High-Level System Context Diagram

Executive Summary

The Ergodic Insurance Limits framework analyzes insurance decisions using time-average (ergodic) theory rather than traditional ensemble averages. This approach reveals that insurance can enhance business growth even when premiums exceed expected losses by 200-500%, transforming insurance from a cost center to a growth enabler.

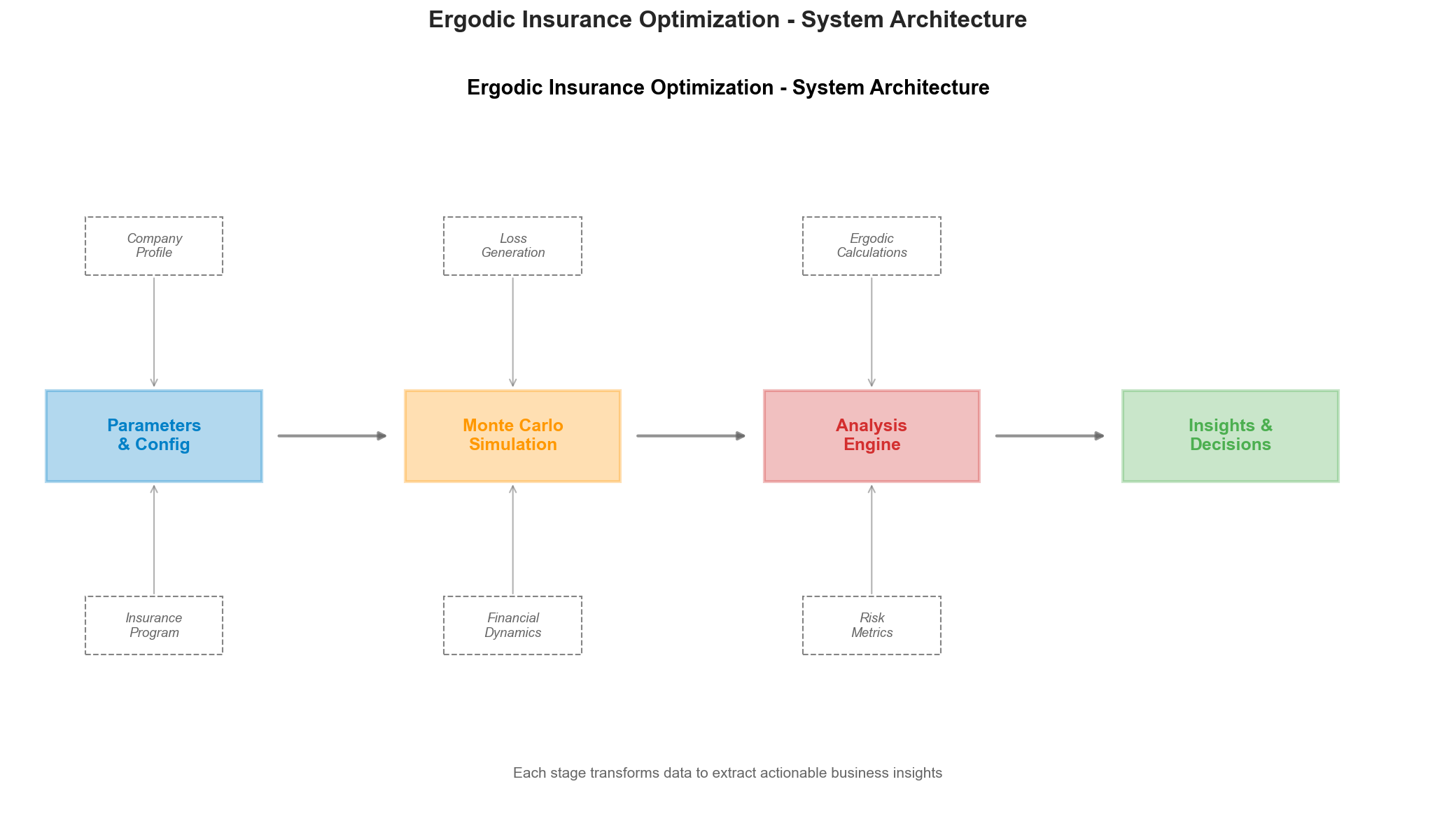

Simplified System Architecture

flowchart LR

%% Simplified Executive View

INPUT[("📊 Market Data<br/>& Configuration")]

BUSINESS[("🏭 Business<br/>Simulation")]

ERGODIC[("📈 Ergodic<br/>Analysis")]

OPTIMIZE[("🎯 Strategy<br/>Optimization")]

OUTPUT[("📑 Reports &<br/>Insights")]

INPUT --> BUSINESS

BUSINESS --> ERGODIC

ERGODIC --> OPTIMIZE

OPTIMIZE --> OUTPUT

%% Styling

classDef inputStyle fill:#e3f2fd,stroke:#0d47a1,stroke-width:3px,font-size:14px

classDef processStyle fill:#f3e5f5,stroke:#4a148c,stroke-width:3px,font-size:14px

classDef outputStyle fill:#e8f5e9,stroke:#1b5e20,stroke-width:3px,font-size:14px

class INPUT inputStyle

class BUSINESS,ERGODIC,OPTIMIZE processStyle

class OUTPUT outputStyle

Key Innovation: By comparing time-average growth (what one business experiences over time) with ensemble-average growth (statistical average across many businesses), the framework demonstrates that insurance fundamentally transforms the growth dynamics of volatile businesses.

System Architecture Overview (Detailed)

The actual implementation follows a sophisticated multi-layer architecture:

graph TB

%% Input Layer

subgraph Inputs["📥 Input Layer"]

CONF["Configuration<br/>(YAML/JSON)"]

HIST["Historical Loss Data"]

PARAMS["Business Parameters"]

end

%% Core Simulation

subgraph Core["⚙️ Core Simulation Engine"]

MANU["WidgetManufacturer<br/>(Business Model)"]

LOSSG["ManufacturingLossGenerator<br/>(Loss Events)"]

INS["InsuranceProgram<br/>(Coverage Tower)"]

SIM["Simulation Engine<br/>(Time Evolution)"]

end

%% Financial Core

subgraph Financial["💰 Financial Core"]

LEDGER["Ledger<br/>(Double-Entry Accounting)"]

ACCRUAL["AccrualManager<br/>(Accrual Timing)"]

INSACCT["InsuranceAccounting<br/>(Premium Amortization)"]

TAXH["TaxHandler<br/>(Tax Calculations)"]

DECUTIL["decimal_utils<br/>(Decimal Precision)"]

end

%% Analysis Layer

subgraph Analysis["📊 Analysis & Optimization"]

MONTE["Monte Carlo Engine<br/>(10,000+ paths)"]

ERGODIC["Ergodic Analyzer<br/>(Time vs Ensemble)"]

OPT["Business Optimizer<br/>(Strategy Selection)"]

SENS["Sensitivity Analysis<br/>(Parameter Impact)"]

end

%% Output Layer

subgraph Outputs["📤 Output & Insights"]

EXCEL["Excel Reports<br/>(Detailed Results)"]

VIZ["Visualizations<br/>(Executive & Technical)"]

METRICS["Risk Metrics<br/>(VaR, CVaR, Ruin Prob)"]

STRATEGY["Optimal Strategy<br/>(Limits & Retentions)"]

end

%% Data Flow

Inputs --> Core

Core --> MONTE

MONTE --> Analysis

Analysis --> Outputs

%% Key Connections

MANU -.-> INS

LOSSG -.-> INS

INS -.-> SIM

SIM -.-> MONTE

ERGODIC -.-> OPT

OPT -.-> SENS

%% Financial Core Connections

MANU --> LEDGER

MANU --> ACCRUAL

MANU --> INSACCT

TAXH --> ACCRUAL

LEDGER --> DECUTIL

ACCRUAL --> DECUTIL

INSACCT --> DECUTIL

classDef inputClass fill:#e3f2fd,stroke:#1565c0

classDef coreClass fill:#fff3e0,stroke:#ef6c00

classDef financialClass fill:#fff9c4,stroke:#f9a825

classDef analysisClass fill:#f3e5f5,stroke:#7b1fa2

classDef outputClass fill:#e8f5e9,stroke:#2e7d32

class CONF,HIST,PARAMS inputClass

class MANU,LOSSG,INS,SIM coreClass

class LEDGER,ACCRUAL,INSACCT,TAXH,DECUTIL financialClass

class MONTE,ERGODIC,OPT,SENS analysisClass

class EXCEL,VIZ,METRICS,STRATEGY outputClass

Reference to System Architecture Diagram

For a visual representation, see: assets/system_architecture.png

{kind=link}

The PNG diagram shows the simplified flow, while the detailed architecture above reflects the actual implementation with all major components.

Detailed System Architecture

This diagram shows the overall architecture of the Ergodic Insurance Limits framework, including the main components, external dependencies, and data flow between major modules.

flowchart TB

%% External Inputs and Configurations

subgraph External["External Inputs"]

CONFIG[("Configuration Files<br/>YAML/JSON")]

MARKET[("Market Data<br/>Loss Distributions")]

PARAMS[("Business Parameters<br/>Financial Metrics")]

end

%% Core System Components

subgraph Core["Core Simulation Engine"]

SIM["Simulation<br/>Engine"]

MANU["Widget<br/>Manufacturer<br/>Model"]

LOSSG["Manufacturing<br/>Loss Generator"]

INS["Insurance<br/>Program"]

end

%% Financial Accounting Subsystem

subgraph FinAcct["Financial Accounting Subsystem"]

LEDGER["Ledger<br/>(Double-Entry)"]

ACCRUAL["AccrualManager<br/>(GAAP Timing)"]

INSACCT["InsuranceAccounting<br/>(Premium & Recovery)"]

TAXH["TaxHandler<br/>(Tax Accruals)"]

DECUTIL["decimal_utils<br/>(Precision)"]

end

%% Insurance Subsystem

subgraph InsuranceSub["Insurance Subsystem"]

INSPOL["InsurancePolicy<br/>(Deprecated)"]

INSLAY["InsuranceLayer<br/>(Deprecated)"]

INSPROG["InsuranceProgram<br/>(Primary)"]

ENHLAY["EnhancedInsuranceLayer<br/>(Primary)"]

PRICER["InsurancePricer<br/>(Market Cycles)"]

end

%% Exposure & Trend System

subgraph ExposureSub["Exposure & Trend System"]

EXPBASE["ExposureBase<br/>(Dynamic Frequency)"]

FSPROV["FinancialStateProvider<br/>(Protocol)"]

TRENDS["trends.py<br/>(Trend Analysis)"]

end

%% Analysis and Optimization

subgraph Analysis["Analysis & Optimization"]

ERGODIC["Ergodic<br/>Analyzer"]

OPT["Business<br/>Optimizer"]

MONTE["Monte Carlo<br/>Engine"]

SENS["Sensitivity<br/>Analyzer"]

end

%% Validation and Testing

subgraph Validation["Validation & Testing"]

ACC["Accuracy<br/>Validator"]

BACK["Strategy<br/>Backtester"]

WALK["Walk-Forward<br/>Validator"]

CONV["Convergence<br/>Monitor"]

end

%% Processing Infrastructure

subgraph Infrastructure["Processing Infrastructure"]

BATCH["Batch<br/>Processor"]

PARALLEL["Parallel<br/>Executor"]

CACHE["Smart<br/>Cache"]

STORAGE["Trajectory<br/>Storage"]

end

%% Reporting and Visualization

subgraph Output["Reporting & Visualization"]

VIZ["Visualization<br/>Engine"]

EXCEL["Excel<br/>Reporter"]

STATS["Summary<br/>Statistics"]

METRICS["Risk<br/>Metrics"]

end

%% Data Flow - Input to Core

CONFIG --> SIM

MARKET --> LOSSG

PARAMS --> MANU

%% Core orchestration

SIM --> MANU

SIM --> LOSSG

SIM --> INS

MANU <--> INS

LOSSG --> INS

%% Manufacturer to Financial Accounting

MANU --> LEDGER

MANU --> ACCRUAL

MANU --> INSACCT

TAXH --> ACCRUAL

LEDGER --> DECUTIL

ACCRUAL --> DECUTIL

INSACCT --> DECUTIL

%% Insurance subsystem relationships

INSPOL --> INSLAY

INSPROG --> ENHLAY

PRICER --> INSPROG

PRICER --> INSPOL

INS -.-> INSPROG

INS -.-> INSPOL

%% Exposure system

EXPBASE --> FSPROV

MANU -.-> FSPROV

TRENDS --> LOSSG

%% Core to Analysis

SIM --> MONTE

MONTE --> ERGODIC

MONTE --> OPT

ERGODIC --> SENS

OPT --> SENS

%% Validation

MONTE --> ACC

MONTE --> BACK

BACK --> WALK

MONTE --> CONV

CONV --> BATCH

%% Infrastructure

BATCH --> PARALLEL

PARALLEL --> CACHE

CACHE --> STORAGE

%% Output

ERGODIC --> VIZ

OPT --> VIZ

SENS --> VIZ

STORAGE --> STATS

STATS --> EXCEL

STATS --> METRICS

VIZ --> EXCEL

%% Styling

classDef external fill:#e1f5fe,stroke:#01579b,stroke-width:2px

classDef core fill:#fff3e0,stroke:#e65100,stroke-width:2px

classDef financial fill:#fff9c4,stroke:#f9a825,stroke-width:2px

classDef insurance fill:#ffe0b2,stroke:#e65100,stroke-width:2px

classDef exposure fill:#f3e5f5,stroke:#6a1b9a,stroke-width:2px

classDef analysis fill:#f3e5f5,stroke:#4a148c,stroke-width:2px

classDef validation fill:#e8f5e9,stroke:#1b5e20,stroke-width:2px

classDef infra fill:#fce4ec,stroke:#880e4f,stroke-width:2px

classDef output fill:#e0f2f1,stroke:#004d40,stroke-width:2px

class CONFIG,MARKET,PARAMS external

class SIM,MANU,LOSSG,INS core

class LEDGER,ACCRUAL,INSACCT,TAXH,DECUTIL financial

class INSPOL,INSLAY,INSPROG,ENHLAY,PRICER insurance

class EXPBASE,FSPROV,TRENDS exposure

class ERGODIC,OPT,MONTE,SENS analysis

class ACC,BACK,WALK,CONV validation

class BATCH,PARALLEL,CACHE,STORAGE infra

class VIZ,EXCEL,STATS,METRICS output

System Overview

The Ergodic Insurance Limits framework is designed as a modular, high-performance system for analyzing insurance purchasing decisions through the lens of ergodic theory. The architecture follows these key principles:

1. Separation of Concerns

Core Simulation: Handles the fundamental business and insurance mechanics

Financial Accounting: Provides double-entry ledger, accrual accounting, insurance accounting, and tax handling – all using Python’s

Decimaltype for precisionInsurance Subsystem: Provides

InsuranceProgramwithEnhancedInsuranceLayerfor coverage modeling, with market-cycle-aware pricing viaInsurancePricer. (The legacyInsurancePolicy/InsuranceLayerclasses are deprecated.)Exposure & Trends: Dynamically adjusts claim frequencies using actual financial state (via the

FinancialStateProviderprotocol) and applies trend multipliers over timeAnalysis Layer: Provides ergodic and optimization capabilities

Infrastructure: Manages computational efficiency and data handling

Validation: Ensures accuracy and robustness of results

Output: Delivers insights through visualizations and reports

2. Data Flow Architecture

Configuration and market data flow into the simulation engine

The

WidgetManufacturerinternally usesLedger,AccrualManager,InsuranceAccounting, andTaxHandlerfor precise financial trackingAll financial amounts use Python’s

Decimaltype (viadecimal_utils) to prevent floating-point drift across long simulationsThe

Ledgermaintains an O(1) current balance cache with pruning support for performanceSimulations generate trajectories processed by analysis modules

Infrastructure layers provide caching and parallelization

Results flow to visualization and reporting components

3. Key Interactions

The Simulation Engine orchestrates the time evolution of the business model

The Manufacturer Model interacts with the Insurance Program for claim processing and uses the Ledger for all balance sheet operations

AccrualManager tracks timing differences between cash movements and accounting recognition (wages, interest, taxes, insurance claims)

InsuranceAccounting handles premium amortization as a prepaid asset and tracks insurance claim recoveries

TaxHandler consolidates tax calculation, accrual, and payment logic, delegating accrual tracking to the AccrualManager

InsurancePricer supports market cycles (Soft / Normal / Hard) to generate realistic premiums for insurance programs

The Exposure System uses a

FinancialStateProviderprotocol so thatExposureBasesubclasses query live financial state from the manufacturer for state-driven claim generationTrend classes (in

trends.py) provide multiplicative adjustments to claim frequencies and severities over time, supporting linear, scenario-based, and stochastic trendsMonte Carlo Engine generates multiple scenarios for statistical analysis

Ergodic Analyzer compares time-average vs ensemble-average growth

Batch Processor and Parallel Executor enable high-performance computing

4. Financial Accounting Subsystem

The financial accounting subsystem was introduced to provide GAAP-compliant financial tracking within the simulation. This subsystem is internal to the WidgetManufacturer and consists of four tightly integrated components:

flowchart LR

MANU["WidgetManufacturer"] --> LEDGER["Ledger"]

MANU --> ACCRUAL["AccrualManager"]

MANU --> INSACCT["InsuranceAccounting"]

MANU --> TAXH["TaxHandler"]

TAXH --> ACCRUAL

LEDGER --> DECUTIL["decimal_utils"]

ACCRUAL --> DECUTIL

INSACCT --> DECUTIL

classDef manuClass fill:#fff3e0,stroke:#e65100,stroke-width:2px

classDef finClass fill:#fff9c4,stroke:#f9a825,stroke-width:2px

classDef utilClass fill:#e0f2f1,stroke:#004d40,stroke-width:2px

class MANU manuClass

class LEDGER,ACCRUAL,INSACCT,TAXH finClass

class DECUTIL utilClass

Ledger: Event-sourcing double-entry ledger with a typed

AccountNameenum (preventing typo bugs),AccountTypeclassification, O(1) balance lookups via an internal cache, and support for pruning old transactionsAccrualManager: Tracks accrual items (wages, interest, taxes, insurance claims, revenue) with configurable payment schedules (immediate, quarterly, annual, custom)

InsuranceAccounting: Manages premium payments as prepaid assets with straight-line monthly amortization, and tracks insurance claim recoveries separately from claim liabilities

TaxHandler: Centralizes tax calculation and accrual management, explicitly designed to avoid circular dependencies in the tax flow; delegates accrual tracking to

AccrualManagerdecimal_utils: Foundation module providing

to_decimal(),quantize_currency(), and standard constants (ZERO,ONE,PENNY) used by all financial modules

5. Insurance Subsystem

The insurance subsystem provides two complementary paths for modeling coverage:

flowchart TB

subgraph Deprecated["Deprecated"]

INSPOL["InsurancePolicy"]

INSLAY["InsuranceLayer"]

INSPOL --> INSLAY

end

subgraph Primary["Primary"]

INSPROG["InsuranceProgram"]

ENHLAY["EnhancedInsuranceLayer"]

INSPROG --> ENHLAY

end

PRICER["InsurancePricer<br/>(Soft / Normal / Hard)"]

PRICER --> INSPROG

INSPOL -.->|deprecated, use| INSPROG

classDef deprecatedClass fill:#ffcdd2,stroke:#b71c1c,stroke-width:2px

classDef primaryClass fill:#fff3e0,stroke:#ef6c00,stroke-width:2px

classDef pricerClass fill:#f3e5f5,stroke:#7b1fa2,stroke-width:2px

class INSPOL,INSLAY deprecatedClass

class INSPROG,ENHLAY primaryClass

class PRICER pricerClass

Primary Path:

InsuranceProgram(ininsurance_program.py) usesEnhancedInsuranceLayerobjects for full-featured coverage modeling including reinstatements, aggregate limits, and market-cycle-aware pricingDeprecated:

InsurancePolicy(ininsurance.py) withInsuranceLayeris deprecated in favor ofInsuranceProgramInsurancePricer (in

insurance_pricing.py) supports threeMarketCyclestates –HARD(60% loss ratio),NORMAL(70%), andSOFT(80%)

6. Exposure & Trend System

The exposure and trend system models how insurance risks evolve dynamically during simulation:

flowchart LR

MANU["WidgetManufacturer<br/>(implements protocol)"] -.-> FSPROV["FinancialStateProvider<br/>(Protocol)"]

FSPROV --> EXPBASE["ExposureBase<br/>(Dynamic Frequency)"]

TRENDS["trends.py<br/>(Trend Multipliers)"] --> LOSSG["ManufacturingLossGenerator"]

EXPBASE --> LOSSG

classDef coreClass fill:#fff3e0,stroke:#e65100,stroke-width:2px

classDef protoClass fill:#e1f5fe,stroke:#01579b,stroke-width:2px

classDef trendClass fill:#f3e5f5,stroke:#6a1b9a,stroke-width:2px

class MANU coreClass

class FSPROV,EXPBASE protoClass

class TRENDS,LOSSG trendClass

FinancialStateProvider: A

Protocol(inexposure_base.py) defining properties likecurrent_revenue,current_assets,current_equityand their base counterparts.WidgetManufacturerimplements this protocol.ExposureBase: Abstract base for exposure classes that query live financial state to compute frequency multipliers (e.g.,

RevenueExposurescales claim frequency based on actual revenue vs. base revenue)trends.py: Provides a hierarchy of trend classes (

TrendABC,LinearTrend,ScenarioTrend, and stochastic variants) that apply multiplicative adjustments to claim frequencies and severities over time, supporting both annual and sub-annual time steps with optional seeded reproducibility

7. External Dependencies

The system integrates with:

NumPy/SciPy for numerical computations

Pandas for data manipulation

Matplotlib/Plotly for visualizations

OpenPyXL for Excel reporting

Multiprocessing for parallel execution

Python’s

decimalmodule for precise financial arithmetic