>>

+time_horizons: list~int~

+n_simulations: int

+min_assets_threshold: float

+min_equity_threshold: float

+early_stopping: bool

+parallel: bool

+n_workers: int

+seed: int

+n_bootstrap: int

}

RiskMetrics --> RiskMetricsResult : returns

RuinProbabilityAnalyzer --> RuinProbabilityResults : produces

RuinProbabilityAnalyzer --> RuinProbabilityConfig : configured by

RiskMetrics is initialized with a loss array and provides VaR, TVaR (CVaR), Expected Shortfall, PML, Maximum Drawdown, and other tail-risk measures. It supports both empirical and parametric methods with optional bootstrap confidence intervals.

RuinProbabilityAnalyzer runs Monte Carlo ruin analysis across multiple time horizons, with support for parallel execution, bootstrap confidence intervals, and mid-year ruin tracking.

Convergence Diagnostics

Convergence analysis ensures Monte Carlo simulations have run long enough to produce reliable results.

classDiagram

class ConvergenceDiagnostics {

-r_hat_threshold: float

-min_ess: int

-relative_mcse_threshold: float

+calculate_r_hat(chains) float

+calculate_ess(chain, max_lag) float

+calculate_batch_ess(chains, method) float

+calculate_ess_per_second(chain, time) float

+calculate_mcse(chain, ess) float

+check_convergence(chains, metric_names) dict

+geweke_test(chain) tuple

+heidelberger_welch_test(chain, alpha) dict

}

class ConvergenceStats {

<<dataclass>>

+r_hat: float

+ess: float

+mcse: float

+converged: bool

+n_iterations: int

+autocorrelation: float

}

ConvergenceDiagnostics --> ConvergenceStats : produces

ConvergenceDiagnostics implements Gelman-Rubin R-hat, Effective Sample Size (ESS), Monte Carlo Standard Error (MCSE), Geweke test, and Heidelberger-Welch stationarity test. The check_convergence() method returns a ConvergenceStats dataclass for each metric being tracked.

Loss Modeling

The loss modeling subsystem uses a composite pattern to combine attritional, large, and catastrophic loss generators into a unified manufacturing risk model.

classDiagram

class LossDistribution {

<<abstract>>

#rng: Generator

+generate_severity(n_samples)* ndarray

+expected_value()* float

+reset_seed(seed) void

}

class LognormalLoss {

+mean: float

+cv: float

+mu: float

+sigma: float

+generate_severity(n_samples) ndarray

+expected_value() float

}

class ParetoLoss {

+alpha: float

+xm: float

+generate_severity(n_samples) ndarray

+expected_value() float

}

class GeneralizedParetoLoss {

+severity_shape: float

+severity_scale: float

+generate_severity(n_samples) ndarray

+expected_value() float

}

class LossEvent {

<<dataclass>>

+amount: float

+time: float

+loss_type: str

+description: str

}

class LossData {

<<dataclass>>

+timestamps: ndarray

+loss_amounts: ndarray

+loss_types: list~str~

+claim_ids: list~str~

+development_factors: ndarray

+metadata: dict

+validate() bool

+to_ergodic_format() ErgodicData

+apply_insurance(program) LossData

+from_loss_events(events)$ LossData

+to_loss_events() list~LossEvent~

+get_annual_aggregates(years) dict

+calculate_statistics() dict

}

LossDistribution <|-- LognormalLoss

LossDistribution <|-- ParetoLoss

LossDistribution <|-- GeneralizedParetoLoss

LossData --> LossEvent : converts to/from

LossDistribution is the abstract base class defining the interface for severity distributions. The three concrete implementations (Lognormal, Pareto, Generalized Pareto) cover the full spectrum from attritional to extreme tail modeling.

LossEvent is a lightweight dataclass representing a single loss occurrence with timing, amount, and type classification. LossData is the unified data container for cross-module compatibility, providing conversion to ergodic format and insurance application methods.

Loss Generation (Composite Pattern)

The manufacturing loss generator uses the Composite pattern to combine multiple loss layer generators, each with independent frequency and severity models.

classDiagram

class ManufacturingLossGenerator {

+attritional: AttritionalLossGenerator

+large: LargeLossGenerator

+catastrophic: CatastrophicLossGenerator

+gpd_generator: GeneralizedParetoLoss

+threshold_value: float

+exposure: ExposureBase

+generate_losses(duration, revenue) tuple

+reseed(seed) void

+create_simple(frequency, severity_mean, severity_std, seed)$ ManufacturingLossGenerator

+validate_distributions(n_simulations) dict

}

class AttritionalLossGenerator {

+frequency_generator: FrequencyGenerator

+severity_distribution: LognormalLoss

+loss_type: str

+generate_losses(duration, revenue) list~LossEvent~

+reseed(seed) void

}

class LargeLossGenerator {

+frequency_generator: FrequencyGenerator

+severity_distribution: LognormalLoss

+loss_type: str

+generate_losses(duration, revenue) list~LossEvent~

+reseed(seed) void

}

class CatastrophicLossGenerator {

+frequency_generator: FrequencyGenerator

+severity_distribution: ParetoLoss

+loss_type: str

+generate_losses(duration, revenue) list~LossEvent~

+reseed(seed) void

}

class FrequencyGenerator {

+base_frequency: float

+revenue_scaling_exponent: float

+reference_revenue: float

-rng: Generator

+reseed(seed) void

+get_scaled_frequency(revenue) float

+generate_event_times(duration, revenue) ndarray

}

ManufacturingLossGenerator *-- AttritionalLossGenerator : composes

ManufacturingLossGenerator *-- LargeLossGenerator : composes

ManufacturingLossGenerator *-- CatastrophicLossGenerator : composes

ManufacturingLossGenerator o-- GeneralizedParetoLoss : optional extreme

AttritionalLossGenerator --> FrequencyGenerator : uses

LargeLossGenerator --> FrequencyGenerator : uses

CatastrophicLossGenerator --> FrequencyGenerator : uses

AttritionalLossGenerator --> LognormalLoss : severity

LargeLossGenerator --> LognormalLoss : severity

CatastrophicLossGenerator --> ParetoLoss : severity

ManufacturingLossGenerator is the composite orchestrator that combines three loss layers (attritional, large, catastrophic) with optional GPD extreme value transformation. The create_simple() class method provides a migration-friendly factory for basic use cases. Each sub-generator pairs a FrequencyGenerator (Poisson process with revenue scaling) with a LossDistribution for severities.

Sensitivity Analysis

Sensitivity tools analyze how parameter changes affect optimization outcomes, with built-in caching for computational efficiency.

classDiagram

class SensitivityAnalyzer {

-base_config: dict

-optimizer: Any

-results_cache: dict

-cache_dir: Path

+analyze_parameter(param_name, param_range, n_points) SensitivityResult

+create_tornado_diagram(parameters, metric) dict

+analyze_parameter_group(params, metric) dict

}

class SensitivityResult {

<<dataclass>>

+parameter: str

+baseline_value: float

+variations: ndarray

+metrics: dict

+parameter_path: str

+units: str

+calculate_impact(metric) float

+get_metric_bounds(metric) tuple

+to_dataframe() DataFrame

}

class TwoWaySensitivityResult {

<<dataclass>>

+parameter1: str

+parameter2: str

+values1: ndarray

+values2: ndarray

+metric_grid: ndarray

+metric_name: str

+find_optimal_region(target, tolerance) ndarray

+to_dataframe() DataFrame

}

SensitivityAnalyzer --> SensitivityResult : produces

SensitivityAnalyzer --> TwoWaySensitivityResult : produces

SensitivityAnalyzer provides one-way parameter analysis, tornado diagram generation, and parameter group analysis. It uses MD5-based caching to avoid redundant optimizer runs. Results are captured as SensitivityResult (one-way) or TwoWaySensitivityResult (two-way interaction) dataclasses with built-in DataFrame conversion.

Financial Statements

The financial statement subsystem generates GAAP-compliant Balance Sheet, Income Statement, and Cash Flow Statement from simulation data, with support for both indirect and direct (ledger-based) cash flow methods.

classDiagram

class FinancialStatementGenerator {

-manufacturer: WidgetManufacturer

-manufacturer_data: dict

-config: FinancialStatementConfig

-metrics_history: list

-years_available: int

-ledger: Ledger

+generate_balance_sheet(year) DataFrame

+generate_income_statement(year) DataFrame

+generate_cash_flow_statement(year) DataFrame

+generate_reconciliation_report(year) DataFrame

}

class CashFlowStatement {

-metrics_history: list

-config: Any

-ledger: Ledger

+generate_statement(year, period, method) DataFrame

}

class FinancialStatementConfig {

<<dataclass>>

+currency_symbol: str

+decimal_places: int

+include_yoy_change: bool

+include_percentages: bool

+fiscal_year_end: int

+consolidate_monthly: bool

}

FinancialStatementGenerator --> CashFlowStatement : delegates to

FinancialStatementGenerator --> FinancialStatementConfig : configured by

FinancialStatementGenerator ..> WidgetManufacturer : reads from

FinancialStatementGenerator is the primary entry point, accepting a WidgetManufacturer (or raw data dictionary) and generating formatted DataFrames for each financial statement. It supports ledger-based direct method cash flow when a Ledger is available. The generate_reconciliation_report() method validates the accounting equation and solvency checks.

CashFlowStatement handles the three-section cash flow statement (Operating, Investing, Financing) with both indirect and direct method support.

Data Flow Sequence

sequenceDiagram

participant LG as ManufacturingLossGenerator

participant Sim as Simulation

participant EA as ErgodicAnalyzer

participant BO as BusinessOptimizer

participant SA as SensitivityAnalyzer

participant RM as RiskMetrics

participant FS as FinancialStatementGenerator

LG->>Sim: Generate losses (attritional + large + catastrophic)

Sim->>EA: Trajectory data (insured & uninsured)

EA->>EA: Calculate time-average growth

EA->>EA: Calculate ensemble-average growth

EA->>RM: Loss data for tail risk

RM-->>EA: VaR, TVaR, drawdown metrics

EA-->>BO: Ergodic metrics & analysis results

BO->>BO: Define objectives & constraints

BO->>SA: Request parameter sensitivity

SA->>SA: Parameter sweep with caching

SA-->>BO: SensitivityResult

BO->>BO: Find optimal strategy via scipy.optimize

BO-->>BO: OptimalStrategy

BO->>FS: Generate financial statements

FS->>FS: Build balance sheet

FS->>FS: Build income statement

FS->>FS: Build cash flow statement

FS-->>BO: Formatted DataFrames

Key Design Patterns

1. Composite Pattern

ManufacturingLossGeneratorcomposesAttritionalLossGenerator,LargeLossGenerator, andCatastrophicLossGeneratorinto a unified interfaceEach sub-generator independently pairs a

FrequencyGeneratorwith aLossDistribution

2. Template Method (Abstract Base Class)

LossDistribution(ABC) defines the interface withgenerate_severity()andexpected_value()as abstract methodsLognormalLoss,ParetoLoss, andGeneralizedParetoLossimplement distribution-specific behavior

3. Dataclass Data Transfer Objects

ErgodicData,ErgodicAnalysisResults,OptimalStrategy,LossEvent,LossData,ConvergenceStats,RuinProbabilityResults,SensitivityResultall use@dataclassfor clean data transfer between modules

4. Factory Method

ManufacturingLossGenerator.create_simple()provides a simplified factory for migration from legacyClaimGeneratorLossData.from_loss_events()constructs data from a list ofLossEventobjects

5. Strategy Pattern

BusinessOptimizersupports multiple optimization strategies: ROE maximization, bankruptcy risk minimization, capital efficiency optimization, and multi-objective optimizationEach strategy uses different objective functions with

scipy.optimize

6. Caching

SensitivityAnalyzeruses MD5-based in-memory and persistent disk caching to avoid redundant optimization runs during parameter sweeps

Key structures:

Config: Pydantic-based configuration with validation

SimulationResults: Comprehensive result aggregation

ValidationMetrics: Performance and accuracy metrics

StateManagement: System state and progress tracking

Service Layer

The service layer diagram shows high-level services that orchestrate the core components, including analytics, optimization, and validation services.

Service Layer and Infrastructure

This document shows the service layer components that provide infrastructure support for the core simulation and analysis. Classes are grouped into logical sections reflecting their roles in the system.

Batch Processing Services

The batch processing subsystem coordinates parallel execution of multiple simulation scenarios with checkpointing and result aggregation.

classDiagram

class BatchProcessor {

-loss_generator: ManufacturingLossGenerator

-insurance_program: InsuranceProgram

-manufacturer: WidgetManufacturer

-n_workers: Optional~int~

-checkpoint_dir: Path

-use_parallel: bool

-progress_bar: bool

-batch_results: List~BatchResult~

-completed_scenarios: Set~str~

-failed_scenarios: Set~str~

+process_batch(scenarios, resume_from_checkpoint, checkpoint_interval, max_failures) AggregatedResults

+export_results(path, export_format)

+export_financial_statements(path)

+clear_checkpoints()

-_process_serial(scenarios, checkpoint_interval, max_failures) List~BatchResult~

-_process_parallel(scenarios, checkpoint_interval, max_failures) List~BatchResult~

-_process_scenario(scenario) BatchResult

-_aggregate_results() AggregatedResults

-_save_checkpoint()

-_load_checkpoint() bool

-_perform_sensitivity_analysis() Optional~DataFrame~

}

class ParallelExecutor {

-n_workers: int

-cpu_profile: CPUProfile

-chunking_strategy: ChunkingStrategy

-shared_memory_config: SharedMemoryConfig

-shared_memory_manager: SharedMemoryManager

-monitor_performance: bool

-performance_metrics: PerformanceMetrics

+map_reduce(work_function, work_items, reduce_function, shared_data, progress_bar) Any

+get_performance_report() str

-_setup_shared_data(shared_data) Dict

-_calculate_chunk_size(n_items, work_function) int

-_profile_work_complexity(work_function) float

-_create_chunks(work_items, chunk_size) List

-_execute_parallel(work_function, chunks, shared_refs, progress_bar) List

-_update_memory_metrics()

}

class SmartCache {

-cache: Dict~Tuple, Any~

-max_size: int

-hits: int

-misses: int

-access_counts: Dict~Tuple, int~

+get(key: Tuple) Optional~Any~

+set(key: Tuple, value: Any)

+clear()

+hit_rate() float

}

class ScenarioManager {

-scenarios: Dict~str, ScenarioConfig~

-parameter_specs: List~ParameterSpec~

+add_scenario(name, scenario)

+get_scenario(name) ScenarioConfig

+generate_scenarios(method, specs) List~ScenarioConfig~

+generate_sensitivity_scenarios(specs) List~ScenarioConfig~

+export_scenarios(path)

}

BatchProcessor --> ParallelExecutor : distributes work via

BatchProcessor --> ScenarioManager : gets scenarios from

BatchProcessor ..> SmartCache : caches results in

Monitoring Services

Monitoring services track simulation progress, convergence behavior, and provide real-time feedback during long-running computations.

classDiagram

class ProgressMonitor {

-total_iterations: int

-check_intervals: List~int~

-update_frequency: int

-show_console: bool

-convergence_threshold: float

-start_time: float

-current_iteration: int

-convergence_checks: List~Tuple~

-converged: bool

-converged_at: Optional~int~

-monitor_overhead: float

+update(iteration, convergence_value) bool

+get_stats() ProgressStats

+generate_convergence_summary() Dict

+finish() ProgressStats

+finalize()

+get_overhead_percentage() float

+reset()

}

class ConvergenceDiagnostics {

-r_hat_threshold: float

-min_ess: int

-relative_mcse_threshold: float

+calculate_r_hat(chains) float

+calculate_ess(chain, max_lag) float

+calculate_batch_ess(chains, method) float

+calculate_ess_per_second(chain, computation_time) float

+calculate_mcse(chain, ess) float

+check_convergence(chains, metric_names) Dict~str, ConvergenceStats~

+geweke_test(chain, first_fraction, last_fraction) Tuple

+heidelberger_welch_test(chain, alpha) Dict

}

class AdvancedConvergenceDiagnostics {

-fft_size: Optional~int~

+calculate_autocorrelation_full(chain, max_lag, method) AutocorrelationAnalysis

+calculate_spectral_density(chain, method, nperseg) SpectralDiagnostics

+calculate_ess_batch_means(chain, batch_size, n_batches) float

+calculate_ess_overlapping_batch(chain, batch_size) float

+heidelberger_welch_advanced(chain, alpha, eps) Dict

+raftery_lewis_diagnostic(chain, q, r, s) Dict

}

ConvergenceDiagnostics <|-- AdvancedConvergenceDiagnostics : extends

ProgressMonitor ..> ConvergenceDiagnostics : uses convergence values from

Storage Services

Storage services handle memory-efficient persistence of simulation trajectories and time-series data using memory-mapped arrays or HDF5.

classDiagram

class TrajectoryStorage {

-config: StorageConfig

-storage_path: Path

-_summaries: Dict~int, SimulationSummary~

-_memmap_files: Dict~str, memmap~

-_hdf5_file: Optional~File~

-_total_simulations: int

-_disk_usage: float

+store_simulation(sim_id, annual_losses, insurance_recoveries, retained_losses, final_assets, initial_assets, ruin_occurred, ruin_year)

+load_simulation(sim_id, load_time_series) Dict

+export_summaries_csv(output_path)

+export_summaries_json(output_path)

+get_storage_stats() Dict

+clear_storage()

-_setup_memmap()

-_setup_hdf5()

-_store_summary(summary)

-_store_time_series(sim_id, annual_losses, insurance_recoveries, retained_losses)

-_persist_summaries()

-_check_disk_space() bool

-_cleanup_memory()

}

class StorageConfig {

+storage_dir: str

+backend: str

+sample_interval: int

+max_disk_usage_gb: float

+compression: bool

+compression_level: int

+chunk_size: int

+enable_summary_stats: bool

+enable_time_series: bool

+dtype: Any

}

TrajectoryStorage --> StorageConfig : configured by

Parameter Sweep Services

Parameter sweep services enable systematic exploration of the parameter space through grid search, adaptive refinement, and scenario comparison.

classDiagram

class ParameterSweeper {

-optimizer: Optional~BusinessOptimizer~

-cache_dir: Path

-results_cache: Dict

-use_parallel: bool

+sweep(config, progress_callback) DataFrame

+create_scenarios() Dict~str, SweepConfig~

+find_optimal_regions(results, objective, constraints, top_percentile) Tuple

+compare_scenarios(results, metrics, normalize) DataFrame

+load_results(sweep_hash) Optional~DataFrame~

+export_results(results, output_file, file_format)

-_run_single(params, metrics) Dict

-_apply_adaptive_refinement(initial_results, config) DataFrame

-_save_results(df, config)

}

class SweepConfig {

+parameters: Dict~str, List~

+fixed_params: Dict~str, Any~

+metrics_to_track: List~str~

+n_workers: Optional~int~

+batch_size: int

+adaptive_refinement: bool

+refinement_threshold: float

+save_intermediate: bool

+cache_dir: str

+generate_grid() List~Dict~

+estimate_runtime(seconds_per_run) str

}

ParameterSweeper --> SweepConfig : configured by

ParameterSweeper --> ParallelExecutor : parallelizes with

Performance and Optimization Services

Performance services provide profiling, benchmarking, and optimization capabilities to ensure simulations run within target times and memory budgets.

classDiagram

class PerformanceOptimizer {

-config: OptimizationConfig

-cache: SmartCache